RPC Inc (RES): A Modestly Undervalued Gem in the Oil & Gas Industry?

With a daily gain of 6.83%, a three-month gain of 19.43%, and an Earnings Per Share (EPS) of 1.35, RPC Inc (NYSE:RES) presents an intriguing case for value investors. This article aims to answer the question: Is RPC (NYSE:RES) modestly undervalued? Let's delve into a comprehensive analysis of RPC's valuation, financial strength, profitability, and growth prospects.

Company Overview

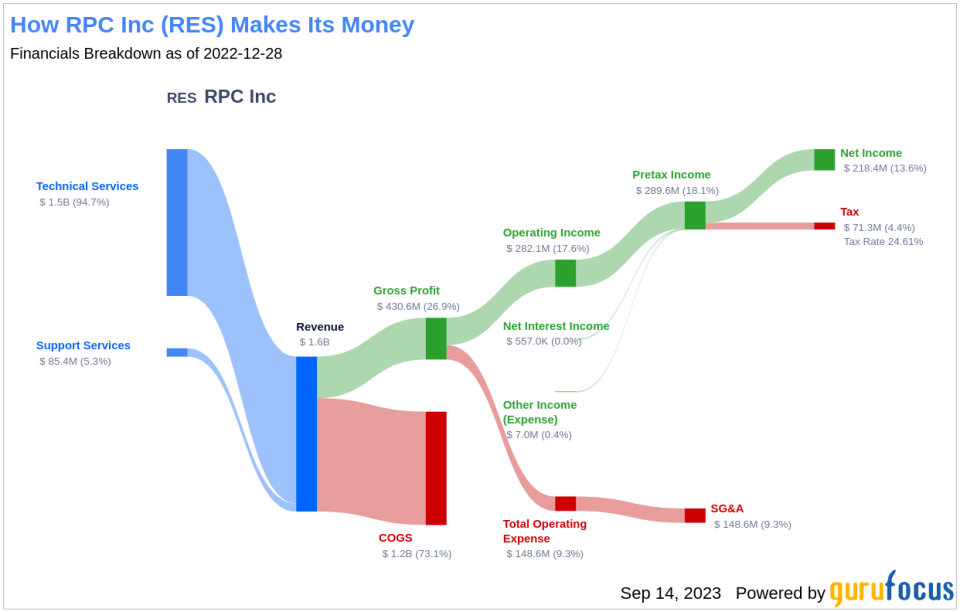

RPC Inc is a specialized oilfield services provider, serving independent and major oil and gas companies engaged in the exploration, production, and development of oil and gas properties across the United States. The company operates through two main segments: Technical Services and Support Services, with the former generating maximum revenue. The Technical Services segment includes pressure pumping, downhole tools, coiled tubing, snubbing, nitrogen, well control, wireline, and fishing. The Support Services segment offers drill pipe and related tools, pipe handling, pipe inspection and storage services, and oilfield training and consulting services.

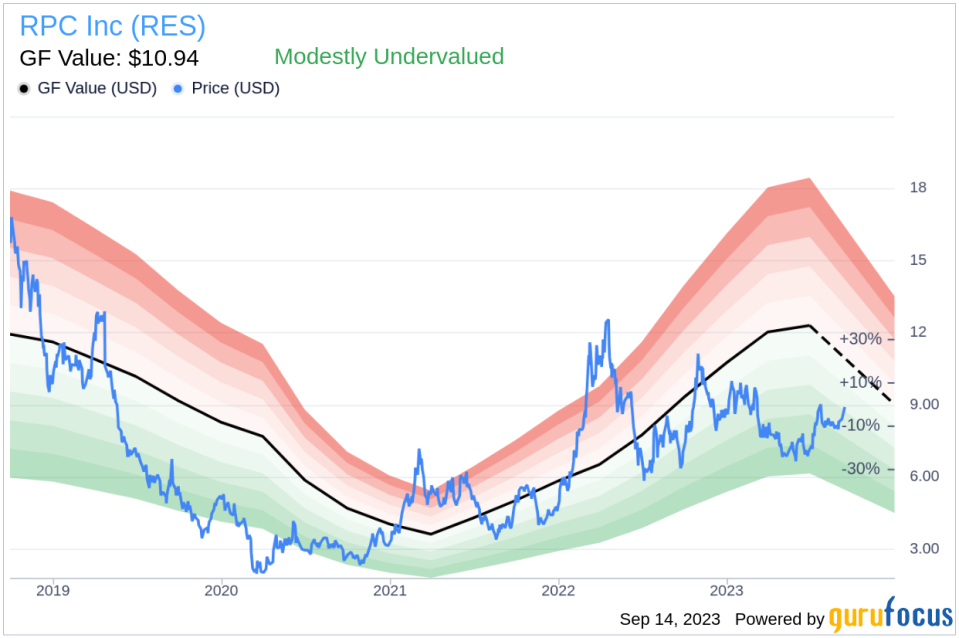

RPC's stock price currently stands at $8.91, while its estimated fair value (GF Value) is $10.94. This discrepancy suggests that the stock might be modestly undervalued. The following analysis will provide a deeper insight into RPC's value.

Understanding GF Value

The GF Value is a proprietary metric that estimates the intrinsic value of a stock. It considers three key factors: historical trading multiples, a GuruFocus adjustment factor based on past performance and growth, and future business performance estimates. The GF Value Line on our summary page gives an overview of the fair value that the stock should be traded at.

