Sally Beauty (NYSE:SBH) Reports Sales Below Analyst Estimates In Q4 Earnings

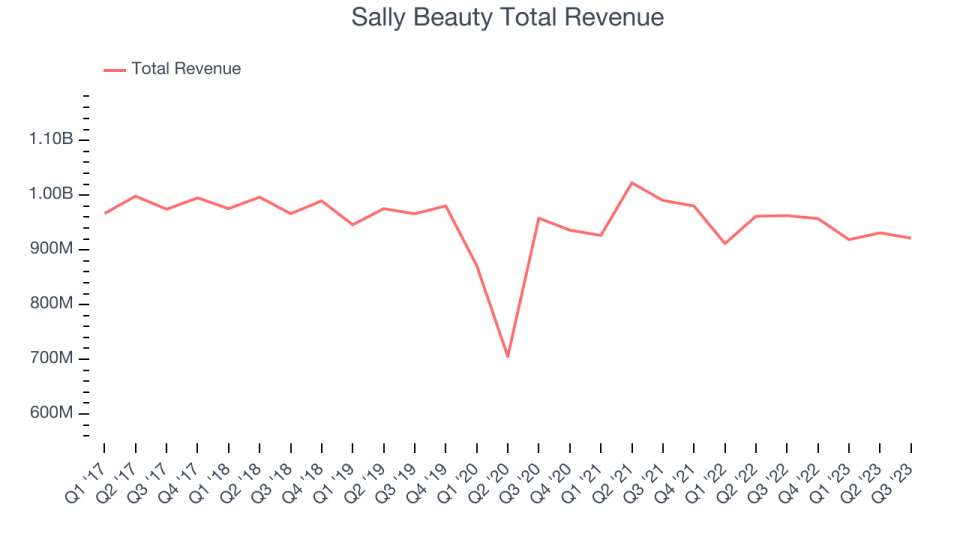

Beauty supply retailer Sally Beauty (NYSE:SBH) fell short of analysts' expectations in Q4 FY2023, with revenue down 4.3% year on year to $921.4 million. Turning to EPS, Sally Beauty made a non-GAAP profit of $0.42 per share, improving from its profit of $0.20 per share in the same quarter last year.

Is now the time to buy Sally Beauty? Find out by accessing our full research report, it's free.

Sally Beauty (SBH) Q4 FY2023 Highlights:

Revenue: $921.4 million vs analyst estimates of $931.2 million (1.1% miss)

EPS (non-GAAP): $0.42 vs analyst expectations of $0.46 (7.8% miss)

Guidance for flat same-store sales next year in FY24 (miss vs. expectations of up 2%)

