Should You Retain Cousins Properties (CUZ) Stock for Now?

Cousins Properties CUZ is well-poised to benefit from its unmatched portfolio of class A office assets concentrated in the high-growth markets in the Sun Belt region. Its impressive tenant roster and capital-recycling efforts position it well for long-term growth. Its robust balance sheet augurs well. However, intense competition, along with high supply in the office real estate market is expected to adversely impact CUZ’s pricing power. Also, higher interest rates make us apprehensive.

What’s Aiding it?

CUZ has been witnessing a recovery in demand for its high-quality, well-placed office properties on the back of tenants’ growing preference for premier office spaces with class-apart amenities. This is evidenced by the rebound in the new leasing volume. Also, the steady return of the workforce to offices has been a contributing factor.

In the nine months ended Sep 30, 2023, Cousins Properties executed 101 leases for a total of 1.2 million square feet of office space, with a weighted average term of 7.7 years. This included 691,232 square feet of new and expansion leases, denoting 55.7% of the total leasing activity.

Going forward, the next cycle of office space demand will likely be driven by an inbound migration and significant investments announced by office occupiers to expand the footprint in the Sun Belt regions. This is expected to boost the demand for CUZ’s properties in the quarters ahead.

The company enjoys a well-diversified, high-end tenant roster. This assures stable rental revenues for it over time and lowers the risk associated with dependency on single-industry tenants.

Cousins Properties’ capital-recycling moves to enhance its portfolio quality with trophy asset acquisitions and opportunistic developments in high-growth Sun Belt submarkets seem encouraging for long-term growth while preserving financial flexibility. In addition, a notable development pipeline is likely to deliver meaningful additional annualized net operating income in the coming years.

This office real estate investment trust (REIT) maintains a healthy balance sheet position and exited the third quarter of 2023 with cash and cash equivalents of $6.9 million. As of Sep 30, 2023, it had a borrowing capacity of $855.5 million under its $1 billion credit facility. With limited near-term debt maturities and ample financial flexibility, it seems well-placed to bank on long-term growth opportunities.

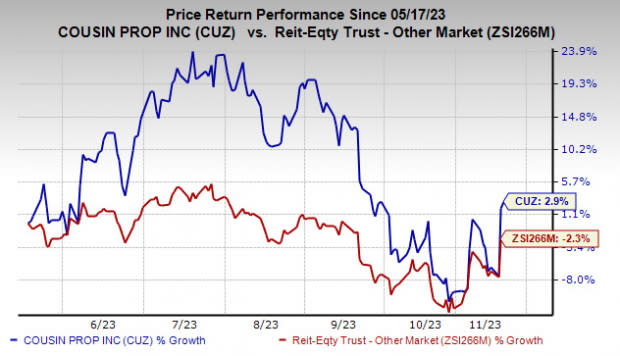

In the past six months, shares of this Zacks Rank #3 (Hold) company have gained 2.9% against the industry’s fall of 2.3%.

Image Source: Zacks Investment Research

What’s Hurting it?

However, Intense competition from developers, owners and operators of office properties and other commercial real estate limits is likely to limit Cousins Properties’ ability to retain tenants at relatively higher rents and dent its pricing power.

Also, with an elevated supply of office properties in the company’s market, it may become increasingly challenging for it to backfill near-term tenant move-outs, resulting in lesser scope for rent and occupancy growth. Further, given the current macroeconomic uncertainties, the demand for office spaces is expected to remain choppy in the near term, weighing on this office REIT.

A high interest rate environment is a concern for Cousins Properties. The company may find it difficult to purchase or develop real estate as borrowing costs will likely be on the higher side due to elevated rates. Moreover, the dividend payout may become less attractive than the yields on fixed-income and money market accounts.

Stocks to Consider

Some better-ranked stocks from the REIT sector are Welltower WELL, EastGroup Properties EGP and Stag Industrial STAG, each carrying a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Welltower’s 2023 FFO per share has been raised marginally over the past week to $3.58.

The Zacks Consensus Estimate for EastGroup’s current-year FFO per share has been raised marginally over the past week to $7.69.

The Zacks Consensus Estimate for Stag’s ongoing year’s FFO per share has been raised 1.3% over the past month to $2.28.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cousins Properties Incorporated (CUZ) : Free Stock Analysis Report

Stag Industrial, Inc. (STAG) : Free Stock Analysis Report

EastGroup Properties, Inc. (EGP) : Free Stock Analysis Report

Welltower Inc. (WELL) : Free Stock Analysis Report