Stitch Fix (NASDAQ:SFIX) Misses Q2 Revenue Estimates, Stock Drops

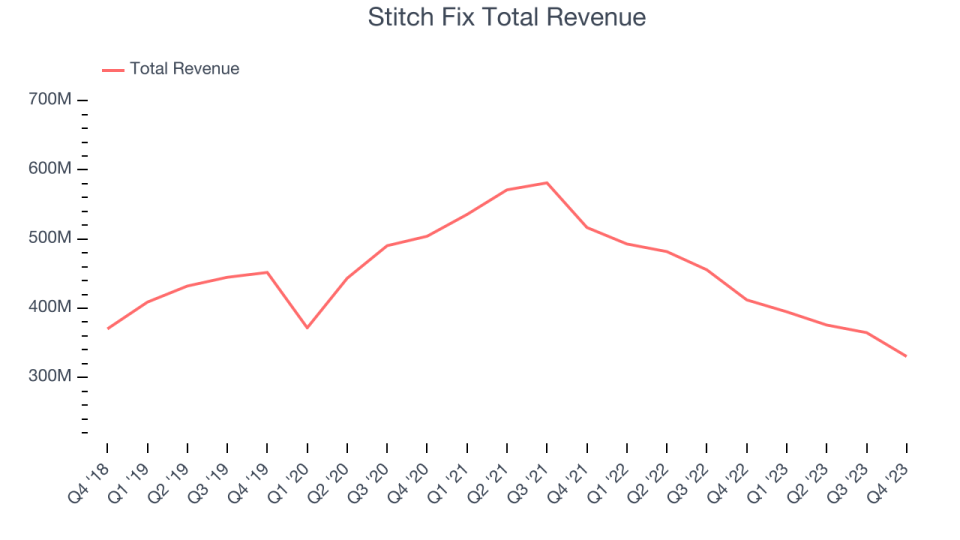

Personalized clothing company Stitch Fix (NASDAQ:SFIX) fell short of analysts' expectations in Q2 FY2024, with revenue down 19.8% year on year to $330.4 million. Next quarter's revenue guidance of $305 million also underwhelmed, coming in 5.7% below analysts' estimates. It made a GAAP loss of $0.29 per share, improving from its loss of $0.58 per share in the same quarter last year.

Is now the time to buy Stitch Fix? Find out by accessing our full research report, it's free.

Stitch Fix (SFIX) Q2 FY2024 Highlights:

Revenue: $330.4 million vs analyst estimates of $332.3 million (0.6% miss)

EPS: -$0.29 vs analyst expectations of -$0.22 (32.6% miss)

Revenue Guidance for Q3 2024 is $305 million at the midpoint, below analyst estimates of $323.3 million

The company dropped its revenue guidance for the full year from $1.34 billion to $1.31 billion at the midpoint, a 2.2% decrease

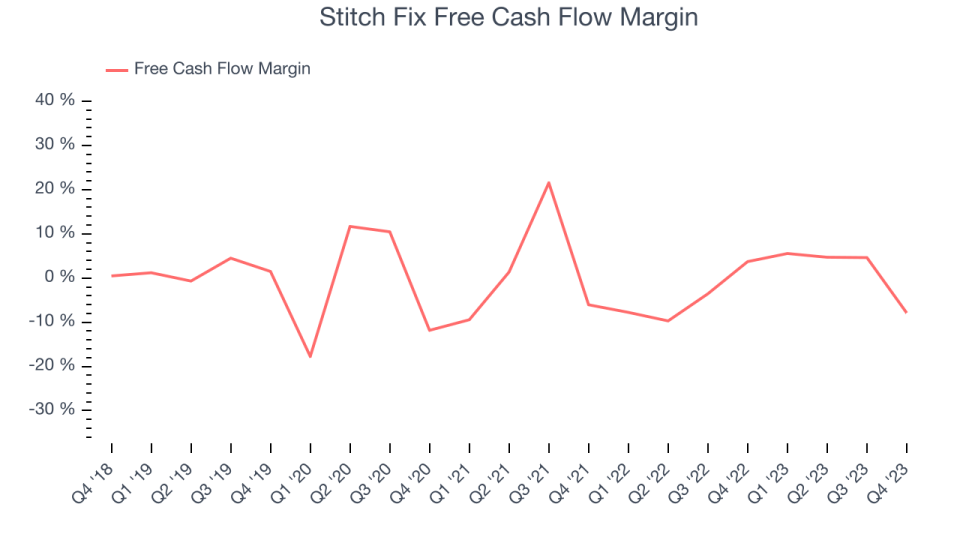

Free Cash Flow was -$26.07 million, down from $16.91 million in the previous quarter

