Steris PLC (STE): A Hidden Bargain or Overpriced Asset? An In-Depth Look at Its Valuation

Steris PLC (NYSE:STE) experienced a daily loss of -2.39%, with a 3-month gain of 0.71%. Its Earnings Per Share (EPS) stands at 1.22. This raises the question: is the stock modestly undervalued? In this analysis, we will explore Steris PLC's valuation, financial strength, profitability, and growth. Let's dive into the details.

Company Overview

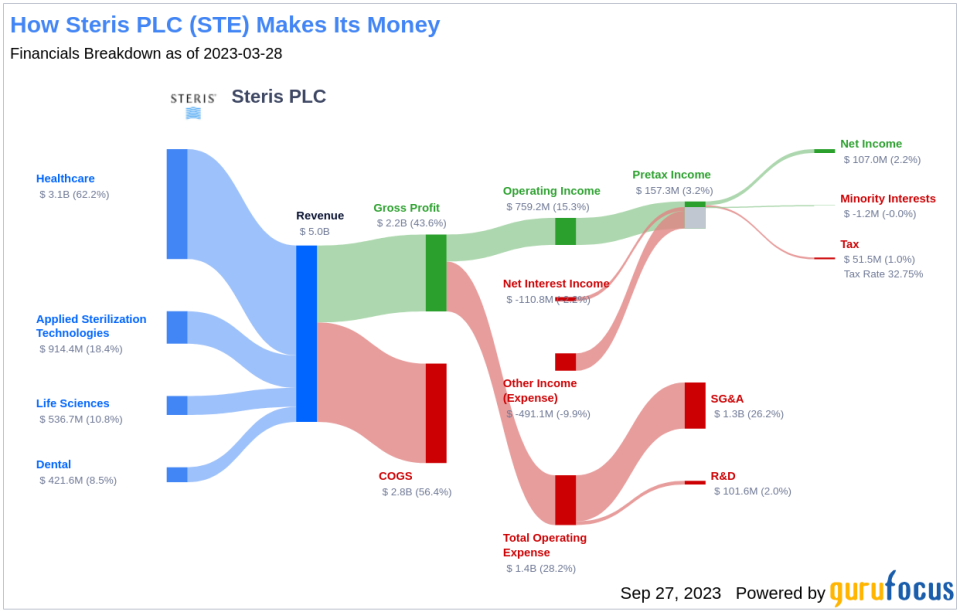

Steris PLC is an Ireland-domiciled medical device company with a focus on sterilization services and infection prevention. It leads the global market in contract sterilization services, ensuring the safe delivery of single-use and implantable medical equipment to hospitals worldwide. Steris PLC also sells sterilizers, washer-disinfectors, and other decontamination equipment and supplies for use by care provider facilities and biopharma manufacturing sites.

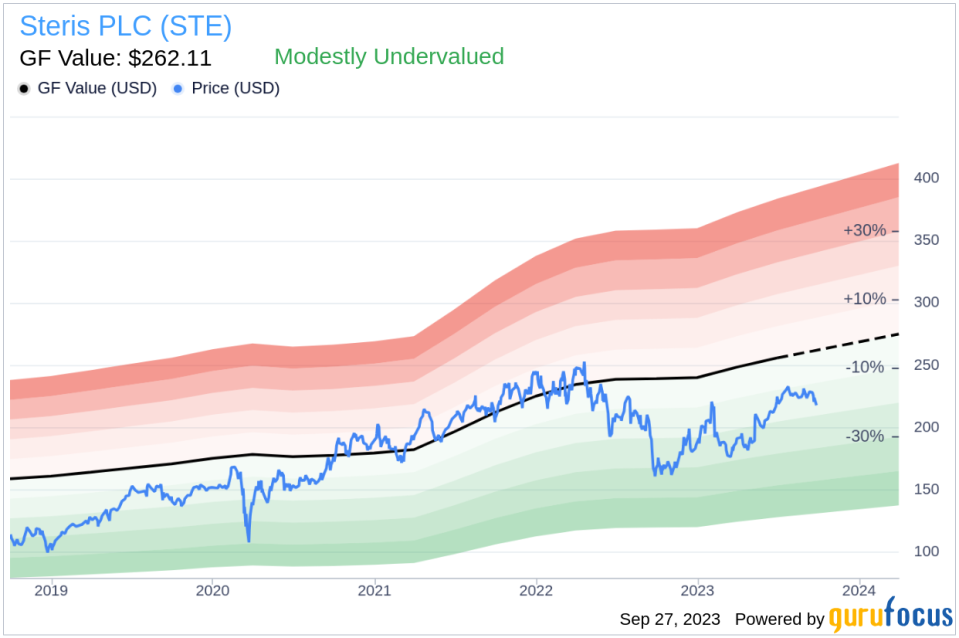

Despite its 2015 inversion to Ireland, the firm still derives approximately 70% of its revenue from its U.S. operations, 10% from the United Kingdom, and the remaining 20% from other international regions. With a market cap of $21.50 billion and sales of $5.10 billion, Steris PLC's stock price stands at $217.9, while the GF Value estimates its fair value at $262.11, suggesting that the stock is modestly undervalued.

