Recticel NV/SA (EBR:REC): A Fundamentally Attractive Investment

Building up an investment case requires looking at a stock holistically. Today I’ve chosen to put the spotlight on Recticel NV/SA (EBR:REC) due to its excellent fundamentals in more than one area. REC is a financially-sound company with a a strong history of performance, trading at a discount. Below, I’ve touched on some key aspects you should know on a high level. If you’re interested in understanding beyond my broad commentary, read the full report on Recticel/SA here.

Undervalued with proven track record and pays a dividend

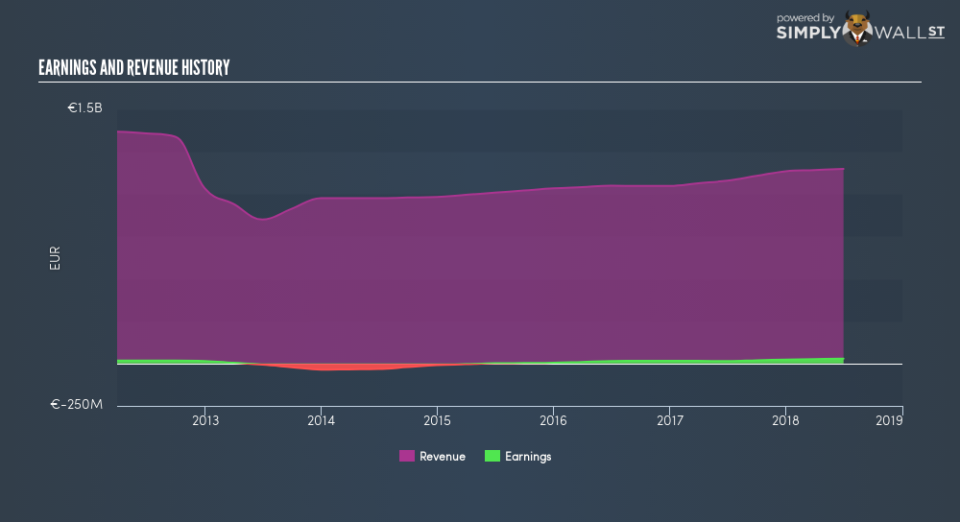

In the previous year, REC has ramped up its bottom line by 87%, with its latest earnings level surpassing its average level over the last five years. Not only did REC outperformed its past performance, its growth also exceeded the Chemicals industry expansion, which generated a 18% earnings growth. This is an optimistic signal for the future. REC’s has produced operating cash levels of 0.55x total debt over the past year, which implies that REC’s management has put its borrowings into good use by generating enough cash to cover a sufficient portion of borrowings. Also, REC’s earnings amply cover its interest expense. Paying interest on time and in full can help the company get favourable debt terms in the future, leading to lower cost of debt and helps REC expand.

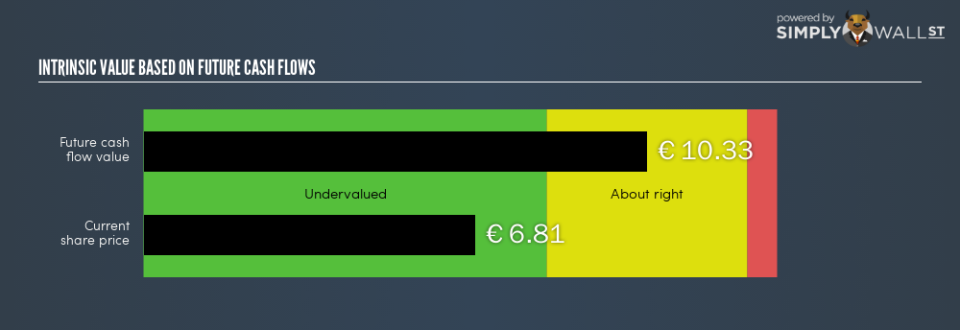

REC is currently trading below its true value, which means the market is undervaluing the company’s expected cash flow going forward. According to my intrinsic value of the stock, which is driven by analyst consensus forecast of REC’s earnings, investors now have the opportunity to buy into the stock to reap capital gains. Compared to the rest of the chemicals industry, REC is also trading below its peers, relative to earnings generated. This bolsters the proposition that REC’s price is currently discounted.

Next Steps:

For Recticel/SA, I’ve put together three relevant factors you should further examine:

Future Outlook: What are well-informed industry analysts predicting for REC’s future growth? Take a look at our free research report of analyst consensus for REC’s outlook.

Dividend Income vs Capital Gains: Does REC return gains to shareholders through reinvesting in itself and growing earnings, or redistribute a decent portion of earnings as dividends? Our historical dividend yield visualization quickly tells you what your can expect from REC as an investment.

Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of REC? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.