Shineco (SISI): A Hidden Gem or a Value Trap?

Value-focused investors are always on the hunt for stocks that are priced below their intrinsic value. One such stock that merits attention is Shineco Inc (NASDAQ:SISI). The stock, which is currently priced at 0.15, recorded a loss of 9.75% in a day and a 3-month decrease of 70.75%. The stock's fair valuation is $0.54, as indicated by its GF Value.

Understanding GF Value

The GF Value represents the current intrinsic value of a stock derived from our exclusive method. The GF Value Line on our summary page gives an overview of the fair value that the stock should be traded at. It is calculated based on three factors:

Historical multiples (PE Ratio, PS Ratio, PB Ratio and Price-to-Free-Cash-Flow) that the stock has traded at.

GuruFocus adjustment factor based on the company's past returns and growth.

Future estimates of the business performance.

We believe the GF Value Line is the fair value that the stock should be traded at. The stock price will most likely fluctuate around the GF Value Line. If the stock price is significantly above the GF Value Line, it is overvalued and its future return is likely to be poor. On the other hand, if it is significantly below the GF Value Line, its future return will likely be higher.

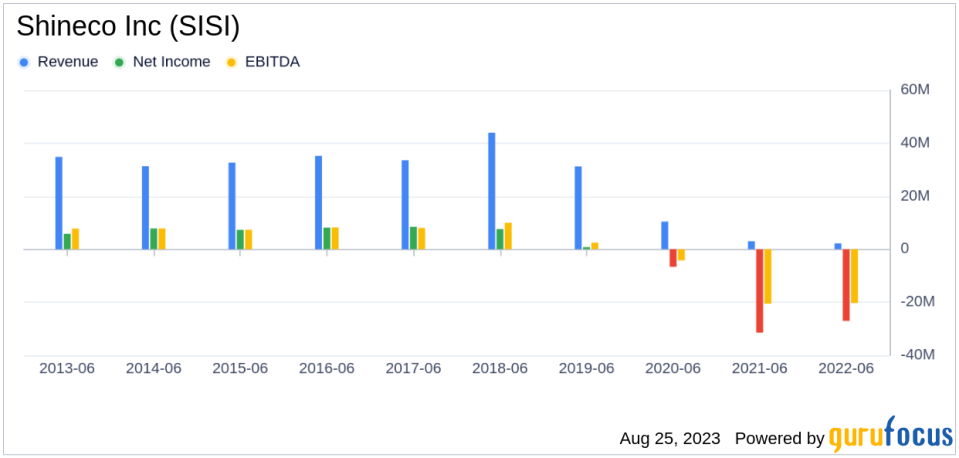

However, investors need to consider a more in-depth analysis before making an investment decision. Despite its seemingly attractive valuation, certain risk factors associated with Shineco should not be ignored. These risks are primarily reflected through its low Altman Z-score of -0.69, and a Beneish M-Score of 16.7 that exceeds -1.78, the threshold for potential earnings manipulation. the company's revenues and earnings have been on a downward trend over the past five years, which raises a crucial question: Is Shineco a hidden gem or a value trap?

These indicators suggest that Shineco, despite its apparent undervaluation, might be a potential value trap. This complexity underlines the importance of thorough due diligence in investment decision-making.

Understanding the Altman Z-Score and Beneish M-Score

Before delving into the details, let's understand what the Altman Z-score entails. Invented by New York University Professor Edward I. Altman in 1968, the Z-Score is a financial model that predicts the probability of a company entering bankruptcy within a two-year time frame. The Altman Z-Score combines five different financial ratios, each weighted to create a final score. A score below 1.8 suggests a high likelihood of financial distress, while a score above 3 indicates a low risk.

Developed by Professor Messod Beneish, the Beneish M-Score is based on eight financial variables that reflect different aspects of a company's financial performance and position. These are Days Sales Outstanding (DSO), Gross Margin (GM), Total Long-term Assets Less Property, Plant and Equipment over Total Assets (TATA), change in Revenue (?REV), change in Depreciation and Amortization (?DA), change in Selling, General and Admin expenses (?SGA), change in Debt-to-Asset Ratio (?LVG), and Net Income Less Non-Operating Income and Cash Flow from Operations over Total Assets (?NOATA).

