The rising price of oil has been one of the biggest economic stories of the year.

Some experts have argued that the rising cost of gas could negate the benefits consumers reaped from the Trump tax cuts passed in late 2017.

But when it comes to the overall economic impact of rising oil prices, some economists think we’d need to see another 50% rise in the price of oil before the drag from oil prices turns outright negative.

Seth Carpenter, an economist at UBS, and his team on Wednesday released an analysis which said that oil prices would have to top $120 a barrel for the impacts on the U.S. economy to be negative. This is because as the U.S. oil industry has continued to increase production amid the rise in oil prices, the investment in the industry and the need to import less oil have aided overall GDP growth.

As of Thursday afternoon, the price of West Texas Intermediate crude oil was trade near $71 a barrel, up from around $60 at the beginning of the year and around $50 at this same time a year ago.

The average price of a gallon of gas in the U.S. was around $2.92 as of Monday, up from $2.40 at this time last year and $2.52 at the beginning of the year.

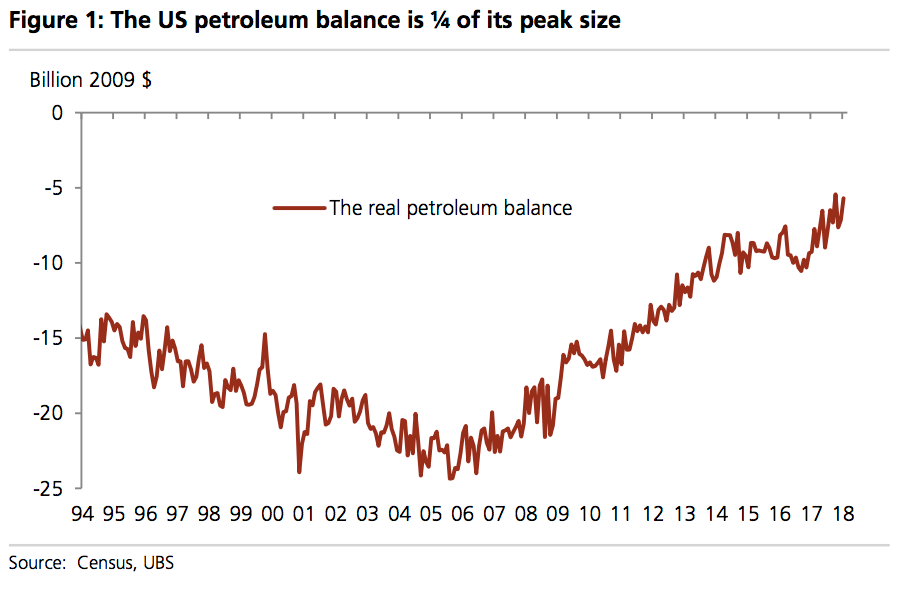

“Fact 1: The US petroleum deficit has dropped sharply and is almost gone,” UBS notes. “Fact 2: The US is now a major marginal producer of oil. These two facts mean that the recent rise in oil prices is not creating a net drag on US economic growth.”

During the last peak in oil prices seen from 2010-2013, the U.S. cut its oil deficit from around $15 to $10 billion. Today, that deficit is about $6 billion, about 25% the size of the deficit back in the mid-00s period ahead of the crisis that was considered “peak oil.”

Recent advances in U.S. fracking and the deregulation of U.S. exports increased global supply, increased investment and employment in the U.S. oil sector, and is seen as the main trigger for the global collapse in oil prices that occurred from late 2014 through 2016.

And though rising prices at the pump can hurt consumers, the overall impact on the economy is to increase investment in an investment-intensive industry, increase exports, and increase employment.

UBS forecasts that the energy sector will add between 100,000-148,000 jobs in the U.S. over the next year. Assuming average wages for mining and manufacturing jobs are earned by these workers, U.S. households would make up to $15 billion in additional income over the next year, according to UBS.

“At current prices, the oil sector is adding almost 40bp to US growth this year, just a touch less than last year,” UBS writes.

“Of course, this contribution is not independent of the price of oil. Because the US is a net importer, rising prices reduce US income. Therefore, oil will once again become a net drag on the US economy if oil prices get sufficiently high. But because the offset from investment is so large, oil prices have to move well into the $100s before this occurs. Even at $120 per barrel, we estimate a positive, if single digit, contribution to US GDP.”

Over at JP Morgan, economist Daniel Silver estimates the increase in oil prices will leave consumers with an additional spending burden equivalent to about 0.3% of GDP. Investment in the oil industry, should tally 0.2% of GDP, leaving the impacts of rising oil prices slightly negative for overall GDP, according to Silver.

Households, however, could lower savings to meet higher energy costs, thus making the net impact of oil’s increase neutral for GDP.

“While historically the consumption impact has overshadowed the capex impact, the rise in energy extraction’s importance in the economy over the past several decades has made the effects more balanced,” Silver writes.

So while President Trump may have bemoaned the “artificially” high oil prices he thinks are being set by OPEC, in the new U.S. economic reality high oil prices are good for growth.

—

Myles Udland is a writer at Yahoo Finance. Follow him on Twitter @MylesUdland