Free Cash Flow of $89.59 million, up 19.1% from the same quarter last year

Gross Margin (GAAP): 50.6%, up from 50.1% in the same quarter last year

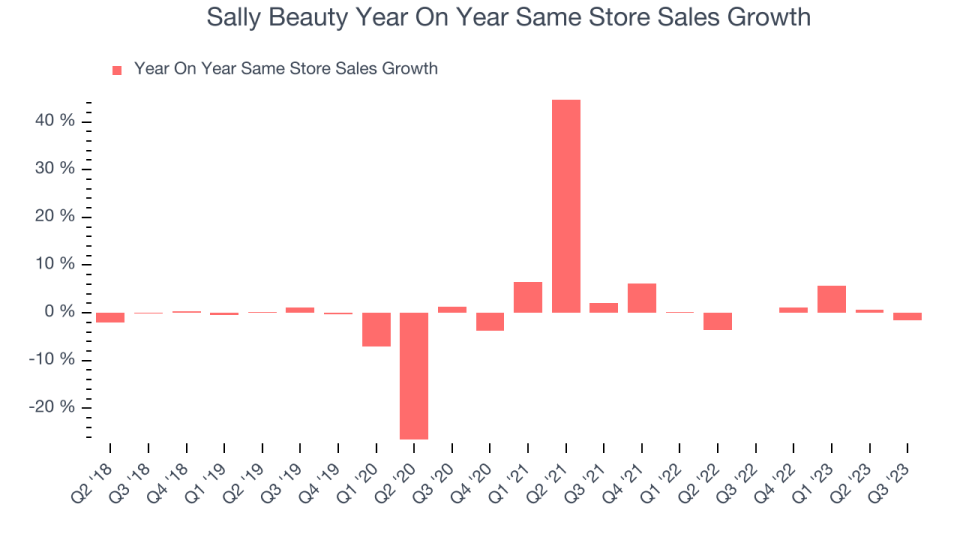

Same-Store Sales were down 1.6% year on year

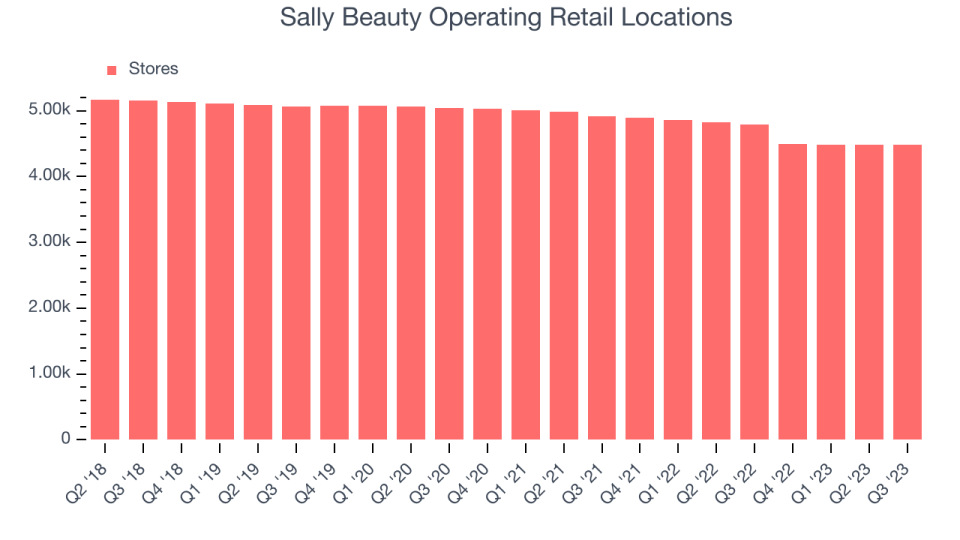

Store Locations: 4,486 at quarter end, decreasing by 308 over the last 12 months

“We are pleased to report full year financial results in line with the expectations we laid out at the beginning of fiscal 2023,” said Denise Paulonis, president and chief executive officer.

Catering to both everyday consumers as well as salon professionals, Sally Beauty (NYSE:SBH) is a retailer that sells salon-quality beauty products such as makeup and haircare products.

Beauty and Cosmetics Retailer

Beauty and cosmetics retailers understand that beauty is in the eye of the beholder, but a little lipstick, nail polish, and glowing skin also help the cause. These stores—which mostly cater to consumers but can also garner the attention of salon pros—aim to be a one-stop personal care and beauty products shop with many brands across many categories. E-commerce is changing how consumers buy cosmetics, so these retailers are constantly evolving to meet the customer where and how they want to shop.

Sales Growth

Sally Beauty is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the other hand, it has an edge over smaller competitors with fewer resources and can still flex high growth rates because it's growing off a smaller base than its larger counterparts.

As you can see below, the company's annualized revenue growth rate over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was flat, or negative 1%, as its store count shrunk.

This quarter, Sally Beauty reported a rather uninspiring 4.3% year-on-year revenue decline, missing Wall Street's expectations. Looking ahead, analysts expect sales to grow 1.5% over the next 12 months.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

The number of stores a retailer operates is a major determinant of how much it can sell, and its growth is a critical driver of how quickly company-level sales can grow.

When a retailer like Sally Beauty is shuttering stores, it usually means that brick-and-mortar demand is less than supply, and the company is responding by closing underperforming locations and possibly shifting sales online. Since last year, Sally Beauty's store count shrank by 308 locations, or 6.4%, to 4,486 total retail locations in the most recently reported quarter.

Taking a step back, the company has generally closed its stores over the last two years, averaging a 5.1% annual decline in its physical footprint. A smaller store base means that the company must rely on higher foot traffic and sales per customer at its remaining stores as well as e-commerce sales to fuel revenue growth.

Same-Store Sales

A company's same-store sales growth shows the year-on-year change in sales for its brick-and-mortar stores that have been open for at least a year, give or take, and e-commerce platform. This is a key performance indicator for retailers because it measures organic growth and demand.

Sally Beauty's demand within its existing stores has been relatively stable over the last eight quarters but fallen behind the broader consumer retail sector. On average, the company's same-store sales have grown by 1.1% year on year. Given its declining store count over the same period, this performance stems from higher e-commerce sales or increased foot traffic at existing stores, which is sometimes a side effect of reducing the total number of stores.

In the latest quarter, Sally Beauty's same-store sales fell 1.6% year on year.

Key Takeaways from Sally Beauty's Q4 Results

Sporting a market capitalization of $876.2 million, Sally Beauty is among smaller companies, but its more than $123 million in cash on hand and positive free cash flow over the last 12 months puts it in an attractive position to invest in growth.

We struggled to find many strong positives in these results. Its same-store sales and revenue unfortunately missed analysts' expectations, leading to an EPS miss. Next year, guidance calls for flat same-store sales, meaning no growth in sales at existing stores. Overall, the results could have been better. The company is down 1.6% on the results and currently trades at $8 per share.

Sally Beauty may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.