ResMed (RMD) Gains From Strong Device Sales Amid Macro Woes

ResMed RMD is leading the market with its cloud-connected flow generator platforms. However, macroeconomic headwinds continue to affect the stock. The stock carries a Zacks Rank #3 (Hold).

ResMed continues to see robust demand for its market-leading mask portfolio despite being faced with challenges related to lower new patient setups from a competitor recall. Continued product development is driving growth within this business globally. The company successfully introduced a full suite of masks in AirFit, AirTouch and other ranges. Further, to promote greater patient adherence, ResMed offers advanced and expanded integrations of its therapy-based software solutions, including AirView.

ResMed’s increased device sales continue to drive overall revenue growth, reflecting the ongoing combined availability of AirSense 10 and AirSense 11 sleep devices to support strong underlying global demand. The company has consistently witnessed strong sales within this business since fiscal 2021 with the launch of its new platform of connected CPAP and APAP devices, AirSense 11, which now comes with features such as a touch screen, algorithms for patients new to therapy and digital enhancements, such as over-the-air update capabilities.

Image Source: Zacks Investment Research

ResMed’s respiratory care business continues to drive growth and the adoption of bilevel and other non-invasive ventilator solutions worldwide. The company is investing in newer-to-market technologies for patients, including home-based high-flow therapy (“HFT”) for treating chronic obstructive pulmonary disease or COPD at home.

Although still early for market development, ResMed continues to generate clinical evidence and economic outcomes to support the broader adoption of these technology innovations for treating lung disease at home. Investing in these opportunities enables the company to address COPD, one of the top global diseases for hospitalization and the principal cause of re-hospitalization in the United States.

On the flip side, the company’s high debt level remains a concern. As of Jun 30, 2023, long-term debt was $1.43 billion, while the cash and cash equivalents balance was only $228 million. A higher debt level induces higher interest payments, which come along with the risk of failure to pay the same. At the end of fiscal 2023, the company had a times interest earned ratio of 24.3%, sequentially lower than the fiscal third quarter’s 29%.

Global macroeconomic conditions, including inflation, supply chain disruptions and fluctuations in foreign currency exchange rates and volatility in capital markets could continue to adversely impact ResMed’s results of operations. Decline in the global economic environment may reduce demand for the company’s products, resulting in lower sales, lower product prices and reduced reimbursement rates by third-party payers, while increasing the cost of operating the business.

These factors have affected ResMed’s supply chain operations globally, as evident from the constraints on raw materials and electronic components. Furthermore, with the sustained inflationary pressures in the future, the company may struggle to keep in check its operating expenses as a percentage of net revenues. We are worried that this might dent ResMed’s profitability.

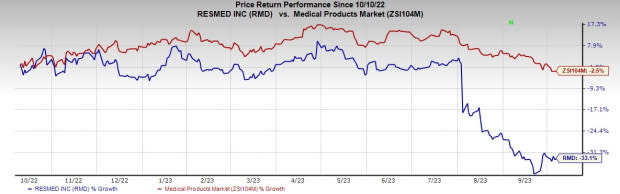

Shares of ResMed have plunged 33.1% over the past year compared with 2.5% decline of the industry.

Key Picks

Some better-ranked stocks in the broader medical space are DaVita Inc. DVA, Quanterix QTRX and Align Technology ALGN, each carrying a Zacks Rank #2 (Buy).

DaVita has an estimated long-term growth rate of 12.7%. DVA’s earnings surpassed estimates in three of the trailing four quarters and missed once, with the average surprise being 21.4%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

DaVita has gained 25.5% against the industry’s 8.9% decline over the past year.

Estimates for Quanterix’s 2023 loss per share have remained constant at 97 cents in the past 30 days. Shares of the company have surged 141.5% in the past year compared with the industry’s fall of 5.6%.

QTRX’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 30.39%. In the last reported quarter, it posted an earnings surprise of 55.56%.

Estimates for Align Technology’s 2023 earnings have moved up from $8.77 to $8.78 per share in the past 30 days. Shares of the company have increased 27% in the past year compared with the industry’s rise of 14.3%

ALGN’s earnings beat estimates in three of the trailing four quarters and missed in one. In the last reported quarter, it posted an earnings surprise of 9.90%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

DaVita Inc. (DVA) : Free Stock Analysis Report

Align Technology, Inc. (ALGN) : Free Stock Analysis Report

ResMed Inc. (RMD) : Free Stock Analysis Report

Quanterix Corporation (QTRX) : Free Stock Analysis Report