Signet (SIG) Stock is Rallying Ahead of Industry: Here's Why

Signet Jewelers Limited SIG has been making constant efforts to enrich customers’ experience. The company is focused on making digital endeavors and smooth progress in its Inspiring Brilliance strategy. It has been integrating its physical stores with advanced virtual experiences through data-driven in-store consultations and services like buy online pickup in-store and curbside options.

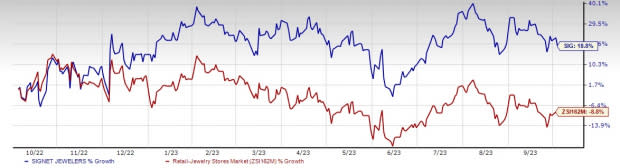

Thanks to the aforesaid endeavors, shares of this jewelry retailer have gained 18.8% over the past year against the industry’s 8.8% decline. A VGM Score of A for this Zacks Rank #3 (Hold) company further speaks volumes.

Let’s Delve Deeper

Signet’s connected commerce strategy helps in combining customer experiences, leveraging in store and online as well as mobile and ubiquitous delivery. This is helping the company cater to customers’ needs more aptly. Management highlighted that growth in the digital realm bears testimony to the success of the company’s connected commerce strategy.

As part of the company’s fleet-optimization endeavors, management expects closing up to 150 stores in the next 12 months. Nearly 90% of the closures will be in mall locations and/or are among the low-performing outlets across the UK market. It also projects opening between 30 stores and35 stores, mainly Kay, Jared and Diamond Direct locations. Management expects capital investments to be up to $200 million, along with investments in banner differentiation with stores, connected-commerce capabilities, and digital and technology upgrades.

Image Source: Zacks Investment Research

Further, the company’s loyalty program is progressing well. It has introduced the option to enroll in the loyalty program when first making an account on one of its banner sites, thus creating a frictionless point of entry for the customers. Also, the company has implemented more than a dozen new priority feature launches. These features consist of the enhancements to online merchandise presentation, messaging, appointment booking and services. Such efforts indicate that Signet has been focusing on evolving its channel-agnostic retailer capabilities.

The company remains focused on enhancing its data- analytics capabilities with higher precision. It is leveraging the analytics capability to optimize the way of adding product assortments. Markedly, the company had added several features and capabilities across its digital platform to offer a seamless customer experience. It has rolled out Google Business Messages and Apple Business Chat features, which allow customers to engage with virtual jewelry consultants in real time or offline from search results or maps. The company has been offering curbside pickup and virtual consultations and buy online pick up in store in various locations.

Analysts seem optimistic about the company. The Zacks Consensus Estimate for fiscal 2025 sales and earnings per share (EPS) is currently pegged at $7.37 billion and $10.38, respectively. These estimates show corresponding increases of 1.9% and 5% year over year.

Solid Picks in Retail

We have highlighted three better-ranked stocks, namely American Eagle Outfitters AEO, Urban Outfitters URBN and Boot Barn BOOT.

American Eagle Outfitters, a retailer of casual apparel, accessories and footwear, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for American Eagle Outfitters’ current financial-year EPS suggests growth of 33%, from the year-ago reported figure. AEO delivered an average trailing four-quarter earnings surprise of 43.2%.

Urban Outfitters, a sporting goods retailer, presently sports a Zacks Rank of 1. The company has an average trailing four-quarter earnings surprise of 12.2%.

The consensus estimate for Urban Outfitters’ current financial-year sales and EPS suggests growth of 5.3% and 60.6%, respectively, from the year-ago reported figures.

Boot Barn, a leading apparel and footwear retailer, currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Boot Barn’s current financial-year sales suggests growth of 7.8% from the year-ago reported figure. BOOT delivered an average trailing four-quarter earnings surprise of 13.5%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

American Eagle Outfitters, Inc. (AEO) : Free Stock Analysis Report

Urban Outfitters, Inc. (URBN) : Free Stock Analysis Report

Signet Jewelers Limited (SIG) : Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT) : Free Stock Analysis Report