Steven Madden's (SHOO) Strategic Efforts Appear Encouraging

Steven Madden, Ltd. SHOO is well-poised for growth, thanks to its sturdy digital efforts and other robust strategies, including international business expansion and brand strength. Solid gains from product assortments and direct-to-consumer channels also remain tailwinds. These tailwinds, coupled with a robust business model, position the company well to cash in on the market growth opportunities and boost stakeholders’ value in the long haul.

Let’s delve deeper.

Strategies in Detail

Steven Madden is focused on creating trend-right merchandise assortment, deepening relations with customers via marketing, enhancing the digital commerce agenda, expanding international markets and efficiently controlling expenses. We note that the company’s international business performed well during the first quarter of 2023. The business recorded a revenue increase of 13% in the said quarter and accounted for more than 18% of the consolidated revenues for the third straight quarter.

Regarding its strategic efforts, management has added high-level talent to the organization, ramped up digital marketing spending, improved data science capabilities, rolled out buy online, pick up in store across its entire U.S. full-price retail outlets and introduced advanced delivery and return options. Steven Madden is focused on driving growth across the direct-to-consumer business, led by digital capabilities; expanding categories apart from footwear, such as handbags and apparel; and reinforcing its core U.S. wholesale footwear business.

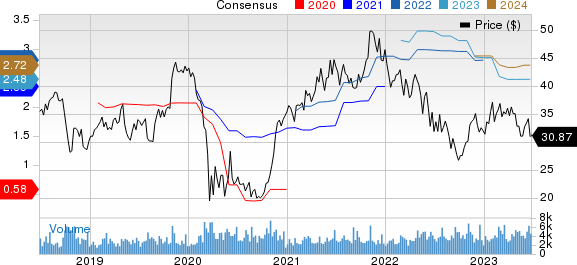

Steven Madden, Ltd. Price and Consensus

Steven Madden, Ltd. price-consensus-chart | Steven Madden, Ltd. Quote

In addition, the company is committed to boosting its e-commerce wing via prudent investments in digital marketing and efforts to optimize its website’s features and functionality. Gains from increased investment in digital marketing and robust consumer reception capabilities such as the try before you buy option have been strengths. The company has also been significantly accelerating its digital commerce initiatives with respect to distribution.

Prudent acquisitions have been aiding Steven Madden’s performance as well. Its BB Dakota buyout, which is a California-based women's apparel company, appears encouraging. With this acquisition, the company is able to expand its apparel category. Additionally, management had concluded the acquisition of the remaining 49.9% share of its European joint venture. This transaction distributes the company’s branded footwear and accessories across the majority of countries in Europe.

What’s More?

Analysts seem quite optimistic about the company. The Zacks Consensus Estimate for 2024 sales and earnings per share (EPS) is currently pegged at $2.1 billion and $2.72, respectively. These estimates show corresponding growth of 5.2% and 9.8% year over year.

The aforesaid strengths have resulted in Steven Madden’s shares increasing 3.4% in the year-to-date span, comfortably outpacing the industry’s 7.5% drop. This Zacks Rank #3 (Hold) company is further backed by a VGM Score of B.

To wrap up, Steven Madden seems to be a decent investment bet now given all the aforementioned positives.

Eye These Solid Picks

Some better-ranked companies are Royal Caribbean RCL, Crocs CROX and lululemon athletica LULU.

Royal Caribbean sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

RCL has a trailing four-quarter earnings surprise of 26.4%, on average. The Zacks Consensus Estimate for RCL’s 2023 sales and EPS indicates increases of 47.9% and 158.3%, respectively, from the year-ago period’s reported levels.

Crocs, which offers casual lifestyle footwear and accessories, presently carries a Zacks Rank #2 (Buy). The expected EPS growth rate for three to five years is 15%.

The Zacks Consensus Estimate for Crocs’ current financial-year sales and EPS suggests growth of 13.1% and 2.8% from the year-ago period’s reported figure. CROX has a trailing four-quarter earnings surprise of 21.8%, on average.

lululemon athletica is a yoga-inspired athletic apparel company. LULU carries a Zacks Rank of 2 at present.

The Zacks Consensus Estimate for lululemon athletica’s current financial-year sales and EPS suggests growth of 16.7% and 18%, respectively, from the year-ago corresponding figures. LULU has a trailing four-quarter earnings surprise of 9.9%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

lululemon athletica inc. (LULU) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

Steven Madden, Ltd. (SHOO) : Free Stock Analysis Report