A Rising Share Price Has Us Looking Closely At Choice Hotels International, Inc.'s (NYSE:CHH) P/E Ratio

Choice Hotels International (NYSE:CHH) shareholders are no doubt pleased to see that the share price has bounced 31% in the last month alone, although it is still down 29% over the last quarter. But shareholders may not all be feeling jubilant, since the share price is still down 14% in the last year.

All else being equal, a sharp share price increase should make a stock less attractive to potential investors. In the long term, share prices tend to follow earnings per share, but in the short term prices bounce around in response to short term factors (which are not always obvious). The implication here is that deep value investors might steer clear when expectations of a company are too high. Perhaps the simplest way to get a read on investors' expectations of a business is to look at its Price to Earnings Ratio (PE Ratio). A high P/E ratio means that investors have a high expectation about future growth, while a low P/E ratio means they have low expectations about future growth.

View our latest analysis for Choice Hotels International

How Does Choice Hotels International's P/E Ratio Compare To Its Peers?

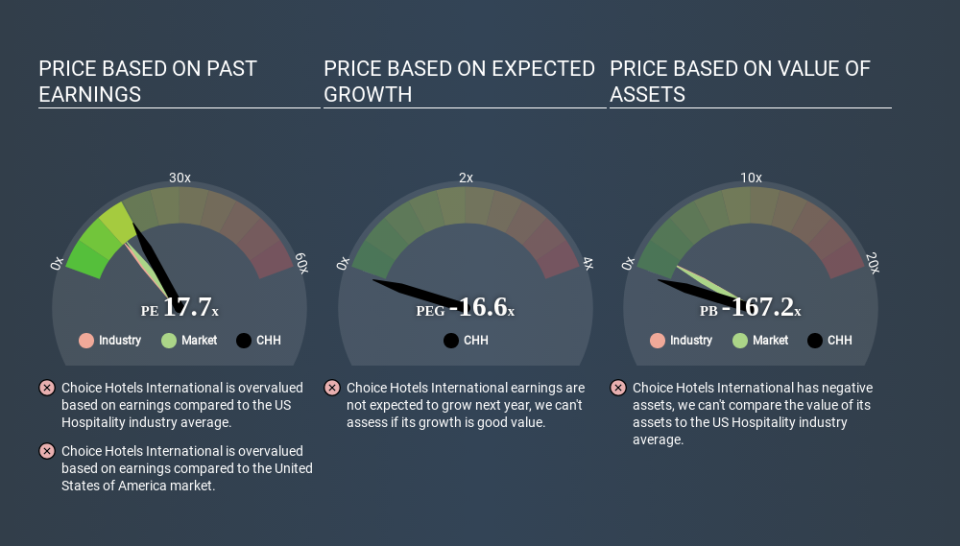

Choice Hotels International's P/E of 17.74 indicates some degree of optimism towards the stock. As you can see below, Choice Hotels International has a higher P/E than the average company (12.7) in the hospitality industry.

Its relatively high P/E ratio indicates that Choice Hotels International shareholders think it will perform better than other companies in its industry classification. The market is optimistic about the future, but that doesn't guarantee future growth. So investors should always consider the P/E ratio alongside other factors, such as whether company directors have been buying shares.

How Growth Rates Impact P/E Ratios

P/E ratios primarily reflect market expectations around earnings growth rates. If earnings are growing quickly, then the 'E' in the equation will increase faster than it would otherwise. That means even if the current P/E is high, it will reduce over time if the share price stays flat. So while a stock may look expensive based on past earnings, it could be cheap based on future earnings.

Choice Hotels International saw earnings per share improve by 4.4% last year. And its annual EPS growth rate over 5 years is 14%.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

The 'Price' in P/E reflects the market capitalization of the company. Thus, the metric does not reflect cash or debt held by the company. Hypothetically, a company could reduce its future P/E ratio by spending its cash (or taking on debt) to achieve higher earnings.

While growth expenditure doesn't always pay off, the point is that it is a good option to have; but one that the P/E ratio ignores.

Is Debt Impacting Choice Hotels International's P/E?

Choice Hotels International's net debt is 21% of its market cap. This could bring some additional risk, and reduce the number of investment options for management; worth remembering if you compare its P/E to businesses without debt.

The Verdict On Choice Hotels International's P/E Ratio

Choice Hotels International trades on a P/E ratio of 17.7, which is above its market average of 13.2. With debt at prudent levels and improving earnings, it's fair to say the market expects steady progress in the future. What is very clear is that the market has become more optimistic about Choice Hotels International over the last month, with the P/E ratio rising from 13.6 back then to 17.7 today. For those who prefer to invest with the flow of momentum, that might mean it's time to put the stock on a watchlist, or research it. But the contrarian may see it as a missed opportunity.

Investors have an opportunity when market expectations about a stock are wrong. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine. So this free visual report on analyst forecasts could hold the key to an excellent investment decision.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.