Steven Madden (SHOO) Q2 Earnings Miss, Revenues Down Y/Y

Steven Madden, Ltd. SHOO reported lower-than-expected results in second-quarter 2023, wherein the top and bottom lines missed the Zacks Consensus Estimate. Revenues and earnings also declined year over year.

In the reported quarter, the company witnessed a tough operating environment, conservative order patterns from wholesale customers and tough year-over-year comparisons. However, Steven Madden has reduced its inventory levels and saw a strong gross margin performance in spite of the promotional retail backdrop. Also, it has been managing expenses.

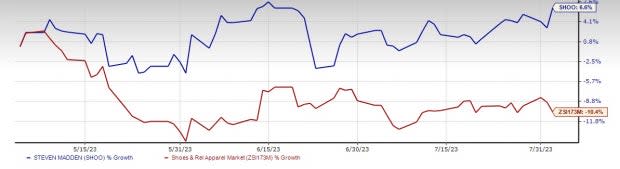

Over the past three months, shares of this presently Zacks Rank #3 (Hold) player have increased 6.6% against the industry’s 10.4% drop.

Image Source: Zacks Investment Research

Q2 Highlights

Steven Madden posted adjusted quarterly earnings of 47 cents a share, which missed the Zacks Consensus Estimate by a penny. The same decreased 25.4% from earnings of 63 cents per share reported in the prior-year period.

Total revenues fell 16.8% year over year to $445.3 million. While net sales of $442.8 million decreased 16.9%, commission and licensing fee income of $2.5 million increased 8.7% from the year-ago period’s level. The top line came below the consensus estimate of $454 million.

Gross profit tumbled 12.8% year over year to $189.9 million. Nonetheless, the gross margin expanded 190 basis points (bps) to 42.6%. Gross profit, as a percentage of wholesale revenues, increased 200 bps to 33.6%, driven by higher margin in the Wholesale accessories/apparel business. However, gross profit, as a percentage of direct-to-consumer revenues, decreased 270 bps to 63.7% owing to higher promotional activity.

Adjusted operating expenses dipped 4.4% year over year to $145.8 million. However, as a percentage of revenues, adjusted operating expenses expanded 440 bps to 32.6%.

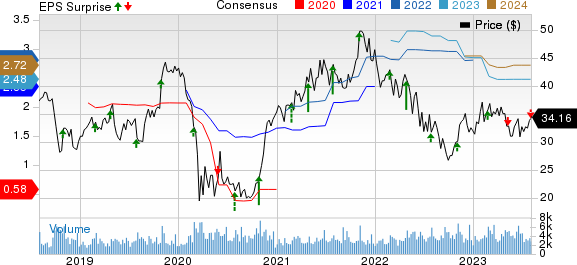

Steven Madden, Ltd. Price, Consensus and EPS Surprise

Steven Madden, Ltd. price-consensus-eps-surprise-chart | Steven Madden, Ltd. Quote

Steven Madden reported an adjusted operating income of $44.5 million, down from $67 million registered in the same quarter a year ago. The adjusted operating margin contracted 250 bps to 10%.

Segmental Performance

Revenues for the Wholesale business decreased 20.8% year over year to $314.6 million. We note that Wholesale footwear revenues fell 19.4% year over year, while Wholesale accessories/apparel revenues were down 24.6%.

Direct-to-consumer revenues dipped 5.4% to $128.2 million, driven by a decrease in the brick-and-mortar business and e-commerce unit.

Steven Madden ended the second quarter with 242 brick-and-mortar retail outlets, five e-commerce websites and 22 company-operated concessions across international markets.

Other Financial Aspects

Steven Madden ended the reported quarter with cash and cash equivalents of $258.1 million, short-term investments of $16.4 million and stockholders’ equity of $824.5 million, excluding non-controlling interest of $17.2 million. Management incurred capital expenditures of $7.8 million in the first half of 2023.

In the reported quarter, SHOO repurchased $25.8 million of its common stock, including shares acquired via the net settlement of employees’ stock awards. Moreover, the company’s board has approved a quarterly cash dividend of 21 cents per share, payable Sep 25, 2023, to stockholders of record as on Sep 15.

Outlook

Moving ahead, although wholesale customers remain cautious, the company expects to experience significant improvement for the rest of the year in comparison to the first half. Management anticipates returning to year-over-year growth in direct-to-consumer in the back half.

Overall, management expects the operating backdrop to be choppy in the near term. However, the company is poised to witness major improvement in its financial performance starting in the third quarter.

Steven Madden continues to project revenues to decline 6.5-8% from the last year’s level. SHOO envisions earnings per share (EPS) of $2.38-$2.48 and adjusted EPS of $2.40-$2.50 for the year. In 2022, Steven Madden reported revenues of $2.1 billion and adjusted EPS of $2.80.

Eye These Solid Picks

Some better-ranked companies are Royal Caribbean RCL, lululemon athletica LULU and Ralph Lauren RL.

Royal Caribbean sports a Zacks Rank #1 (Strong Buy), at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

RCL has a trailing four-quarter earnings surprise of 26.4%, on average. The Zacks Consensus Estimate for RCL’s 2023 sales and EPS indicates increases of 48.7% and 162.9%, respectively, from the year-ago period’s reported levels.

lululemon athletica is a yoga-inspired athletic apparel company. LULU carries a Zacks Rank #2 (Buy), at present.

The Zacks Consensus Estimate for lululemon athletica’s current financial-year sales and EPS suggests growth of 17.1% and 18.4%, respectively, from the year-ago corresponding figures. LULU has a trailing four-quarter earnings surprise of 9.9%, on average.

Ralph Lauren, a footwear and accessories dealer, has a Zacks Rank of 2 at present. RL has a trailing four-quarter earnings surprise of 17.4%, on average.

The Zacks Consensus Estimate for Ralph Lauren’s current financial-year sales and EPS suggests growth of 2.8% and 13.1%, respectively, from the year-ago corresponding figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

Ralph Lauren Corporation (RL) : Free Stock Analysis Report

lululemon athletica inc. (LULU) : Free Stock Analysis Report

Steven Madden, Ltd. (SHOO) : Free Stock Analysis Report