Returns At Tombador Iron (ASX:TI1) Are On The Way Up

What are the early trends we should look for to identify a stock that could multiply in value over the long term? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. So on that note, Tombador Iron (ASX:TI1) looks quite promising in regards to its trends of return on capital.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Tombador Iron, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

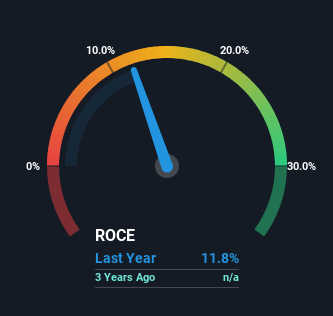

0.12 = AU$5.4m ÷ (AU$55m - AU$9.8m) (Based on the trailing twelve months to June 2022).

Thus, Tombador Iron has an ROCE of 12%. In absolute terms, that's a satisfactory return, but compared to the Metals and Mining industry average of 9.1% it's much better.

Check out our latest analysis for Tombador Iron

Historical performance is a great place to start when researching a stock so above you can see the gauge for Tombador Iron's ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Tombador Iron, check out these free graphs here.

So How Is Tombador Iron's ROCE Trending?

The fact that Tombador Iron is now generating some pre-tax profits from its prior investments is very encouraging. Shareholders would no doubt be pleased with this because the business was loss-making two years ago but is is now generating 12% on its capital. Not only that, but the company is utilizing 2,728,349% more capital than before, but that's to be expected from a company trying to break into profitability. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, both common traits of a multi-bagger.

On a related note, the company's ratio of current liabilities to total assets has decreased to 18%, which basically reduces it's funding from the likes of short-term creditors or suppliers. So this improvement in ROCE has come from the business' underlying economics, which is great to see.

In Conclusion...

Overall, Tombador Iron gets a big tick from us thanks in most part to the fact that it is now profitable and is reinvesting in its business. And since the stock has fallen 48% over the last three years, there might be an opportunity here. With that in mind, we believe the promising trends warrant this stock for further investigation.

If you'd like to know more about Tombador Iron, we've spotted 5 warning signs, and 3 of them are concerning.

While Tombador Iron may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.