According to the GF Value, RPC (NYSE:RES) appears to be modestly undervalued. If the stock price is significantly above the GF Value Line, it suggests overvaluation and potentially poor future returns. Conversely, if the price is significantly below the GF Value Line, it indicates undervaluation and potentially higher future returns. Given RPC's current price of $8.91 per share, the stock seems modestly undervalued.

As a result, the long-term return of RPC's stock is likely to be higher than its business growth due to its relative undervaluation.

Link: These companies may deliever higher future returns at reduced risk.

RPC's Financial Strength

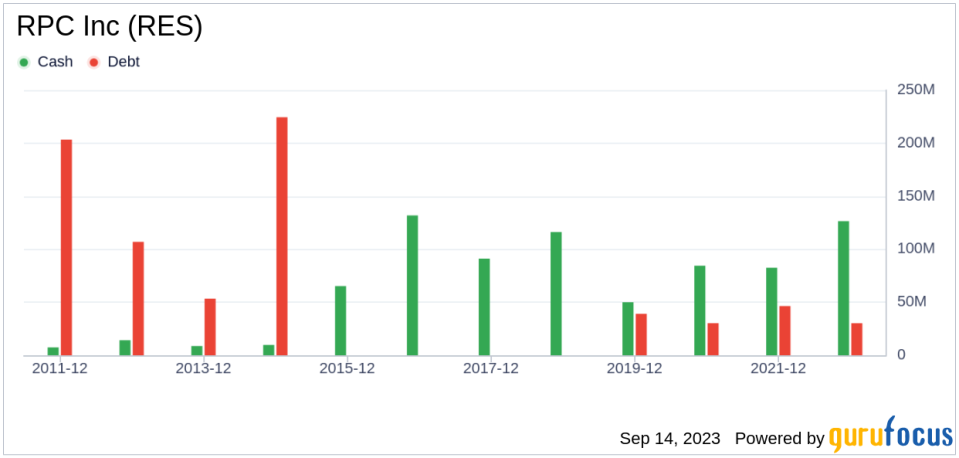

Investing in companies with low financial strength could result in permanent capital loss. Therefore, a company's financial strength should be carefully reviewed before deciding to buy shares. Key indicators such as the cash-to-debt ratio and interest coverage can provide a good initial perspective on the company's financial strength. RPC has a cash-to-debt ratio of 3.5, which ranks better than 71.11% of 1028 companies in the Oil & Gas industry. Based on this, GuruFocus ranks RPC's financial strength as 10 out of 10, suggesting a strong balance sheet.

Profitability and Growth

Investing in profitable companies, especially those with consistent profitability over the long term, poses less risk. RPC has been profitable 6 over the past 10 years. Over the past twelve months, the company had a revenue of $1.80 billion and an Earnings Per Share (EPS) of $1.35. Its operating margin is 20.2%, which ranks better than 66.94% of 974 companies in the Oil & Gas industry. Overall, GuruFocus ranks RPC's profitability at 6 out of 10, indicating fair profitability.

Growth is a crucial factor in a company's valuation. A faster-growing company creates more value for shareholders, especially if the growth is profitable. The 3-year average annual revenue growth of RPC is 9.2%, which ranks worse than 52.39% of 857 companies in the Oil & Gas industry. The 3-year average EBITDA growth rate is 83.9%, which ranks better than 94.05% of 824 companies in the Oil & Gas industry.

ROIC vs WACC

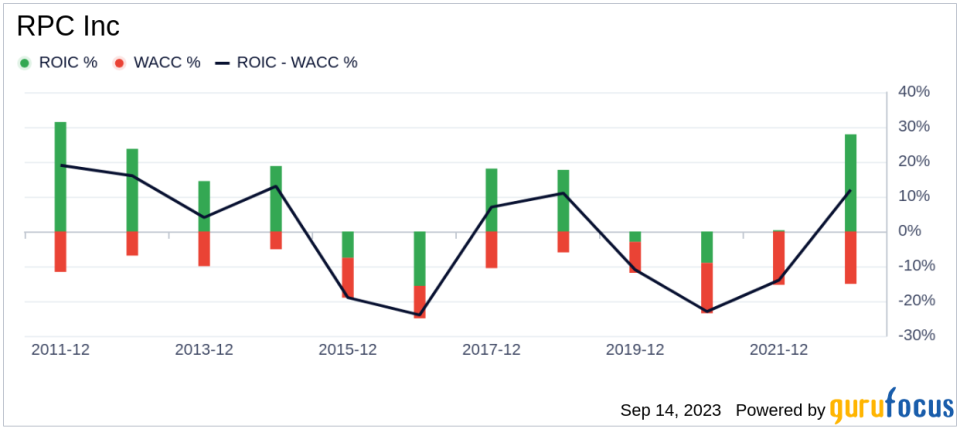

Comparing a company's Return on Invested Capital (ROIC) and the Weighted Average Cost of Capital (WACC) can provide insights into its profitability. ROIC measures how well a company generates cash flow relative to the capital it has invested in its business. WACC is the rate that a company is expected to pay on average to all its security holders to finance its assets. Ideally, ROIC should be higher than WACC. For the past 12 months, RPC's ROIC is 32.88, and its WACC is 11.04.

Conclusion

In conclusion, the stock of RPC (NYSE:RES) shows every sign of being modestly undervalued. The company's financial condition is strong, and its profitability is fair. Its growth ranks better than 94.05% of 824 companies in the Oil & Gas industry. To learn more about RPC stock, you can check out its 30-Year Financials here.

To find out high-quality companies that may deliver above-average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.