Supermarkets Likely to Gain in 2023 Despite Growing Challenges

Supermarkets had a great run during and right after the pandemic, as people were staying home more often, which meant that they were cooking at home. The hybrid working style that was adopted thereafter was also conducive to growth, and for the same reasons.

Inflation has been positive for the industry in the sense that it allowed companies to raise prices and thereby record higher sales even when volumes didn’t keep up. The negative side of the story is that it increased overall costs of operation, including on freight and transportation, as well as labor charges. It also led to the loss of customers on the low end who went elsewhere for better bargains.

Those bargains are coming from no-frills online-only warehouse-type outlets that deliver orders quickly and cheaply. These dark stores, or micro fulfillment centers, are growing popular because of cost, speed and convenience.

Another group taking away business are stores like Costco, Dollar General, Target and Walmart that sell general merchandise in addition to groceries. Since they have a broader spread, they attract more foot traffic. And since they usually offer huge deals on groceries with lost profits being made good on other items, many shoppers get diverted to them. Whatever these stores gain, the supermarkets lose out on.

Competition is also coming from the traditional eateries, i.e. restaurants. Eating out had become taboo during the pandemic, and although rising prices are a deterrent, many are going back to old habits. This is expected to be a growing trend over the next few years despite the fact that people are cooking at home more than they had previously.

But there is hope for grocers yet. While they can’t fight the eating out trend, the deli section is likely to do well, as it offers quick and healthy options for consumers not wanting to eat out, especially those that can’t afford it. So even if they don’t want to spend what it takes to have a healthy meal at restaurants, they still have options. Focusing on improving and stocking this section is one way for supermarkets to make the best of the situation.

Health itself is a focus for many consumers, as well as sustainability. An increasing number of consumers are willing to pay more for healthy options that have been sourced responsibly. Therefore, this segment offers scope for growth.

The other big area that companies are focusing on is convenience. In fact, it is the main reason for the growth in online grocery shopping. Therefore, in order to balance the growth in online shopping (which is not going anywhere), supermarkets need to upgrade the technology they are using to improve the experience for the patrons.

Improved technology can do wonders in the store, for example scanning products while in the isle, smart baskets that record your sales while you shop, no-touch payments, seamless payments for which you don’t need to wait in line, etc. All of this attracts customers, especially the younger ones. When you add omnichannel services to this, it gets all the more convenient for consumers.

Given this backdrop and the fact that grocery sales are expected to increase 5.6% in 2023, this could be a good time to stock up on some shares:

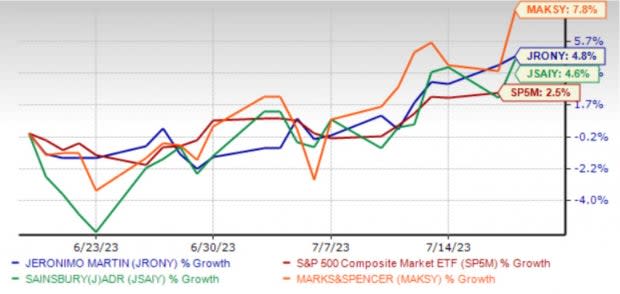

Jeronimo Martins SGPS JRONY for example carries a Zacks Rank #1 (Strong Buy). The Zacks Style Score system indicates that Jeronimo is attractive for both Value and Growth investors. Its revenue and profit are expected to grow a respective 25.4% and 36.9% this year and another 6.1% and 10.7%. respectively in the next. The 2023 estimate is up 12.0% and the 2024 estimate up 11.5% in the last 60 days.

Similarly, #2 (Buy) ranked Marks and Spencer Group MAKSY is attractive for both Value and Growth investors. The company’s revenues are expected to grow 5.1% in the year ending March 2024. They following year they’re expected to grow 3.3%. The company’s earnings are expected to grow -4.8% and 21.3%, respectively in the two years. The 2024 estimate has gone from 36 cents to 40 cents while the 2025 estimate has gone from 42 cents to 48 cents in the last 60 days.

#2 ranked J. Sainsbury JSAIY is also attractive for both Value and Growth investors. While revenue and earnings are expected to decline around 2% this year, 2025 (ending March) is expected to bring a respective 1.6% and 4.3% growth. Estimates for the two years are up 5 cents and 4 cents, respectively in the last 60 days.

Walmart’s stock is also worth considering. With a B for Growth and Value, the shares are clearly appealing for most investors. Walmart’s revenue is currently expected to grow 4.2% this year even as its earnings decline 1.3%. Next year, its revenue and earnings are expected to grow a respective 3.5% and 10.5%. Estimates for 2024 (ending January) and 2025 are up 5 cents and 4 cents, respectively in the last 60 days.

One-Month Price Performance

Image Source: Zacks Investment Research

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Marks and Spencer Group PLC (MAKSY) : Free Stock Analysis Report

Jeronimo Martins SGPS SA (JRONY) : Free Stock Analysis Report

J. Sainsbury PLC (JSAIY) : Free Stock Analysis Report