Sally Beauty's (NYSE:SBH) Q1 Earnings Results: Revenue In Line With Expectations

Beauty supply retailer Sally Beauty (NYSE:SBH) reported results in line with analysts' expectations in Q1 FY2024, with revenue down 2.7% year on year to $931.3 million. It made a GAAP profit of $0.35 per share, down from its profit of $0.52 per share in the same quarter last year.

Is now the time to buy Sally Beauty? Find out by accessing our full research report, it's free.

Sally Beauty (SBH) Q1 FY2024 Highlights:

Market Capitalization: $1.32 billion

Revenue: $931.3 million vs analyst estimates of $928.6 million (small beat)

EPS: $0.35 vs analyst expectations of $0.37 (4.5% miss)

Free Cash Flow of $20.47 million, down 31.6% from the same quarter last year

Gross Margin (GAAP): 50.2%, down from 50.8% in the same quarter last year

Same-Store Sales were down 0.8% year on year

Store Locations: 4,475 at quarter end, decreasing by 23 over the last 12 months

Catering to both everyday consumers as well as salon professionals, Sally Beauty (NYSE:SBH) is a retailer that sells salon-quality beauty products such as makeup and haircare products.

Beauty and Cosmetics Retailer

Beauty and cosmetics retailers understand that beauty is in the eye of the beholder, but a little lipstick, nail polish, and glowing skin also help the cause. These stores—which mostly cater to consumers but can also garner the attention of salon pros—aim to be a one-stop personal care and beauty products shop with many brands across many categories. E-commerce is changing how consumers buy cosmetics, so these retailers are constantly evolving to meet the customer where and how they want to shop.

Sales Growth

Sally Beauty is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the other hand, it has an edge over smaller competitors with fewer resources and can still flex high growth rates because it's growing off a smaller base than its larger counterparts.

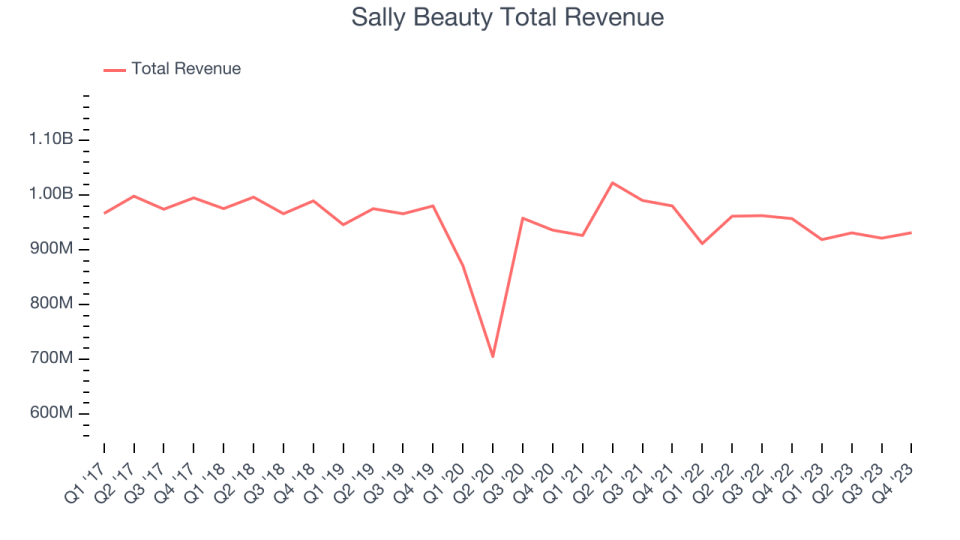

As you can see below, the company's revenue has declined over the last four years, dropping 1.1% annually as its store count shrunk.

This quarter, Sally Beauty reported a rather uninspiring 2.7% year-on-year revenue decline to $931.3 million in revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

It’s not often you find a high-quality company at a significant discount to its historical P/E multiple, but that’s exactly what we found. Click here for your FREE report on this attractive Network Effect stock at a very silly price.