Gross Margin (GAAP): 43.4%, up from 41% in the same quarter last year

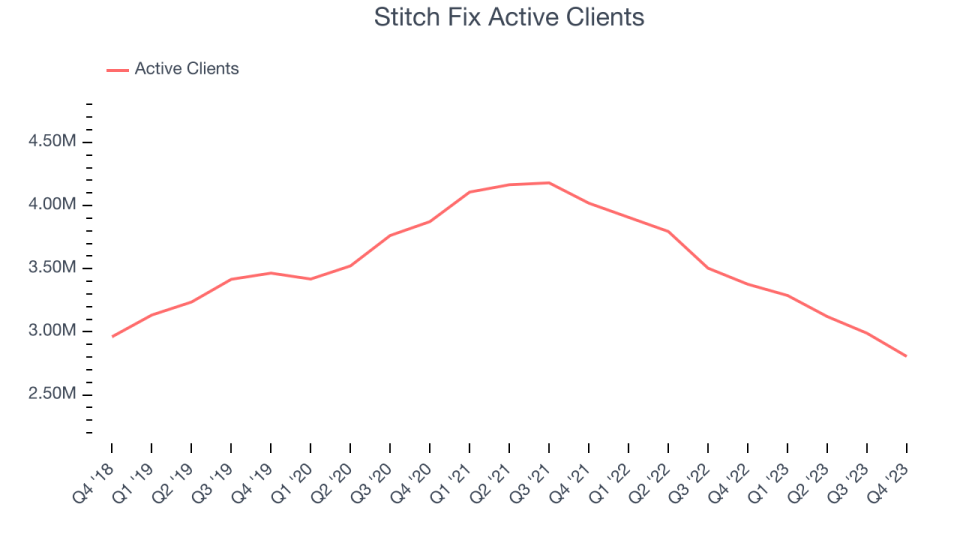

Active Clients: 2.81 million

Market Capitalization: $378.4 million

“The original Stitch Fix vision, to create an easier and more enjoyable way for people to shop for clothing and accessories, remains both relevant and compelling,” said Matt Baer, Chief Executive Officer.

One of the original subscription box companies, Stitch Fix (NASDAQ:SFIX) is an online personal styling and fashion service that curates personalized clothing selections for customers.

Apparel, Accessories and Luxury Goods

Within apparel and accessories, not only do styles change more frequently today than decades past as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel, accessories, and luxury goods companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

A company’s long-term performance can give signals about its business quality. Any business can put up a good quarter or two, but many enduring ones muster years of growth. Stitch Fix's annualized revenue growth rate of 1.3% over the last five years was weak for a consumer discretionary business.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Stitch Fix's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 18.5% over the last two years.

We can better understand the company's revenue dynamics by analyzing its number of active clients, which reached 2.81 million in the latest quarter. Over the last two years, Stitch Fix's active clients averaged 13.9% year-on-year declines. Because this number is higher than its revenue growth during the same period, we can see the company's monetization has fallen.

This quarter, Stitch Fix missed Wall Street's estimates and reported a rather uninspiring 19.8% year-on-year revenue decline, generating $330.4 million of revenue. The company is guiding for a 22.8% year-on-year revenue decline next quarter to $305 million, a deceleration from the 19.9% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects revenue to decline 5.9% over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, Stitch Fix's demanding reinvestments to stay relevant with consumers have drained company resources. Its free cash flow margin has been among the worst in the consumer discretionary sector, averaging negative 1.7%.

Stitch Fix burned through $26.07 million of cash in Q2, equivalent to a negative 7.9% margin. This caught our eye as the company shifted from cash flow positive in the same quarter last year to cash flow negative this quarter.

Key Takeaways from Stitch Fix's Q2 Results

We struggled to find many strong positives in these results. Its full-year revenue guidance missed and its declining active clients fell short of Wall Street's estimates. Furthermore, its cash burn and EPS loss were much worse than expected. Overall, the results could have been better. The company is down 9.8% on the results and currently trades at $2.96 per share.

Stitch Fix may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.