Company Introduction

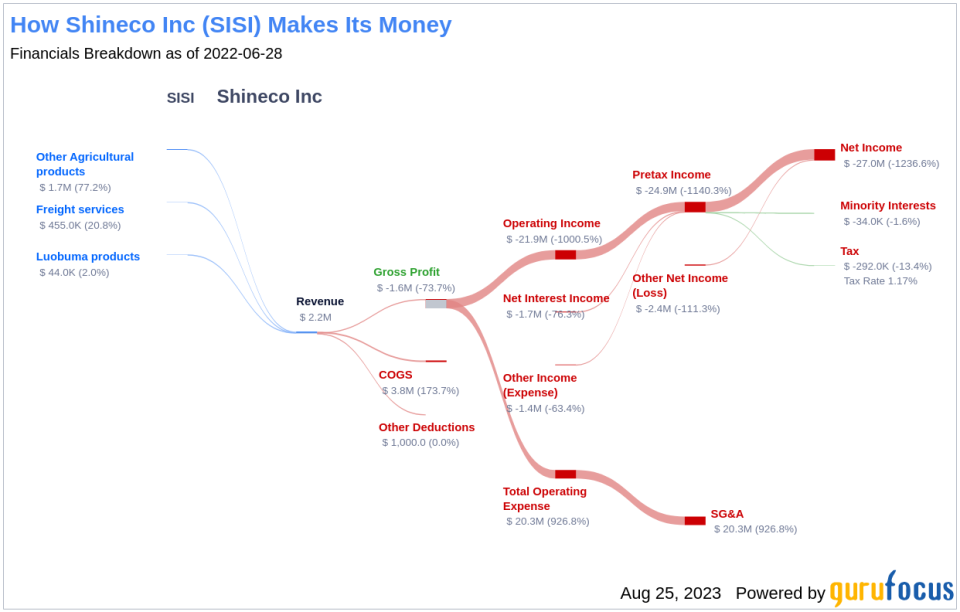

Shineco Inc, through its subsidiaries, produces, distributes, and sells health and well-being focused plant-based products under the Tenethealth and Tenet Bojian brands in China. It operates through Luobuma products; Other agricultural products and Freight services segment. The company generates maximum revenue from the Other agricultural products segment. Despite its seemingly attractive valuation, Shineco's stock price is currently below its fair GF Value, indicating potential undervaluation. However, a deeper analysis reveals certain risk factors that investors should consider before making an investment decision.

Shineco's Low Altman Z-Score: A Breakdown of Key Drivers

A dissection of Shineco's Altman Z-score reveals Shineco's financial health may be weak, suggesting possible financial distress:

The first factor we need to consider is a measure of short-term liquidity. This is calculated as the working capital divided by total assets. When we evaluate the data provided: 2021: 0.05; 2022: -0.01; 2023: 0.00, it's clear that Shineco has experienced a declining trend in its Working Capital to Total Assets ratio over the past few years. This decline suggests potential liquidity issues that the company may be facing. The ratio is strikingly low, which unfavorably influences the overall Z-Score.

The Retained Earnings to Total Assets ratio provides insights into a company's capability to reinvest its profits or manage debt. Evaluating Shineco's historical data, 2021: 0.27; 2022: -0.16; 2023: -0.39, we observe a declining trend in this ratio. This downward movement indicates Shineco's diminishing ability to reinvest in its business or effectively manage its debt. Consequently, it exerts a negative impact on its Z-Score.

The EBIT to Total Assets ratio serves as a crucial barometer of a company's operational effectiveness, correlating earnings before interest and taxes (EBIT) to total assets. An analysis of Shineco's EBIT to Total Assets ratio from historical data (2021: -0.15; 2022: -0.38; 2023: -0.21) indicates a descending trend. This reduction suggests that Shineco might not be utilizing its assets to their full potential to generate operational profits, which could be negatively affecting the company's overall Z-score.

The Bearish Signs: Declining Revenues and Earnings

One of the telltale indicators of a company's potential trouble is a sustained decline in revenues. In the case of Shineco, both the revenue per share (evident from the last five years' TTM data: 2019: 13.19; 2020: 9.41; 2021: -1.93; 2022: 0.29; 2023: 0.12; ) and the 5-year revenue growth rate (-59.8%) have been on a consistent downward trajectory. This pattern may point to underlying challenges such as diminishing demand for Shineco's products, or escalating competition in its market sector. Either scenario can pose serious risks to the company's future performance, warranting a thorough analysis by investors.

The Red Flag: Sluggish Earnings Growth

Despite its low price-to-fair-value ratio, Shineco's falling revenues and earnings cast a long shadow over its investment attractiveness. A low price relative to intrinsic value can indeed suggest an investment opportunity, but only if the company's fundamentals are sound or improving. In Steelcase's case, the declining revenues, EBITDA, and earnings growth suggest that the company's issues may be more than just cyclical fluctuations.

Without a clear turnaround strategy, there's a risk that the company's performance could continue to deteriorate, leading to further price declines. In such a scenario, the low price-to-GF-Value ratio may be more indicative of a value trap than a value opportunity.

Conclusion

In conclusion, despite Shineco's seemingly attractive valuation, its declining revenues, earnings, and low Altman Z-Score suggest that the company might be a potential value trap. Therefore, investors should exercise caution and conduct thorough due diligence before making an investment decision.

GuruFocus Premium members can find stocks with high Altman Z-Score using the following Screener: Walter Schloss Screen .To find out the high quality companies that may deliever above average returns, please check out GuruFocus High Quality Low Capex Screener.Investors can find stocks with good revenue and earnings growth using GuruFocus' Peter Lynch Growth with Low Valuation Screener.

This article first appeared on GuruFocus.