Sweetgreen (NYSE:SG) Posts Q4 Sales In Line With Estimates, Stock Soars

Casual salad chain Sweetgreen (NYSE:SG) reported results in line with analysts' expectations in Q4 FY2023, with revenue up 29.1% year on year to $153 million. The company expects next quarter's revenue to be around $152 million, coming in 2.8% above analysts' estimates. It made a GAAP loss of $0.24 per share, improving from its loss of $0.49 per share in the same quarter last year.

Is now the time to buy Sweetgreen? Find out by accessing our full research report, it's free.

Sweetgreen (SG) Q4 FY2023 Highlights:

Revenue: $153 million vs analyst estimates of $152 million (small beat)

EPS: -$0.24 vs analyst estimates of -$0.27 (10.9% beat)

Revenue Guidance for Q1 2024 is $152 million at the midpoint, above analyst estimates of $147.8 million (adjusted EBITDA guided ahead for that period as well)

Management's revenue guidance for the upcoming financial year 2024 is $662.5 million at the midpoint, in line with analyst expectations and implying 13.4% growth (vs 24.2% in FY2023) (adjusted EBITDA guided ahead for that period as well)

Gross Margin (GAAP): 16.2%, up from 13.3% in the same quarter last year

Same-Store Sales were up 6% year on year

Market Capitalization: $1.39 billion

“2023 was a strong year for Sweetgreen - we continued to demonstrate high growth, substantial operating leverage and executed on significant innovation across the business. In the fourth quarter, we expanded restaurant-level profit margins by 500 basis points in 2023 compared to 2022, and our guidance calls for Adjusted EBITDA profitability in 2024(2),” said Jonathan Neman, CEO and Co-Founder.

Founded in 2007 by three Georgetown University alum, Sweetgreen (NYSE:SG) is a casual quick service chain known for its healthy salads and bowls.

Modern Fast Food

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

Sales Growth

Sweetgreen is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefitting from better brand awareness and economies of scale. On the other hand, one advantage is that its growth rates can be higher because it's growing off a small base.

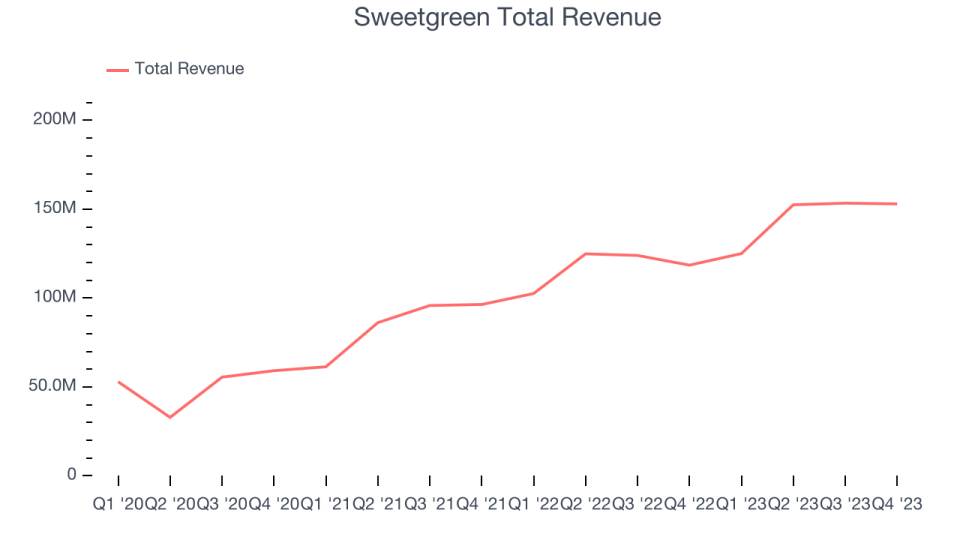

As you can see below, the company's annualized revenue growth rate of 20.8% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was exceptional as it added more dining locations and increased sales at existing, established restaurants.

This quarter, Sweetgreen's year-on-year revenue growth of 29.1% was excellent, and its $153 million in revenue was in line with Wall Street's estimates. The company is guiding for revenue to rise 21.5% year on year to $152 million next quarter, in line with the 21.9% year-on-year increase it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 13.5% over the next 12 months, a deceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Same-Store Sales

Same-store sales growth is an important metric that tracks organic growth and demand for a restaurant's established locations.

Sweetgreen's demand has outpaced the broader restaurant sector over the last eight quarters. On average, the company has grown its same-store sales by a robust 9.9% year on year. With positive same-store sales growth amid an increasing number of restaurants, Sweetgreen is reaching more diners and growing sales.

In the latest quarter, Sweetgreen's same-store sales rose 6% year on year. This growth was an acceleration from the 4% year-on-year increase it posted 12 months ago, which is always an encouraging sign.

Key Takeaways from Sweetgreen's Q4 Results

Revenue beat by a small amount and EPS beat by a more convincing amount. We were also glad that next quarter's revenue and adjusted EBITDA guidance came in higher than Wall Street's estimates. Finally, while full year revenue guidance was in line, adjusted EBITDA was better than Wall Street estimates. Overall, we think this was a really good quarter that should please shareholders. The stock is up 11.2% after reporting and currently trades at $14.19 per share.

Sweetgreen may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.