Is Targa Resources Corp (TRGP) Modestly Overvalued?

With a daily gain of 3.61% and an Earnings Per Share (EPS) of $3.86, Targa Resources Corp (NYSE:TRGP) has attracted attention from value investors. But is the stock modestly overvalued? This analysis will delve into the company's valuation, financial strength, and future prospects to provide an informed perspective.

A Snapshot of Targa Resources Corp (NYSE:TRGP)

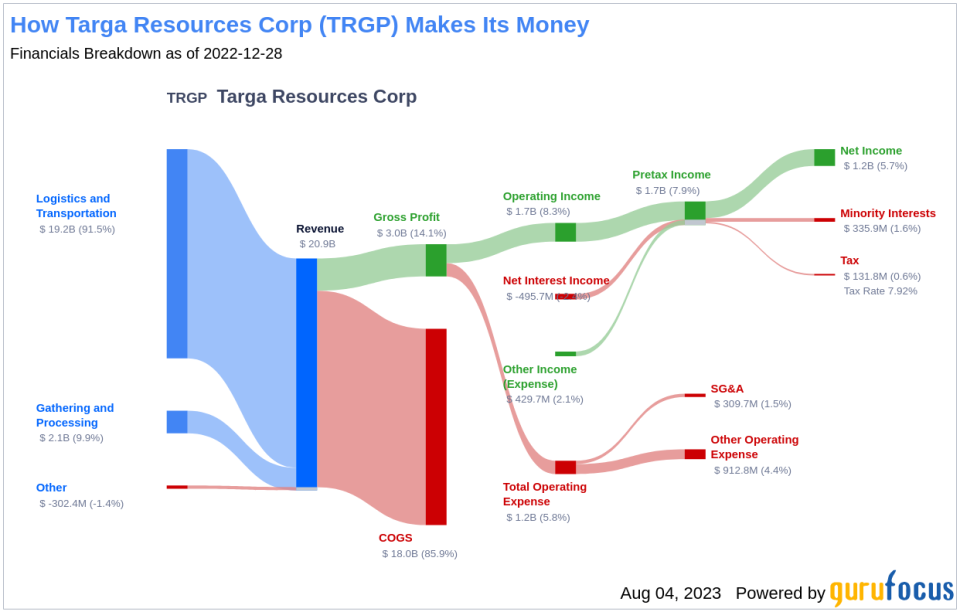

Targa Resources Corp is a midstream firm with significant operations in the Permian, Stack, Scoop, and Bakken plays. It boasts 843,000 barrels a day of gross fractionation capacity at Mont Belvieu and operates a liquefied petroleum gas export terminal. The Grand Prix natural gas liquids pipeline is one of its major assets currently in full service.

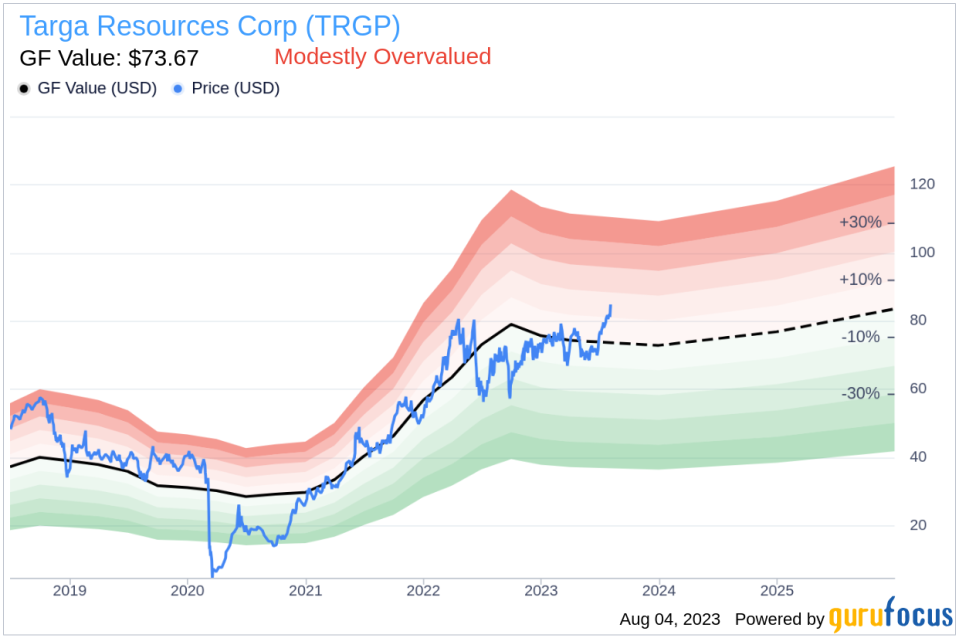

Despite an impressive daily gain, the question of its valuation persists. The company's stock price stands at $84.76, while the GF Value, an intrinsic value estimate, is at $73.67. This discrepancy suggests that the stock may be modestly overvalued.