Understanding GF Value

The GF Value is a unique measure of a stock's intrinsic value, calculated based on historical multiples, a GuruFocus adjustment factor, and future business performance estimates. The GF Value Line gives an overview of the stock's ideal fair trading value.

According to the GF Value, Steris PLC's stock is estimated to be modestly undervalued. This estimation is based on historical multiples, an internal adjustment based on the company's past business growth, and analyst estimates of future business performance. If the share price is significantly above the GF Value Line, the stock may be overvalued and have poor future returns. Conversely, if the share price is significantly below the GF Value Line, the stock may be undervalued and have higher future returns.

Because Steris PLC is relatively undervalued, the long-term return of its stock is likely to be higher than its business growth.

Link: These companies may deliever higher future returns at reduced risk.

Financial Strength

Investing in companies with low financial strength could result in permanent capital loss. Therefore, it's crucial to review a company's financial strength before deciding to buy shares. Steris PLC has a cash-to-debt ratio of 0.07, ranking worse than 94.52% of 840 companies in the Medical Devices & Instruments industry. Based on this, GuruFocus ranks Steris PLC's financial strength as 6 out of 10, suggesting a fair balance sheet.

Profitability and Growth

Investing in profitable companies, especially those with consistent profitability over the long term, is less risky. Steris PLC has been profitable 10 over the past 10 years. Over the past twelve months, the company had revenue of $5.10 billion and Earnings Per Share (EPS) of $1.22. Its operating margin is 15.53%, ranking better than 76.29% of 835 companies in the Medical Devices & Instruments industry. Overall, the profitability of Steris PLC is ranked 9 out of 10, indicating strong profitability.

Growth is a significant factor in the valuation of a company. The faster a company is growing, the more likely it is to be creating value for shareholders, especially if the growth is profitable. The 3-year average annual revenue growth rate of Steris PLC is11.8%, ranking better than 62.52% of 731 companies in the Medical Devices & Instruments industry. However, the 3-year average EBITDA growth rate is -1.6%, ranking worse than 64.45% of 737 companies in the same industry.

ROIC vs WACC

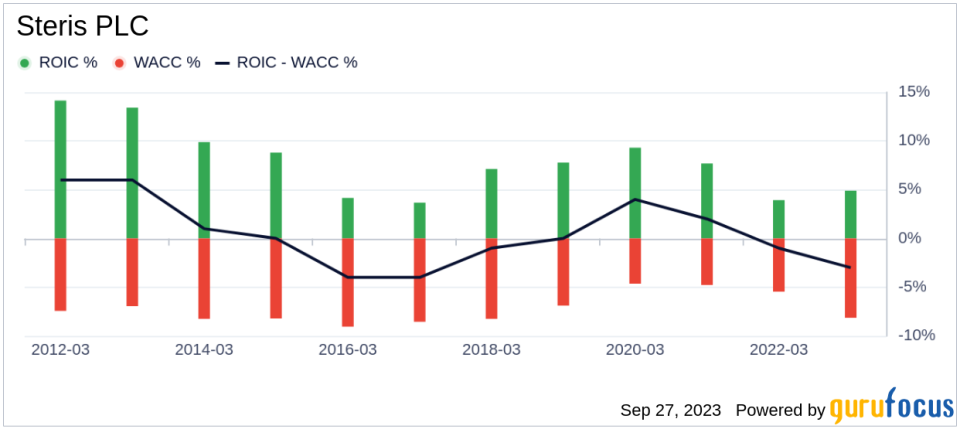

Comparing the return on invested capital to the weighted average cost of capital is another method of determining a company's profitability. Return on invested capital (ROIC) measures how well a company generates cash flow relative to the capital it has invested in its business. The weighted average cost of capital (WACC) is the rate that a company is expected to pay on average to all its security holders to finance its assets. When the ROIC is higher than the WACC, it implies the company is creating value for shareholders. For the past 12 months, Steris PLC's ROIC is 5.12, and its WACC is 9.99.

Conclusion

In conclusion, Steris PLC (NYSE:STE) stock appears to be modestly undervalued. The company's financial condition is fair, and its profitability is strong. However, its growth ranks worse than 64.45% of 737 companies in the Medical Devices & Instruments industry. To learn more about Steris PLC stock, you can check out its 30-Year Financials here.

To find out the high-quality companies that may deliver above-average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.