SEMrush (NYSE:SEMR) Posts Q4 Sales In Line With Estimates But Stock Drops

Marketing analytics software Semrush (NYSE:SEMR) reported results in line with analysts' expectations in Q4 FY2023, with revenue up 21.2% year on year to $83.39 million. On the other hand, next quarter's revenue guidance of $85 million was less impressive, coming in 1.3% below analysts' estimates. It made a GAAP profit of $0.05 per share, improving from its loss of $0.10 per share in the same quarter last year.

Is now the time to buy SEMrush? Find out by accessing our full research report, it's free.

SEMrush (SEMR) Q4 FY2023 Highlights:

Revenue: $83.39 million vs analyst estimates of $83.13 million (small beat)

EPS: $0.05 vs analyst estimates of $0.01 ($0.04 beat)

Revenue Guidance for Q1 2024 is $85 million at the midpoint, below analyst estimates of $86.09 million

Management's revenue guidance for the upcoming financial year 2024 is $366 million at the midpoint, missing analyst estimates by 0.8% and implying 19% growth (vs 21.1% in FY2023)

Free Cash Flow of $8.88 million, up 78.9% from the previous quarter

Net Revenue Retention Rate: 107%, in line with the previous quarter

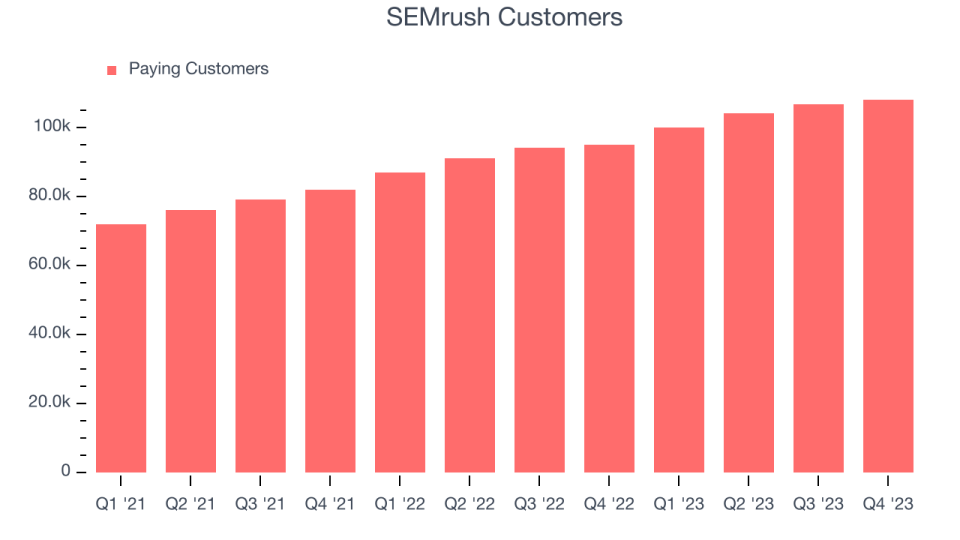

Customers: 108,000, up from 106,800 in the previous quarter

Gross Margin (GAAP): 83.6%, up from 82.6% in the same quarter last year

Market Capitalization: $1.80 billion

“In 2023, we accelerated revenue growth throughout the year, delivering ARR growth of 23%, and strong profitability. In Q4, we reported revenue growth of 21% year-over-year, increased paying customers to nearly 108,000, and our number of free, active customers surpassed one million for the first time. Looking ahead, we remain focused on our three main growth pillars: increasing new user growth, driving expansion by delivering higher value to our customers, and adding new products and monetization to our portfolio to address client needs and market trends. I want to express my sincere gratitude to our growing number of customers, talented employees, and shareholders who showed incredible support and loyalty across our business,” said Oleg Shchegolev, CEO and Co-Founder of Semrush.

Started by Oleg Shchegolev while still in university, Semrush (NYSE:SEMR) is a software as a service platform that helps companies optimize their search engine and content marketing efforts.

Listing Management Software

As the number of places that keep business listings (such as addresses, opening hours and contact details) increases, the task of keeping all listings up-to-date becomes more difficult and that drives demand for centralized solutions that update all touchpoints.

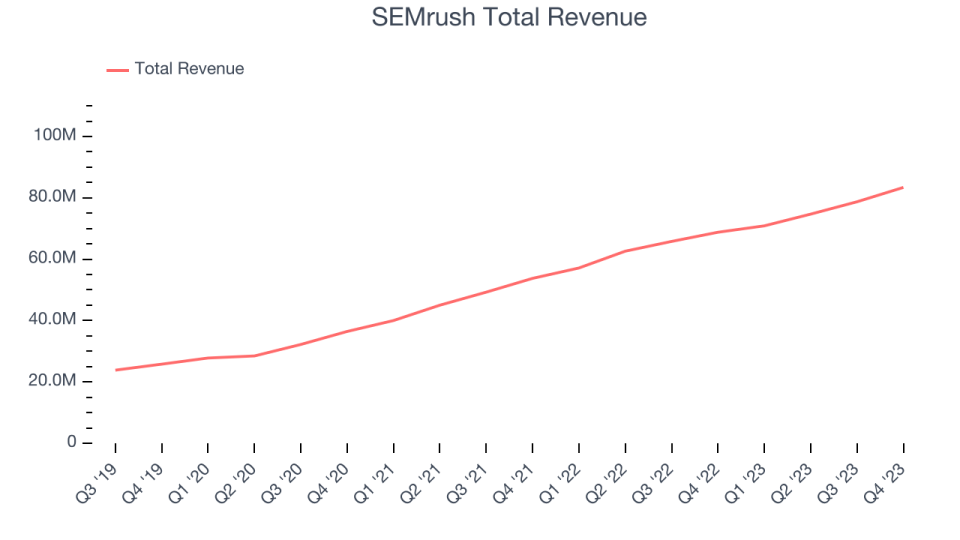

Sales Growth

As you can see below, SEMrush's revenue growth has been strong over the last two years, growing from $53.75 million in Q4 FY2021 to $83.39 million this quarter.

This quarter, SEMrush's quarterly revenue was once again up a very solid 21.2% year on year. On top of that, its revenue increased $4.68 million quarter on quarter, a solid improvement from the $4.03 million increase in Q3 2023. Thankfully, that's a slight re-acceleration of growth.

Next quarter's guidance suggests that SEMrush is expecting revenue to grow 19.9% year on year to $85 million, slowing down from the 24.1% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $366 million at the midpoint, growing 19% year on year compared to the 21% increase in FY2023.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Customer Growth

SEMrush reported 108,000 customers at the end of the quarter, an increase of 1,200 from the previous quarter. , suggesting that the company's customer acquisition momentum is slowing.

Key Takeaways from SEMrush's Q4 Results

It was good to see SEMrush beat analysts' revenue estimates this quarter, but we discount the results as its total number of customers and net revenue retention rate fell short of expectations. Furthermore, its revenue guidance for next quarter and the full year 2024 missed analysts' forecasts. On the bright side, its projected free cash flow margin for 2024 was better than expected.

In the first half of 2024, it expects its new Enterprise Platform to be available to all customers. According to the company, "it has been in a soft launch state since late October 2023 and is currently being used by a select number of large-scale business customers".

Overall, this was a mediocre quarter for SEMrush. The company is down 9.2% on the results and currently trades at $11.81 per share.

SEMrush may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.