Should You Retain Huntington (HBAN) for Its Dividend Yield?

The banking sector is facing challenges amid the current operating backdrop, with expectations of an economic slowdown in the near term. Hence, solid dividend-yielding stocks should be on investors’ radar. Today, we are discussing one such stock, Huntington Bancshares HBAN.

This Columbus, OH-based multi-state diversified regional bank, through its banking subsidiary, The Huntington National Bank, provides a comprehensive suite of banking, payments, wealth management, and risk management products and services.

HBAN has been paying its quarterly dividends on a regular basis and raising the same. The last hike of 3.3% to 15.5 cents per share was announced in October 2021. Over the past five years, it increased dividends twice, with an annualized dividend growth rate of 2.03%.

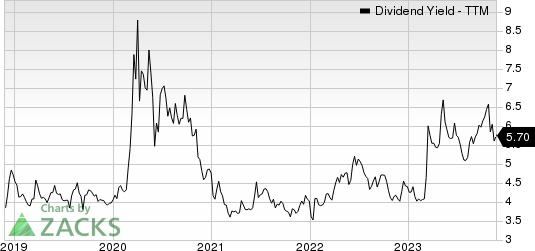

Considering the Oct 22 closing price of $10.87 per share, Huntington’s current dividend yield is pegged at 5.7%. This is impressive compared with the industry’s average of 3.7% and attracts investors as it represents a steady income stream.

Huntington Bancshares Incorporated Dividend Yield (TTM)

Huntington Bancshares Incorporated dividend-yield-ttm | Huntington Bancshares Incorporated Quote

Is Huntington stock worth a look to earn a high dividend yield? Let’s check the company’s fundamentals to understand its risks and rewards for making a proper investment decision.

Apart from regular quarterly dividend payouts, HBAN has a share repurchase program in place. In January 2023, the company’s board authorized the repurchase of common shares worth $1 billion till Dec 31, 2024.

However, it did not repurchase shares under the current authorization in the first nine months of 2023. Also, to improve its capital position, management does not expect to utilize this program in the current year as part of its 2023 plan.

As of Sep 30, 2023, Huntington had liquidity, comprising cash and contingent borrowing capacity, of $91 billion. The company’s largest source of liquidity is core deposits. Its core deposits were $144.2 billion in third-quarter 2023 end and comprised 97% of total deposits. During the same period, it had total debt (comprising long-term debt and short-term borrowings) of $13.5 billion. Given its decent liquidity, dividend payments seem sustainable.

Huntington, one of the top 20 bank holding companies in the United States, remains focused on acquiring the industry's best deposit franchise. The company’s total deposits witnessed a four-year compounded annual growth rate (CAGR) of 21.6% in 2022. The rising trend continued in the first nine months of 2023.

The company’s loan balance rose in 2022, seeing a four-year CAGR of 16.6%. The uptrend persisted in the first nine months of 2023. Supported by strong loan demand and deposit balance, its balance sheet is expected to keep improving. Management projects loan growth of approximately 5% in 2023. In 2024, the company anticipates sustaining deposit momentum with a continued focus on acquiring and deepening primary bank customer relationships.

With expectations of the Federal Reserve keeping interest rates high in the near term, Huntington’s net interest income (NII) and the yield on interest-earning assets are expected to witness decent growth. In fact, management expects to maintain modest asset sensitivity to support net interest margin and NII growth in a high interest-rate scenario in 2024.

However, weak mortgage business on higher rates is expected to ail fee income. Further, rising costs may hinder bottom-line growth. Also, loan concentration, comprising 56% of commercial loans in the total loan portfolio, is concerning.

Over the past six months, shares of HBAN have gained 4.3% compared with the industry’s rise of 10%.

Image Source: Zacks Investment Research

HBAN currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Other Bank Stocks With Attractive Dividend Yields

Banking stocks like Premier Financial PFC and KeyCorp KEY are worth a look as these, too, have robust dividend yields.

Considering the Oct 22 closing price, PFC’s dividend yield is pegged at 6.2%. In the past six months, shares of PFC have gained 40.8%.

Based on the last day’s closing price, KeyCorp’s dividend yield is pinned at 6.82%. In the past six months, shares of KEY have gained 19%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Huntington Bancshares Incorporated (HBAN) : Free Stock Analysis Report

KeyCorp (KEY) : Free Stock Analysis Report

Premier Financial Corp. (PFC) : Free Stock Analysis Report