Strategic Value Investing: Replacement Value

Wouldn't it be nice to simply tally up a firm's assets, estimate the replacement cost of each of them and arrive at a purchase price, whether for the whole company or per share?

Yes, but once again reality intrudes. "This idea is straightforward in concept, but, unfortunately, in practice, it is much more difficult for the investor to estimate this seemingly straightforward metric," wrote the authors of "Strategic Value Investing: Practical Techniques of Leading Value Investors."

With that, Stephen Horan, Robert R. Johnson and Thomas Robinson introduced a measure called "Tobin's q." Yale economist and Nobel Laureate James Tobin hypothesized that the total value of companies in the market should be about the same as their replacement costs. They added, "Specifically, Tobin's q is the ratio of the market value of debt and equity to the replacement cost of total assets:"

The formula resembles that of MV/BV (market value divided by book value), as discussed in the previous section. But there are a couple of differences:

The numerator (the top number) includes the market value of both debt and equity (or the total capital).

The denominator (the lower number) refers to total assets rather than equity. Note that assets are valued by their replacement cost, rather than their historical accounting cost (i.e., book value). This allows analysts to factor in such effects as inflation.

What does it all mean? Tobin's q is a tool for estimating the valuation of the whole market; when it is high, the market is likely overvalued and carries significant risk. When it is low, value investors will take it as a sign that the market is potentially undervalued and poses less risk.

Some analysts do use Tobin's q for individual stocks, but it is considered more useful for the market as a whole. From an individual company perspective, it is difficult to estimate replacement costs. As the authors noted, rational investors likely would not agree on the replacement value of Microsoft (NASDAQ:MSFT)'s assets. This is not an issue for estimating the value of the market, in part because the Federal Reserve provides data for the variables in its "Flow of Funds" report.

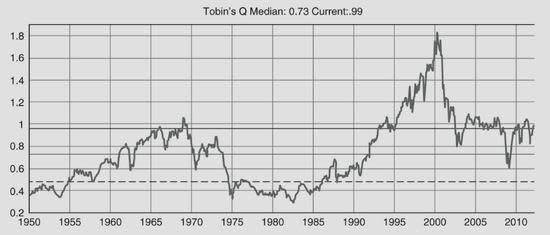

Between 1950 and 2010, Tobin's q varied between 0.3 and 1.8. It was at its lowest during the recession and high-interest period of the early 1980s. The highest reading came in early 2000, as the dot-com bubble was reaching its zenith:

The authors added, "The takeaway for the strategic value investor on the discussion on replacement value in general and Tobin's q specifically, is that it gives you an idea of the general valuation level of the market."

Sum-of-the-parts valuation

Another asset-based model is the sum-of-the-parts valuation model, or as it's sometimes called, the "breakup" value.

It may come into play when analysts are valuing a highly complex firm; by valuing each of the parts of such companies individually, they believe they can reach a more accurate valuation.

An example occurred in 1999 when Creative Computers decided to sell a 20% stake in its subsidiary, uBid (UBID). Based on uBid's share price, Creative's stake in it was worth $350 million. However, Creative's total market equity was worth only $275 million. That implied the rest of Creative was worth a negative $75 million. The authors pointed out this meant Creative was undervalued, uBid was overvalued, or there was some combination of the two.

In another example, hedge fund manager John Paulson (Trades, Portfolio) bought some 8.4% of the stock of Hartford Financial Services Group (NYSE:HIG). His research told him that if Hartford's life insurance and property-and-casualty insurance services were split up, the company would be valued at $32 per share, 50% more than the $21 it was trading at when Paulson brought forward his proposal. Many conglomerates with unrelated product lines are valued this way.

Spin-offs and carve-outs

If activist investors see that management is not making the most of one of its business lines, they may press for spin-offs or carve-outs. A "spin-off" means a business line is spun out of the parent company by making it an independent company, owned and operated on its own. A "carve-out" occurs when a company sells a minority stake in a subsidiary through an initial public offering or rights offering; it is thus considered a partial spin-off. When Creative Computers sold a minority interest in uBid, for example, it was a carve-out.

The authors observed:

"The performance of spin-offs and carve outs over time has been quite remarkable. The mere announcement of a spin-off or carve out is generally positively received by the market ... as the market anticipates improved operating performance by the parent company. These studies find a mean abnormal (that is, above the market and adjusted for risk) spin-off announcement return of approximately 3 percent."

The spin-off or carve-out effect may last up to several years, as these companies outperform the market by a significant margin. At the same time, the companies that did the spinning off or carving out also benefited: "These results certainly provide an economic rationale for firms to consider spin-offs and provides evidence that strategic value investors should consider spin-offs (and their parents) as potential investments."

In another example, the authors reported on a valuation of Berkshire Hathaway (NYSE:BRK.A)(NYSE:BRK.B) by Tom Gayner (Trades, Portfolio) and Greg Speicher. They broke Berkshire into three parts: the investment portfolio, insurance operations and non-insurance operations. Their calculations led to an average value of the A- and B-shares of $191,336 and $128. Both were higher than the market prices at the time: $175,825 and $117.17. If such a difference were great enough, at any other company than Berkshire Hathaway, activists would no doubt be taking a close look.

One other aspect of using this model: It opens the door to sensitivity analysis.

Conclusion

In this section of chapter nine of "Strategic Value Investing: Practical Techniques of Leading Value Investors," authors Stephen Horan, Robert R. Johnson and Thomas Robinson have provided more models for valuing the market and individual stocks.

Tobin's q is the market-pricing tool, allowing investors to quantify the idea that "the market is up" or "the market is down." Its application as a tool for valuing individual companies is generally limited.

For valuing companies, the book has added three new tools under the banner of replacement value: sum of the parts, spin-offs and carve-outs. Each has a niche place in the toolbox of value investors.

Disclosure: I do not own shares in any company listed, and do not expect to buy any in the next 72 hours.

Read more here:

Strategic Value Investing: Book Value

Strategic Value Investing: Free Cash Flow to Equity Model

Strategic Value Investing: Free Cash Flow to the Firm Model

Not a Premium Member of GuruFocus? Sign up for a free 7-day trial here.

This article first appeared on GuruFocus.