Reynolds (NASDAQ:REYN) Reports Q4 In Line With Expectations

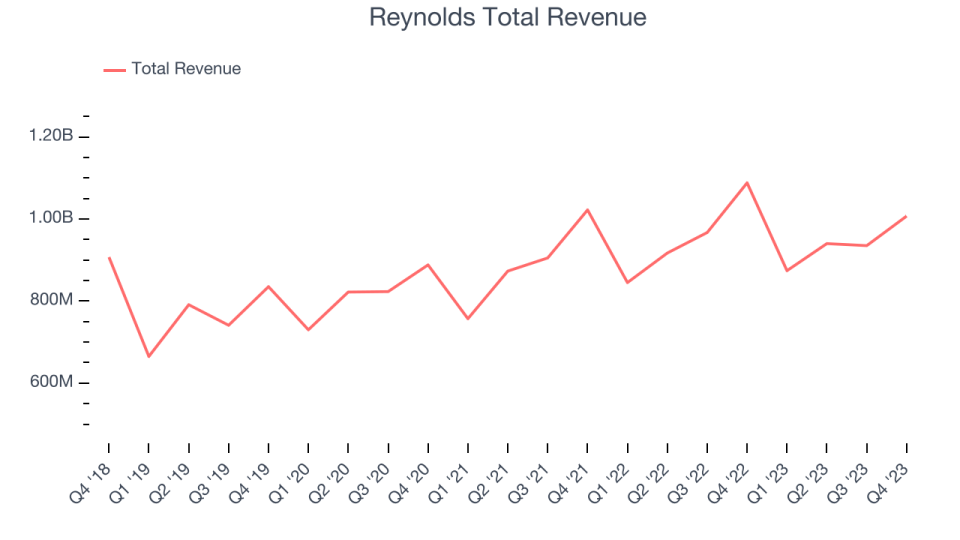

Household products company Reynolds (NASDAQ:REYN) reported results in line with analysts' expectations in Q4 FY2023, with revenue down 7.5% year on year to $1.01 billion. It made a GAAP profit of $0.65 per share, improving from its profit of $0.53 per share in the same quarter last year.

Is now the time to buy Reynolds? Find out by accessing our full research report, it's free.

Reynolds (REYN) Q4 FY2023 Highlights:

Revenue: $1.01 billion vs analyst estimates of $1.01 billion (small beat)

EPS: $0.65 vs analyst estimates of $0.62 (4.9% beat)

Guidance for EPS: Q1 guidance of $0.22 (vs. expectations of $0.20) and full year guidance of $1.61 (in line)

Free Cash Flow of $194 million, similar to the previous quarter

Gross Margin (GAAP): 30.7%, up from 22.7% in the same quarter last year

Organic Revenue was down 8% year on year

Sales Volumes were down 7% year on year

Market Capitalization: $5.84 billion

Best known for its aluminum foil, Reynolds (NASDAQ:REYN) is a household products company whose products focus on food storage, cooking, and waste.

Household Products

Household products companies engage in the manufacturing, distribution, and sale of goods that maintain and enhance the home environment. This includes cleaning supplies, home improvement tools, kitchenware, small appliances, and home decor items. Companies within this sector must focus on product quality, innovation, and cost efficiency to remain competitive. Household products stocks are generally stable investments, as many of the industry's products are essential for a comfortable and functional living space. Recently, there's been a growing emphasis on eco-friendly and sustainable offerings, reflecting the evolving consumer preferences for environmentally conscious options.

Sales Growth

Reynolds is larger than most consumer staples companies and benefits from economies of scale, giving it an edge over its smaller competitors.

As you can see below, the company's annualized revenue growth rate of 4.8% over the last three years was weak as consumers bought less of its products. We'll explore what this means in the "Volume Growth" section.

This quarter, Reynolds reported a rather uninspiring 7.5% year-on-year revenue decline to $1.01 billion in revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Key Takeaways from Reynolds's Q4 Results

We liked that revenue beat by a small amount and EPS beat more convincingly. We were also impressed by Reynolds's optimistic earnings forecast for next quarter, which beat analysts' expectations, although the full year outlook was in line. Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is up 4.2% after reporting and currently trades at $29 per share.

So should you invest in Reynolds right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.