Scotts Miracle-Gro (SMG) Q3 Earnings & Sales Lag Estimates

The Scotts Miracle-Gro Company SMG reported third-quarter fiscal 2023 (ended Jul 1, 2023) profit of $43.7 million or 77 cents per share against a loss of $443.9 million or $8.01 per share in the year-ago quarter.

Barring one-time items, the adjusted earnings were $1.17 per share, down from $1.98 a year ago. The figure missed the Zacks Consensus Estimate of $1.41.

Net sales fell around 5.7% year over year to $1,118.7 million and missed the consensus mark of $1,160.6 million. The decline in sales was due to lower sales in the Hawthorne segment.

The Scotts Miracle-Gro Company Price, Consensus and EPS Surprise

The Scotts Miracle-Gro Company price-consensus-eps-surprise-chart | The Scotts Miracle-Gro Company Quote

Segment Details

In the fiscal third quarter, net sales in the U.S. Consumer division were up 1% year over year to $916.4 million. It was lower than our estimate of $928.2 million. The segment delivered a profit of $124.8 million, down 31% year over year.

Net sales in the Hawthorne segment tumbled 40% year over year to $93.4 million in the reported quarter. The figure was lower than our estimate of $120 million. The segment reported a loss of $8.7 million, down 312% year over year.

Net sales in the other segment fell 14% year over year to $108.9 million. The segment reported a profit of $5.8 million, down 47%.

Balance Sheet

At the end of the quarter, the company had cash and cash equivalents of $27.4 million, down around 1.4% year over year. Long-term debt was $2,628.8 million, down around 16.7%.

FY2023 Outlook

The company anticipates a roughly 10–11% fall in overall net sales, primarily due to a 2–4% decline in net sales in the U.S. Consumer segment and a 30–35% decrease in net sales in the Hawthorne sector. In addition, the operating income for the year is anticipated to be between 7% and 7.5% of revenues. Taking these changes into account, full-year adjusted EBITDA is anticipated to be around 25% lower than the prior year, and the consequent tax rate will increase to 28 to 29% for the year. Expectations for strong free cash flow generation and interest expense remain unchanged.

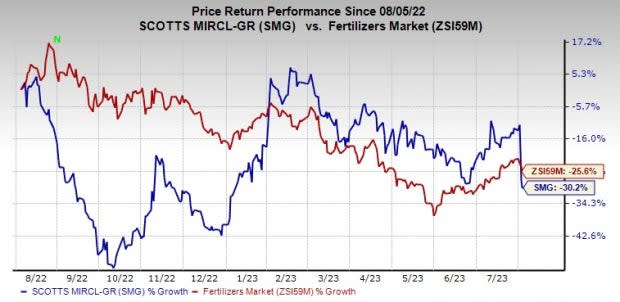

Price Performance

Shares of Scotts Miracle-Gro have lost 30.2% in the past year compared with a 25.6% decline of the industry.

Image Source: Zacks Investment Research

Zacks Rank & Key Picks

Scotts Miracle-Gro currently carries a Zacks Rank #5 (Strong Sell).

Better-ranked stocks worth considering in the basic materials space include PPG Industries Inc. PPG, ATI Inc. ATI and Carpenter Technology Corporation CRS.

PPG, currently carrying a Zacks Rank #2 (Buy), has an expected earnings growth rate of 20.8% for the current fiscal year. The Zacks Consensus Estimate for PPG's earnings for the current fiscal year has been revised 1.6% upward in the past 60 days. It delivered an earnings surprise of 7.3% each of the trailing four quarters, on average. PPG has gained around 9.5% over a year. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

ATI, currently carrying a Zacks Rank #2, has a projected earnings growth rate of 13.1% for the current year. Its earnings beat the Zacks Consensus Estimate in each of the last four quarters. It has a trailing four-quarter earnings surprise of roughly 13%, on average. ATI shares are up around 61.2% in a year.

o

CRS, currently carrying a Zacks Rank #1, has a projected earnings growth rate of 198.11% for the current year. Its earnings beat the Zacks Consensus Estimate in each of the last four quarters. It has a trailing four-quarter earnings surprise of roughly 30.9%, on average. CRS shares are up around 71% in a year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ATI Inc. (ATI) : Free Stock Analysis Report

PPG Industries, Inc. (PPG) : Free Stock Analysis Report

Carpenter Technology Corporation (CRS) : Free Stock Analysis Report

The Scotts Miracle-Gro Company (SMG) : Free Stock Analysis Report