Rubicon Technologies, Inc.'s (NYSE:RBT) Share Price Boosted 29% But Its Business Prospects Need A Lift Too

Those holding Rubicon Technologies, Inc. (NYSE:RBT) shares would be relieved that the share price has rebounded 29% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Still, the 30-day jump doesn't change the fact that longer term shareholders have seen their stock decimated by the 87% share price drop in the last twelve months.

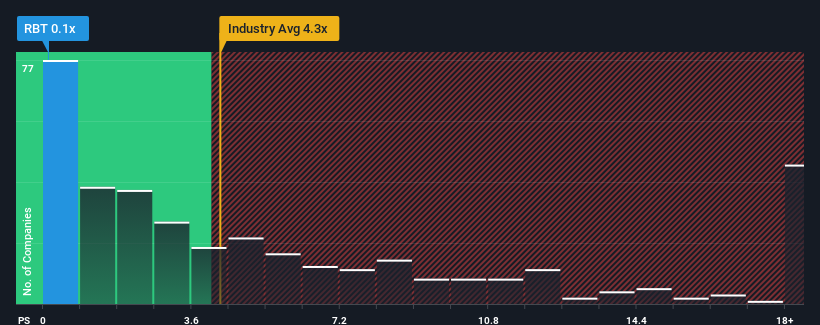

In spite of the firm bounce in price, Rubicon Technologies' price-to-sales (or "P/S") ratio of 0.1x might still make it look like a strong buy right now compared to the wider Software industry in the United States, where around half of the companies have P/S ratios above 4.3x and even P/S above 10x are quite common. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Rubicon Technologies

How Rubicon Technologies Has Been Performing

Rubicon Technologies could be doing better as it's been growing revenue less than most other companies lately. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Rubicon Technologies.

Is There Any Revenue Growth Forecasted For Rubicon Technologies?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like Rubicon Technologies' to be considered reasonable.

Retrospectively, the last year delivered a decent 3.0% gain to the company's revenues. Revenue has also lifted 28% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Shifting to the future, estimates from the three analysts covering the company suggest revenue should grow by 9.5% per annum over the next three years. With the industry predicted to deliver 16% growth per year, the company is positioned for a weaker revenue result.

In light of this, it's understandable that Rubicon Technologies' P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

Shares in Rubicon Technologies have risen appreciably however, its P/S is still subdued. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Rubicon Technologies maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. The company will need a change of fortune to justify the P/S rising higher in the future.

Having said that, be aware Rubicon Technologies is showing 5 warning signs in our investment analysis, and 3 of those are potentially serious.

If you're unsure about the strength of Rubicon Technologies' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.