Number of Stores

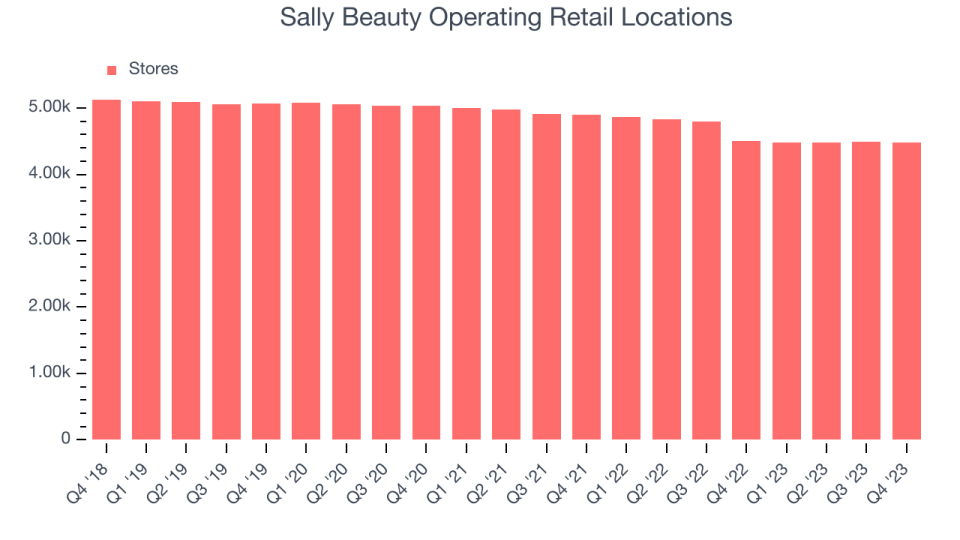

A retailer's store count often determines on how much revenue it can generate.

When a retailer like Sally Beauty is shuttering stores, it usually means that brick-and-mortar demand is less than supply, and the company is responding by closing underperforming locations and possibly shifting sales online. As of the most recently reported quarter, Sally Beauty operated 4,475 total retail locations, in line with its store count a year ago.

Taking a step back, the company has generally closed its stores over the last two years, averaging a 4.8% annual decline in its physical footprint. A smaller store base means that the company must rely on higher foot traffic and sales per customer at its remaining stores as well as e-commerce sales to fuel revenue growth.

Same-Store Sales

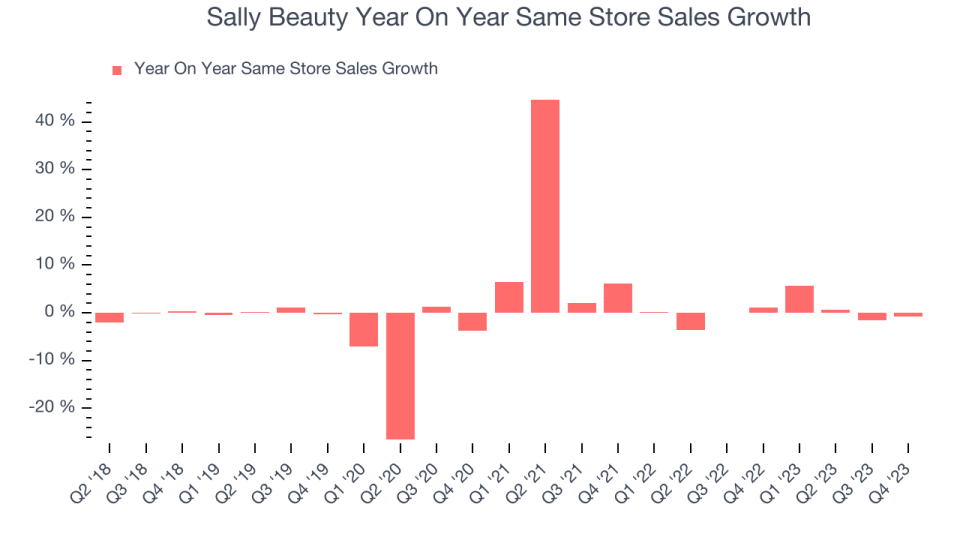

Sally Beauty's demand within its existing stores has barely increased over the last eight quarters. On average, the company's same-store sales growth has been flat.

In the latest quarter, Sally Beauty's year on year same-store sales were flat. By the company's standards, this growth was a meaningful deceleration from the 1.1% year-on-year increase it posted 12 months ago. We'll be watching Sally Beauty closely to see if it can reaccelerate growth.

Key Takeaways from Sally Beauty's Q1 Results

We struggled to find many strong positives in these results. Although its revenue slightly beat estimates, driven by better-than-expected performance in its Beauty Systems Group which contributed to outperformance in its same-store sales, its operating margin and EPS missed Wall Street's expectations. Furthermore, its full-year free cash flow guidance fell short. Overall, the results could have been better. The stock is flat after reporting and currently trades at $12.4 per share.

So should you invest in Sally Beauty right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.