Understanding the GF Value of Targa Resources (NYSE:TRGP)

The GF Value is a proprietary measure that reflects the intrinsic value of a stock. It takes into account historical trading multiples, a GuruFocus adjustment factor based on past performance and growth, and future business performance estimates. If the stock price significantly surpasses the GF Value Line, it implies an overvaluation and potentially poor future returns. Conversely, if it falls below the GF Value Line, the stock could be undervalued and offer higher future returns.

With a current market cap of $19.2 billion and a price of $84.76 per share, Targa Resources appears to be modestly overvalued according to the GF Value. This suggests that the long-term return of its stock is likely to be lower than its business growth.

Link: These companies may deliver higher future returns at reduced risk.

Assessing the Financial Strength of Targa Resources

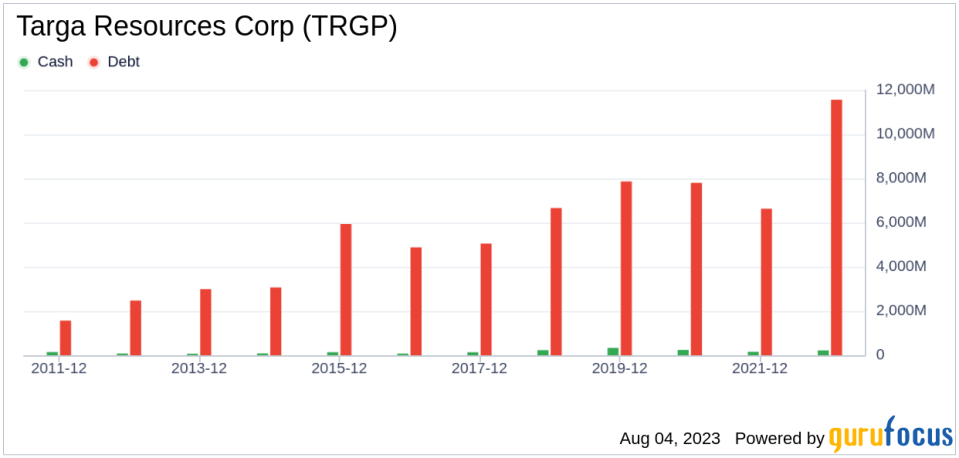

Investing in companies with robust financial strength mitigates the risk of permanent loss. Key indicators such as the cash-to-debt ratio and interest coverage offer insights into a company's financial health. Targa Resources' cash-to-debt ratio of 0.02 is inferior to 92.87% of companies in the Oil & Gas industry, indicating poor financial strength.

Evaluating the Profitability and Growth of Targa Resources

Investing in profitable companies, especially those demonstrating consistent profitability over the long term, is generally less risky. Targa Resources has been profitable for 7 out of the past 10 years. With a revenue of $20.5 billion and an Earnings Per Share (EPS) of $3.86 in the past twelve months, its operating margin of 11.08% ranks better than 54.55% of companies in the Oil & Gas industry. This indicates strong profitability.

Growth is closely correlated with the long-term performance of a company's stock. Targa Resources' 3-year average annual revenue growth rate is 34.4%, ranking better than 86.62% of companies in the Oil & Gas industry. Its 3-year average EBITDA growth rate is 36.7%, outperforming 74.97% of industry peers. This suggests strong growth.

ROIC vs WACC: A Measure of Profitability

Comparing a company's Return on Invested Capital (ROIC) to its Weighted Average Cost of Capital (WACC) offers another perspective on its profitability. Targa Resources' ROIC of 12.29 surpasses its WACC of 8.87, indicating value creation for shareholders.

Conclusion

In conclusion, Targa Resources Corp (NYSE:TRGP) appears to be modestly overvalued. Despite poor financial strength, the company exhibits strong profitability and outperforms 74.97% of companies in the Oil & Gas industry in terms of growth. For more insights into Targa Resources stock, you can check out its 30-Year Financials here.

For high-quality companies that may deliver above-average returns, consider the GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.