Recon Technology Ltd (RCON): Is Oil & Gas Attractive Relative To NasdaqCM Peers?

Recon Technology Ltd (NASDAQ:RCON), a USD$6.63M small-cap, operates in the oil and gas industry which has endured a continued decline in oil prices since 2014. However, energy-sector analysts are forecasting for the entire industry, the bottom line growth to double in the upcoming year, and a massive triple-digit earnings growth over the next couple of years. Not surprisingly, this rate is more than double the growth rate of the US stock market as a whole. Is the oil and gas industry an attractive sector-play right now? In this article, I’ll take you through the energy sector growth expectations, as well as evaluate whether RCON is lagging or leading its competitors in the industry. Check out our latest analysis for Recon Technology

What’s the catalyst for RCON's sector growth?

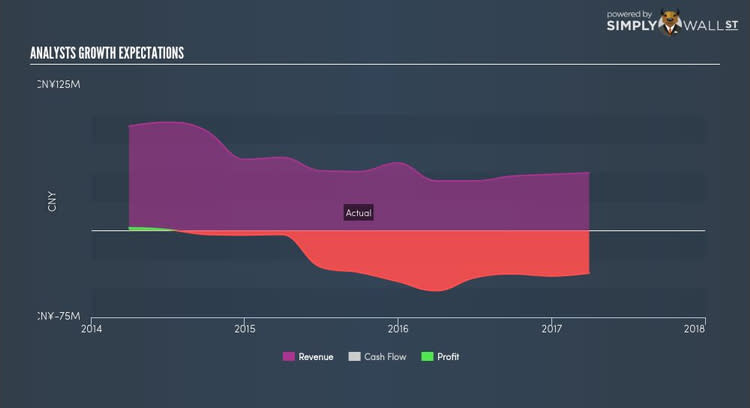

The oil price collapse drove a negative 40 percent growth in the energy sector in the past five years. Global oil and gas companies cut capital expenditures by about 40 percent during 2014 and 2016, and as part of this cost cutting initiative, some 400,000 workers were let go, with major projects cancelled or deferred. In the previous year, the industry endured negative growth of -29 percent, underperforming the US market growth of 53 percent. RCON leads the pack with its impressive earnings growth of 42 percent over the past year. This proven growth may make RCON a more expensive stock relative to its peers.

Is RCON and the sector relatively cheap?

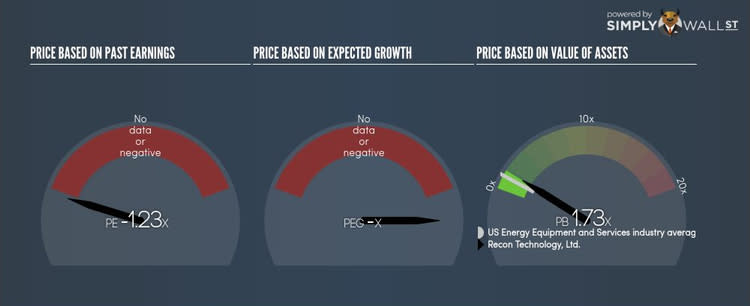

The oil and gas industry is trading at a PE ratio of 58 times, higher than the rest of the US stock market PE of 27 times. This illustrates a somewhat overpriced sector compared to the rest of the market. However, the industry returned a lower 3 percent compared to the market’s 16 percent, illustrative of the recent sector upheaval. Since RCON’s earnings doesn’t seem to reflect its true value, its PE ratio isn’t very useful. A loose alternative to gauge RCON’s value is to assume the stock should be relatively in-line with its industry.

What this means for you:

Are you a shareholder? RCON recently delivered an industry-beating growth rate in earnings, which is a positive for shareholders. If you’re bullish on the stock and well-diversified by industry, you may decide to hold onto RCON as part of your portfolio. However, if you’re relatively concentrated in oil and gas, you may want to value RCON based on its cash flows to determine if it is overpriced based on its current growth outlook.

Are you a potential investor? If RCON has been on your watchlist for a while, now may be the time to enter into the stock, if you like its ability to deliver growth and are not highly concentrated in the oil and gas industry. However, before you make a decision on the stock, I suggest you look at RCON’s future cash flows in order to assess whether the stock is trading at a reasonable price, as well as other important fundamentals such as the company’s financial health in order to build a holistic investment thesis.

For a deeper dive into Recon Technology's stock, take a look at the company's latest free analysis report to find out more on its financial health and other fundamentals. Interested in other energy stocks instead? Use our free playform to see my list of over 300 other oil and gas companies trading on the market.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.