Salesforce (CRM) Reaffirms FY23 Guidance, Reveals FY26 Target

Salesforce CRM recently reconfirmed its fiscal 2023 guidance and provided a fiscal 2026 financial target during last week’s Investor Day event.

Salesforce restated its revenue guidance range of $30.9-$31 billion for fiscal 2023. Non-GAAP earnings are projected in the $4.71-$4.73 per share band. Operating cash flow growth is likely to be in the 16-17% range year over year. The company reiterated its non-GAAP operating margin forecast for the fiscal year at approximately 20.4%.

On the same day, the company also revealed that it anticipates reaching $50 billion in annual revenues by fiscal 2026, reflecting a CAGR of 17%. The company expects a non-GAAP operating margin for FY26 at more than 25%, driven by reducing non-GAAP sales and marketing expenses as a percentage of total revenues below 35% during the fiscal year.

According to an IDC study, Salesforce and its partners together are likely to create 9.3 million new jobs and $1.6 trillion in new business revenues globally by FY26. With online platforms like Trailblazer Community, Trailhead and Salesforce Talent Alliance, the company is capable of generating both revenues and jobs directly into its customer base. Such platforms are anticipated to aid CRM to achieve massive growth by the end of fiscal 2026.

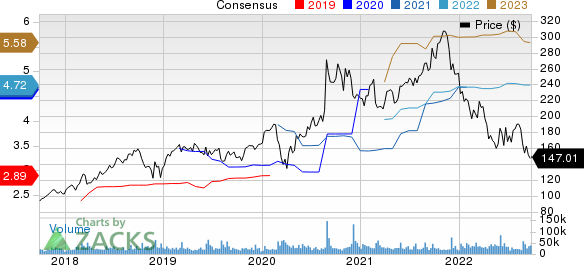

Salesforce Inc. Price and Consensus

Salesforce Inc. price-consensus-chart | Salesforce Inc. Quote

Further, Salesforce plans to authorize the repurchase of up to $10 billion worth of shares for the first time by fiscal 2026 (without any mention of expiration). The company predicts to return 30-40% of free cash flow in fiscal 2026.

Additionally, Salesforce is expecting its total addressable market size to cross $290 billion by 2026, at a CAGR of 13% during the forecast period of 2022-2026. This is likely to accelerate the company’s geographic expansion to a new standard. In this regard, it can be noted that CRM’s management expects the international share of annualized recurring revenues to reach 37% by the end of fiscal 2023.

Currently, Salesforce is benefiting from a robust demand environment as customers are undergoing a major digital transformation. With the rapid adoption of its cloud-based solutions, the company continues to focus on introducing more aligned products as per customer needs. Consecutive deal wins in the international market are another growth driver.

During second-quarter fiscal 2023, Salesforce generated revenues of $7.72 billion, reflecting a 22% year-over-year increase.

Zacks Rank & Stocks to Consider

Currently, Salesforce carries a Zacks Rank #3 (Hold). Shares of CRM lost 47.5% in the past year.

Some better-ranked stocks from the broader Computer and Technology sector are Clearfield CLFD, Silicon Laboratories SLAB and EPAM Systems EPAM. While Clearfield and Silicon Laboratories currently flaunt a Zacks Rank #1 (Strong Buy), EPAM carries a Zacks Rank #2 (Buy). You can see the complete list of today's Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Clearfield's fourth-quarter fiscal 2022 earnings has been revised 10 cents north to 80 cents per share over the past 60 days. For fiscal 2022, earnings estimates have moved 36 cents north to $3.13 per share in the past 60 days.

Clearfield’s earnings beat the Zacks Consensus Estimate in each of the preceding four quarters, the average surprise being 33.9%. Shares of CLFD have improved 97.3% in the past year.

The Zacks Consensus Estimate for Silicon Laboratories’ third-quarter 2022 earnings has increased 36% to $1.13 per share over the past 60 days. For 2022, earnings estimates have moved 20.5% up to $4.41 per share in the past 60 days.

Silicon Laboratories’ earnings beat the Zacks Consensus Estimate in each of the preceding four quarters, the average surprise being 63.6%. Shares of SLAB have declined 15.9% in the past year.

The Zacks Consensus Estimate for EPAM's third-quarter 2022 earnings has been revised 7 cents north to $2.52 per share over the past seven days. For 2022, earnings estimates have moved 15 cents north to $9.96 per share in the past seven days.

EPAM's earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 23%. Shares of the company have declined 39.1% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Salesforce Inc. (CRM) : Free Stock Analysis Report

EPAM Systems, Inc. (EPAM) : Free Stock Analysis Report

Silicon Laboratories, Inc. (SLAB) : Free Stock Analysis Report

Clearfield, Inc. (CLFD) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research