Spotlight on Encore Capital's (ECPG) Q4 Earnings Drivers

Encore Capital Group, Inc. ECPG is set to report its fourth-quarter 2023 results on Feb 21, after the closing bell. It is expected to have witnessed increased top line and profits in the December quarter.

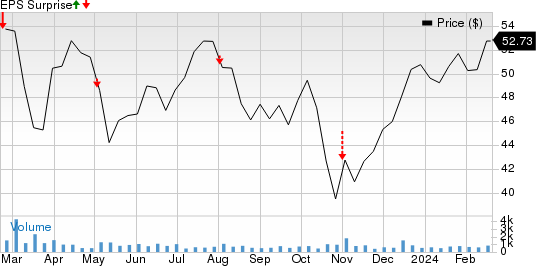

Earnings Surprise History

Encore Capital’s earnings missed the consensus estimate in all the prior four quarters, with the average surprise being negative 97.9%. This is depicted in the graph below:

Encore Capital Group Inc Price and EPS Surprise

Encore Capital Group Inc price-eps-surprise | Encore Capital Group Inc Quote

In the last reported quarter, the international specialty finance company reported adjusted operating earnings per share of 79 cents, missing the Zacks Consensus Estimate by 41.5% due to higher operating expenses and lower Servicing revenues. The negatives were partially offset by stable collections performance and improved portfolio pricing.

Now, let’s see how things have shaped up prior to the fourth-quarter earnings announcement.

Q4 Factors to Note

The Zacks Consensus Estimate for fourth-quarter revenues from receivable portfolios is pegged at almost $304 million, signaling a 3.1% year-over-year jump. The consensus mark also indicates 46.4% growth in other revenues in the quarter under review.

These are likely to have boosted ECPG’s top line. The consensus estimate for fourth-quarter revenues of $330.8 million indicates a 41.4% increase from the year-ago reported figure. Growing credit card lending and charge-off rates are likely to have benefited U.S. portfolio supply. This is expected to have aided its portfolio pricing and returns.

Higher global collections due to normalizing consumer behavior and a steady collections environment are likely to have aided the company. The Zacks Consensus Estimate for fourth-quarter global collections is pegged at $467.3 million, indicating 7.1% year-over-year growth.

The above-mentioned factors are likely to have positioned the company for year-over-year growth. The Zacks Consensus Estimate for fourth-quarter earnings per share of $1.22 suggests a 139.2% increase from the prior-year level. The estimate remained stable over the past week.

However, the company is expected to have encountered higher operating expenses due to increased salaries and employee benefits, cost of legal collections and collection agency commissions, partially offsetting the upside and making an earnings beat uncertain.

Also, the Zacks Consensus Estimate for Servicing revenues in the fourth quarter indicates a 4.3% decline from the year-ago period. The competitive portfolio purchasing market in Europe is likely to have acted as a constraint for the company. This, in turn, is likely to have forced ECPG to reallocate capital to the U.S. market.

Earnings Whispers

Our proven model does not conclusively predict an earnings beat for Encore Capital this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. That is not the case here, as you will see below.

Earnings ESP: The company currently has an Earnings ESP of 0.00%. This is because the Most Accurate Estimate currently stands at an earnings of $1.22 per share, in line with the Zacks Consensus Estimate.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: Encore Capital currently carries a Zacks Rank #3.

You can see the complete list of today’s Zacks #1 Rank stocks here.

How Other Stocks Performed

Here are some companies from the broader Finance space that have already reported earnings for the December quarter: PRA Group, Inc. PRAA, Rithm Capital Corp. RITM and Virtu Financial, Inc. VIRT.

PRA Group incurred a fourth-quarter 2023 loss of 22 cents per share, narrower than the Zacks Consensus Estimate of a loss of 35 cents per share, thanks to robust portfolio income, growing cash collection, improving pricing and better operational results in Brazil and Europe. However, the upside was partially offset by increased expenses and weakness in PRAA’s U.S. business.

Rithm Capital reported fourth-quarter 2023 adjusted earnings of 51 cents per share, which outpaced the Zacks Consensus Estimate by a whopping 45.7%, thanks to improved asset management revenues and continuous acquisition of customer loans. RITM’s results were partially offset by an elevated expense level, lower net servicing revenues and interest income.

Virtu Financial reported fourth-quarter 2023 adjusted earnings per share of 27 cents, which missed the Zacks Consensus Estimate by 35.7%, due to deterioration in net trading income and commissions, net and technology service revenues and higher expenses. However, VIRT’s results were somewhat supported by improved interest and dividend income.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PRA Group, Inc. (PRAA) : Free Stock Analysis Report

Encore Capital Group Inc (ECPG) : Free Stock Analysis Report

Virtu Financial, Inc. (VIRT) : Free Stock Analysis Report

Rithm Capital Corp. (RITM) : Free Stock Analysis Report