Shareholders May Not Be So Generous With Quickstep Holdings Limited's (ASX:QHL) CEO Compensation And Here's Why

In the past three years, the share price of Quickstep Holdings Limited (ASX:QHL) has struggled to grow and now shareholders are sitting on a loss. Despite positive EPS growth in the past few years, the share price hasn't tracked the fundamental performance of the company. Shareholders may want to question the board on the future direction of the company at the upcoming AGM on 18 November 2021. They could also try to influence management and firm direction through voting on resolutions such as executive remuneration and other company matters. We think shareholders might be reluctant to increase compensation for the CEO at the moment, according to our analysis below.

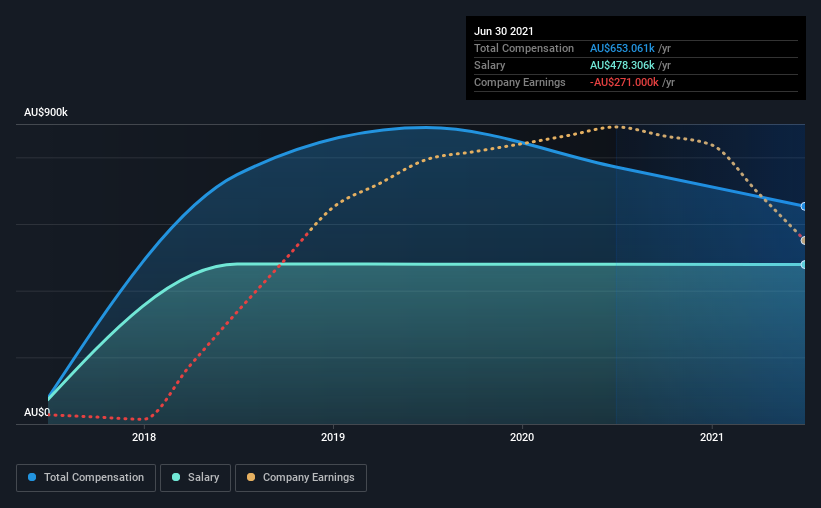

See our latest analysis for Quickstep Holdings

Comparing Quickstep Holdings Limited's CEO Compensation With the industry

At the time of writing, our data shows that Quickstep Holdings Limited has a market capitalization of AU$38m, and reported total annual CEO compensation of AU$653k for the year to June 2021. Notably, that's a decrease of 15% over the year before. In particular, the salary of AU$478.3k, makes up a huge portion of the total compensation being paid to the CEO.

On comparing similar-sized companies in the industry with market capitalizations below AU$272m, we found that the median total CEO compensation was AU$464k. Hence, we can conclude that Mark Burgess is remunerated higher than the industry median. Moreover, Mark Burgess also holds AU$223k worth of Quickstep Holdings stock directly under their own name.

Component | 2021 | 2020 | Proportion (2021) |

Salary | AU$478k | AU$479k | 73% |

Other | AU$175k | AU$292k | 27% |

Total Compensation | AU$653k | AU$771k | 100% |

Speaking on an industry level, nearly 64% of total compensation represents salary, while the remainder of 36% is other remuneration. Quickstep Holdings pays out 73% of remuneration in the form of a salary, significantly higher than the industry average. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Quickstep Holdings Limited's Growth Numbers

Quickstep Holdings Limited has seen its earnings per share (EPS) increase by 41% a year over the past three years. Its revenue is up 3.5% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's also good to see modest revenue growth, suggesting the underlying business is healthy. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Quickstep Holdings Limited Been A Good Investment?

With a total shareholder return of -30% over three years, Quickstep Holdings Limited shareholders would by and large be disappointed. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

Despite the growth in its earnings, the share price decline in the past three years is certainly concerning. The fact that the stock price hasn't grown along with earnings may indicate that other issues may be affecting that stock. If there are some unknown variables that are influencing the stock's price, surely shareholders would have some concerns. At the upcoming AGM, shareholders will get the opportunity to discuss any issues with the board, including those related to CEO remuneration and assess if the board's plan will likely improve performance in the future.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We did our research and spotted 1 warning sign for Quickstep Holdings that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.