Scorpio Tankers (STNG): A Comprehensive Analysis of Its Market Value

Scorpio Tankers Inc (NYSE:STNG) recently observed a daily gain of 5.56% and a 3-month gain of 15.81%. The company's Earnings Per Share (EPS) stands at 14.35. But does this performance justify its current valuation? Is the stock modestly overvalued? This analysis aims to provide a comprehensive exploration of Scorpio Tankers' intrinsic value. Let's delve into the details.

Introduction to Scorpio Tankers Inc (NYSE:STNG)

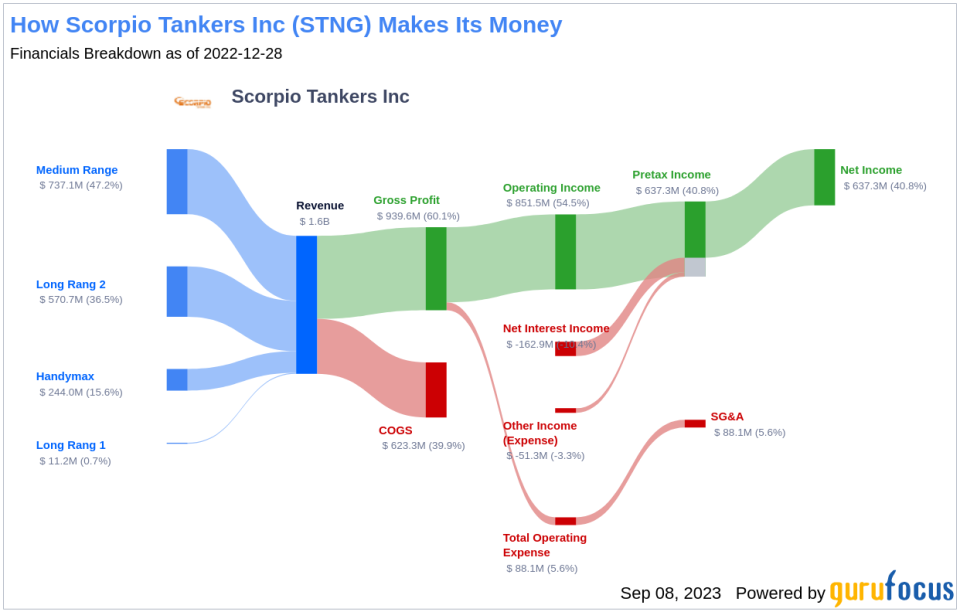

Scorpio Tankers Inc is a leading provider of marine transportation of petroleum products. The company owns, lease finances, or bareboat charters-in 113 product tankers, including 39 LR2 tankers, 60 MR tankers, and 14 Handymax tankers. Scorpio Tankers boasts the largest, newest, and most eco-friendly fleet on the water hauling clean petroleum products.

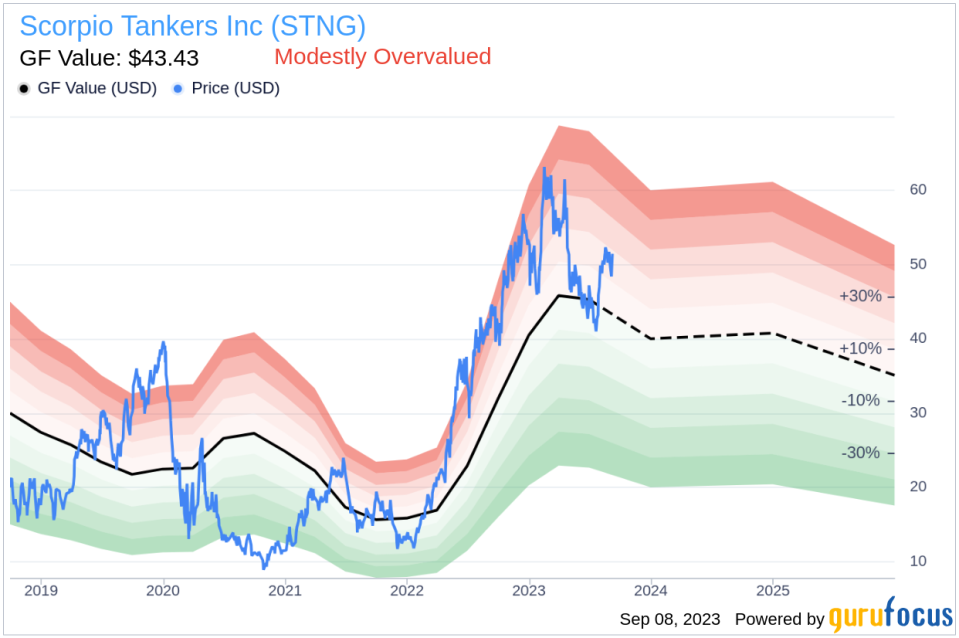

As of September 08, 2023, Scorpio Tankers (NYSE:STNG) trades at $51.48 per share, which is above its fair value (GF Value) of $43.43, suggesting that the stock might be modestly overvalued.

Understanding GF Value

The GF Value is a unique measure of a stock's intrinsic value, derived from historical trading multiples, an internal adjustment factor based on past returns and growth, and future business performance estimates. The GF Value Line provides an overview of the stock's fair trading value.

