Ross Stores (NASDAQ:ROST) Beats Expectations in Strong Q4

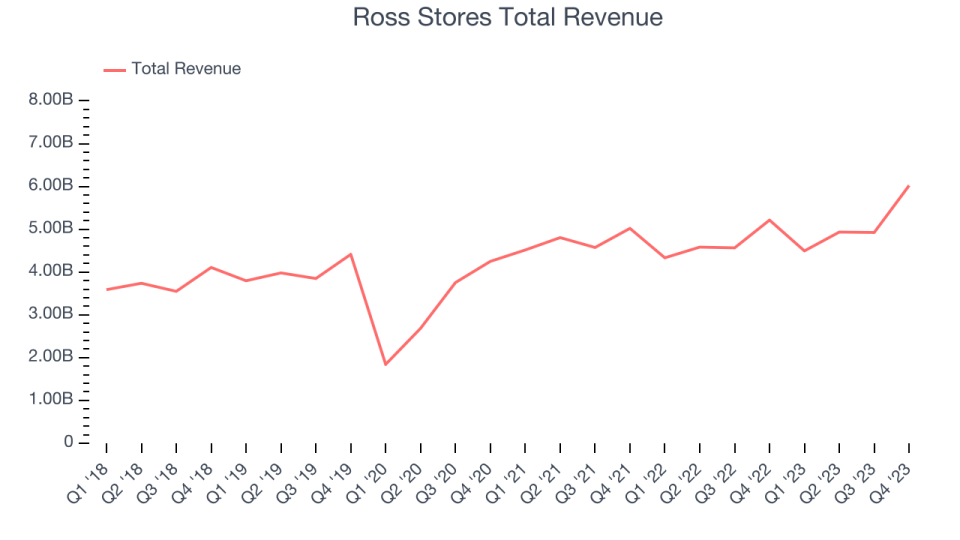

Off-price retail company Ross Stores (NASDAQ:ROST) reported results ahead of analysts' expectations in Q4 FY2023, with revenue up 15.5% year on year to $6.02 billion. It made a GAAP profit of $1.82 per share, improving from its profit of $1.30 per share in the same quarter last year.

Is now the time to buy Ross Stores? Find out by accessing our full research report, it's free.

Ross Stores (ROST) Q4 FY2023 Highlights:

Revenue: $6.02 billion vs analyst estimates of $5.81 billion (3.6% beat)

EPS: $1.82 vs analyst estimates of $1.65 (10.2% beat)

Free Cash Flow of $726.4 million, down 25.9% from the same quarter last year

Gross Margin (GAAP): 27.3%, down from 42.5% in the same quarter last year

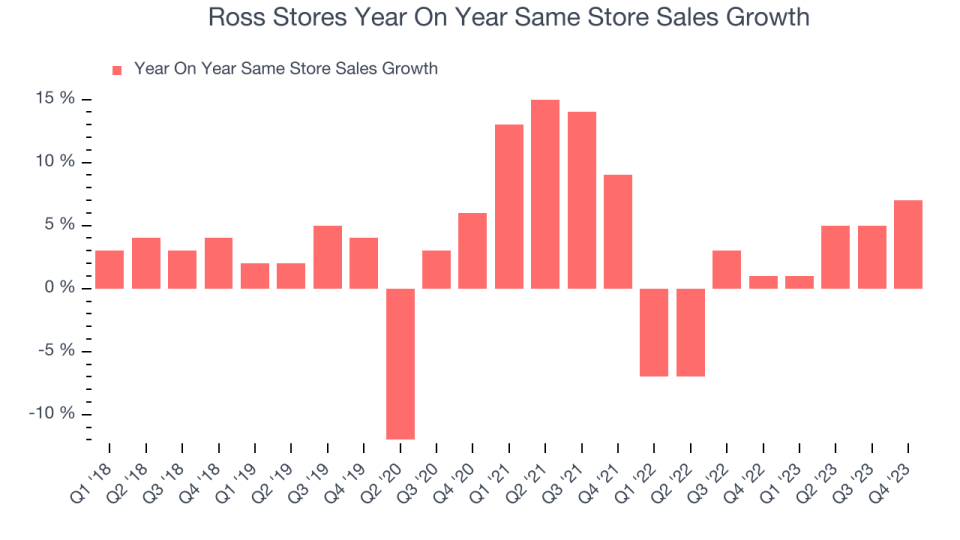

Same-Store Sales were up 7% year on year

Store Locations: 2,109 at quarter end, increasing by 94 over the last 12 months

Market Capitalization: $50.49 billion

Barbara Rentler, Chief Executive Officer, commented, “We are pleased with our fourth quarter sales and earnings results that were well ahead of our expectations. Our above-plan sales were driven by customers’ positive response to our improved assortments of quality branded bargains throughout our stores.”

Selling excess inventory or overstocked items from other retailers, Ross Stores (NASDAQ:ROST) is an off-price concept that sells apparel and other goods at prices much lower than department stores.

Off-Price Apparel and Home Goods Retailer

Off-price retailers, which sell name-brand goods at major discounts because of their unique purchasing and procurement strategies, understand that everyone loves a good deal. Specifically, these companies buy excess inventory and overstocks from manufacturers and other retailers so they can turn around and offer these products at super competitive prices. Despite the unique draw lure of discounts, these off-price retailers must also contend with the secular headwinds of online penetration and stalling retail foot traffic in places like suburban shopping centers.

Sales Growth

Ross Stores is one of the larger companies in the consumer retail industry and benefits from economies of scale, enabling it to gain more leverage on fixed costs and offer consumers lower prices.

As you can see below, the company's annualized revenue growth rate of 6.2% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was weak , but to its credit, it opened new stores and grew sales at existing, established stores.

This quarter, Ross Stores reported robust year-on-year revenue growth of 15.5%, and its $6.02 billion in revenue exceeded Wall Street's estimates by 3.6%. Looking ahead, Wall Street expects sales to grow 3.8% over the next 12 months, a deceleration from this quarter.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Same-Store Sales

Same-store sales growth is an important metric that tracks demand for a retailer's established brick-and-mortar stores and e-commerce platform.

Ross Stores's demand within its existing stores has barely increased over the last eight quarters. On average, the company's same-store sales growth has been flat.

In the latest quarter, Ross Stores's same-store sales rose 7% year on year. This growth was an acceleration from the 1% year-on-year increase it posted 12 months ago, which is always an encouraging sign.

Key Takeaways from Ross Stores's Q4 Results

We were impressed by how significantly Ross Stores blew past analysts' revenue and EPS expectations this quarter, driven by huge outperformance in its same-store sales (7% growth vs estimates of 3%). On the other hand, its full-year 2024 same-store sales and earnings guidance was underwhelming. Management noted it was being conservative because "while inflation has moderated, housing, food, and gasoline costs remain elevated and continue to pressure our low-to-moderate income customers’ discretionary spend".

During the quarter, Ross Stores approved a new two-year $2.1 billion stock repurchase program for fiscal 2024 and 2025 and authorized a 10% increase in its quarterly cash dividend to $0.3675 per share.

Despite the soft guidance, we think this was a strong quarter that should satisfy shareholders. The stock is flat after reporting and currently trades at $149.42 per share.

Ross Stores may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.