Is Semtech Corporation's (NASDAQ:SMTC) Liquidity Good Enough?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Small-cap and large-cap companies receive a lot of attention from investors, but mid-cap stocks like Semtech Corporation (NASDAQ:SMTC), with a market cap of US$3.6b, are often out of the spotlight. While they are less talked about as an investment category, mid-cap risk-adjusted returns have generally been better than more commonly focused stocks that fall into the small- or large-cap categories. Today we will look at SMTC’s financial liquidity and debt levels, which are strong indicators for whether the company can weather economic downturns or fund strategic acquisitions for future growth. Note that this commentary is very high-level and solely focused on financial health, so I suggest you dig deeper yourself into SMTC here.

See our latest analysis for Semtech

Does SMTC Produce Much Cash Relative To Its Debt?

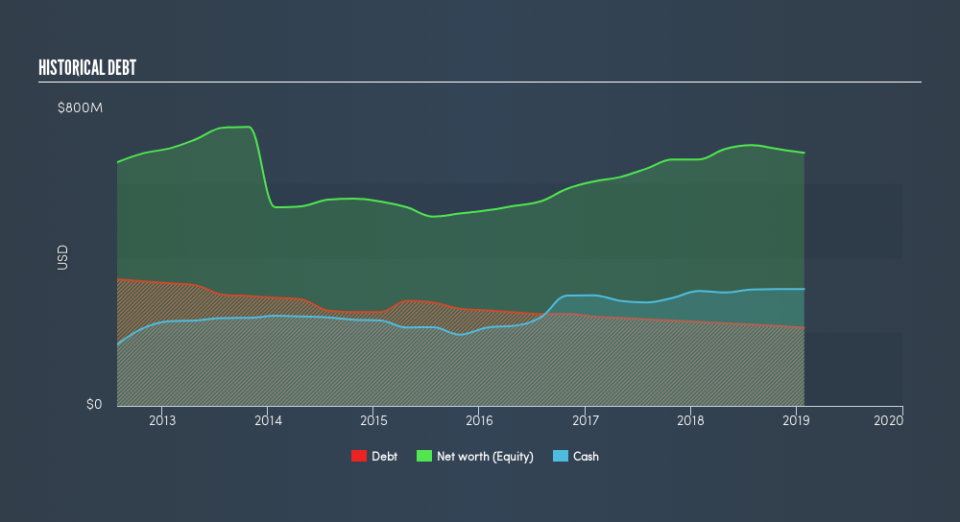

Over the past year, SMTC has reduced its debt from US$227m to US$211m , which includes long-term debt. With this debt payback, SMTC's cash and short-term investments stands at US$315m to keep the business going. Moreover, SMTC has produced cash from operations of US$184m during the same period of time, leading to an operating cash to total debt ratio of 87%, indicating that SMTC’s debt is appropriately covered by operating cash.

Does SMTC’s liquid assets cover its short-term commitments?

With current liabilities at US$130m, the company has maintained a safe level of current assets to meet its obligations, with the current ratio last standing at 3.74x. The current ratio is calculated by dividing current assets by current liabilities. Having said that, a ratio greater than 3x may be considered by some to be quite high, however this is not necessarily a negative for the company.

Does SMTC face the risk of succumbing to its debt-load?

SMTC’s level of debt is appropriate relative to its total equity, at 31%. This range is considered safe as SMTC is not taking on too much debt obligation, which can be restrictive and risky for equity-holders. We can check to see whether SMTC is able to meet its debt obligations by looking at the net interest coverage ratio. A company generating earnings before interest and tax (EBIT) at least three times its net interest payments is considered financially sound. In SMTC's, case, the ratio of 8.88x suggests that interest is appropriately covered, which means that debtors may be willing to loan the company more money, giving SMTC ample headroom to grow its debt facilities.

Next Steps:

SMTC’s high cash coverage and appropriate debt levels indicate its ability to utilise its borrowings efficiently in order to generate ample cash flow. Furthermore, the company exhibits proper management of current assets and upcoming liabilities. Keep in mind I haven't considered other factors such as how SMTC has been performing in the past. I recommend you continue to research Semtech to get a more holistic view of the stock by looking at:

Future Outlook: What are well-informed industry analysts predicting for SMTC’s future growth? Take a look at our free research report of analyst consensus for SMTC’s outlook.

Valuation: What is SMTC worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether SMTC is currently mispriced by the market.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.