According to GuruFocus' valuation method, Scorpio Tankers' stock appears to be modestly overvalued. If the share price is significantly above the GF Value Line, the stock may be overpriced, potentially leading to poor future returns. Conversely, if the share price is significantly below the GF Value Line, the stock might be undervalued and could offer higher future returns. Given Scorpio Tankers' current price of $51.48 per share, the stock appears to be modestly overvalued.

Because Scorpio Tankers (NYSE:STNG) is somewhat overvalued, the long-term return of its stock is likely to be lower than its business growth.

Link: These companies may deliver higher future returns at reduced risk.

Assessing Scorpio Tankers' Financial Strength

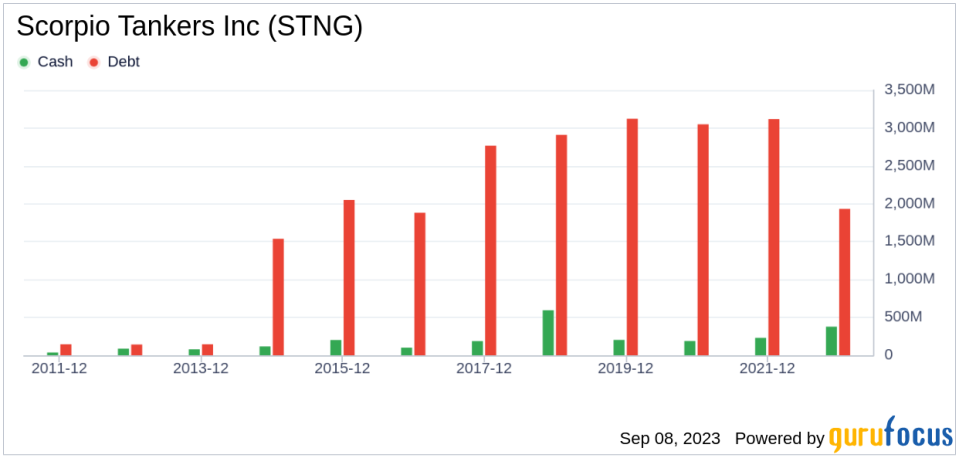

Investing in companies with low financial strength could lead to permanent capital loss. Therefore, it is crucial to carefully review a company's financial strength before purchasing its shares. Scorpio Tankers has a cash-to-debt ratio of 0.17, which ranks worse than 72.28% of 1021 companies in the Oil & Gas industry. Based on this, GuruFocus ranks Scorpio Tankers' financial strength as 6 out of 10, suggesting a fair balance sheet.

Profitability and Growth of Scorpio Tankers

Investing in profitable companies, especially those with consistent profitability over the long term, generally poses less risk. Scorpio Tankers has been profitable 5 years over the past decade. The company's operating margin is 59%, which ranks better than 94.21% of 967 companies in the Oil & Gas industry. Overall, GuruFocus ranks Scorpio Tankers' profitability at 5 out of 10, indicating fair profitability.

Growth is a critical factor in a company's valuation. The faster a company is growing, the more likely it is to be creating value for shareholders, especially if the growth is profitable. Scorpio Tankers' 3-year average annual revenue growth rate is 20.3%, which ranks better than 71.65% of 850 companies in the Oil & Gas industry. The 3-year average EBITDA growth rate is 32.5%, which ranks better than 70.85% of 820 companies in the Oil & Gas industry.

ROIC vs WACC

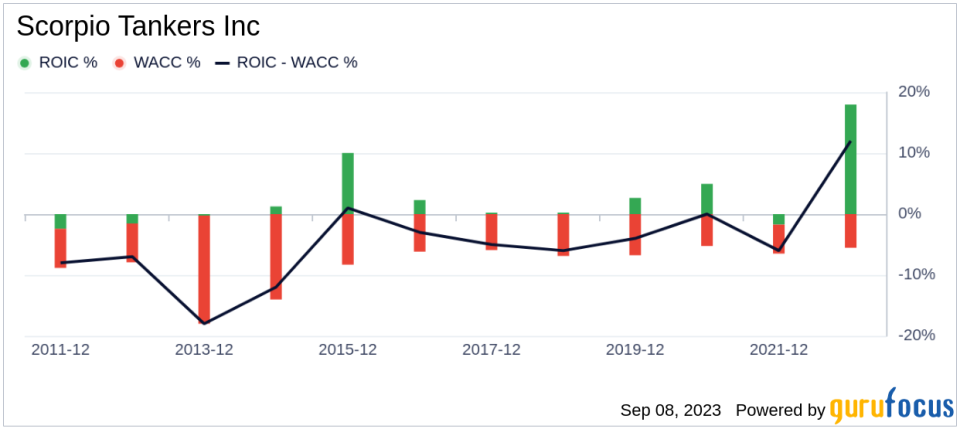

One can evaluate a company's profitability by comparing its return on invested capital (ROIC) to its weighted average cost of capital (WACC). ROIC measures how well a company generates cash flow relative to the capital invested in its business. WACC is the average rate a company is expected to pay its security holders to finance its assets. If ROIC exceeds WACC, the company is likely creating value for its shareholders. In the past 12 months, Scorpio Tankers' ROIC was 23.51, while its WACC was 4.95.

Conclusion

In conclusion, Scorpio Tankers (NYSE:STNG) appears to be modestly overvalued. The company's financial condition is fair, and its profitability is fair. Its growth ranks better than 70.85% of 820 companies in the Oil & Gas industry. For more details about Scorpio Tankers stock, you can check out its 30-Year Financials here.

To find high-quality companies that may deliver above-average returns, please visit the GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.