Shareholders Should Be Pleased With EcoSynthetix Inc.'s (TSE:ECO) Price

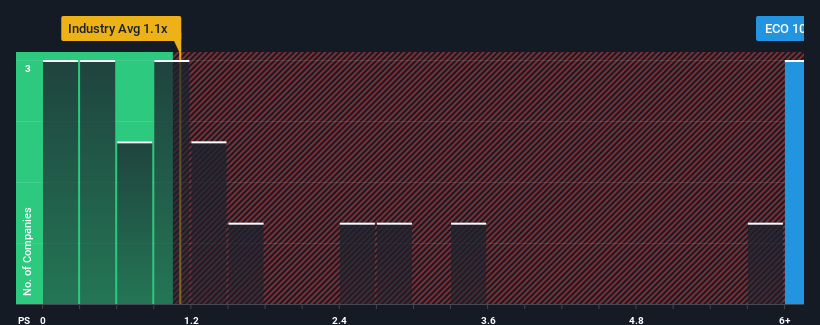

When you see that almost half of the companies in the Chemicals industry in Canada have price-to-sales ratios (or "P/S") below 1.1x, EcoSynthetix Inc. (TSE:ECO) looks to be giving off strong sell signals with its 10.4x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for EcoSynthetix

What Does EcoSynthetix's Recent Performance Look Like?

As an illustration, revenue has deteriorated at EcoSynthetix over the last year, which is not ideal at all. Perhaps the market believes the company can do enough to outperform the rest of the industry in the near future, which is keeping the P/S ratio high. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Although there are no analyst estimates available for EcoSynthetix, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.

How Is EcoSynthetix's Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like EcoSynthetix's to be considered reasonable.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 16%. This has erased any of its gains during the last three years, with practically no change in revenue being achieved in total. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

In contrast to the company, the rest of the industry is expected to decline by 5.7% over the next year, which puts the company's recent medium-term positive growth rates in a good light for now.

With this information, we can see why EcoSynthetix is trading at a high P/S compared to the industry. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the industry. However, its current revenue trajectory will be very difficult to maintain against the headwinds other companies are facing at the moment.

The Bottom Line On EcoSynthetix's P/S

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We see that EcoSynthetix justifiably maintains its high P/S on the merits of its recentthree-year revenue growth beating forecasts amidst struggling industry. Right now shareholders are comfortable with the P/S as they are quite confident revenues aren't under threat. Our only concern is whether its revenue trajectory can keep outperforming under these tough industry conditions. If things remain consistent though, shareholders shouldn't expect any major share price shocks in the near term.

Before you take the next step, you should know about the 2 warning signs for EcoSynthetix (1 is a bit concerning!) that we have uncovered.

If these risks are making you reconsider your opinion on EcoSynthetix, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.