Should You Be Tempted To Sell Dominion Energy, Inc. (NYSE:D) Because Of Its P/E Ratio?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

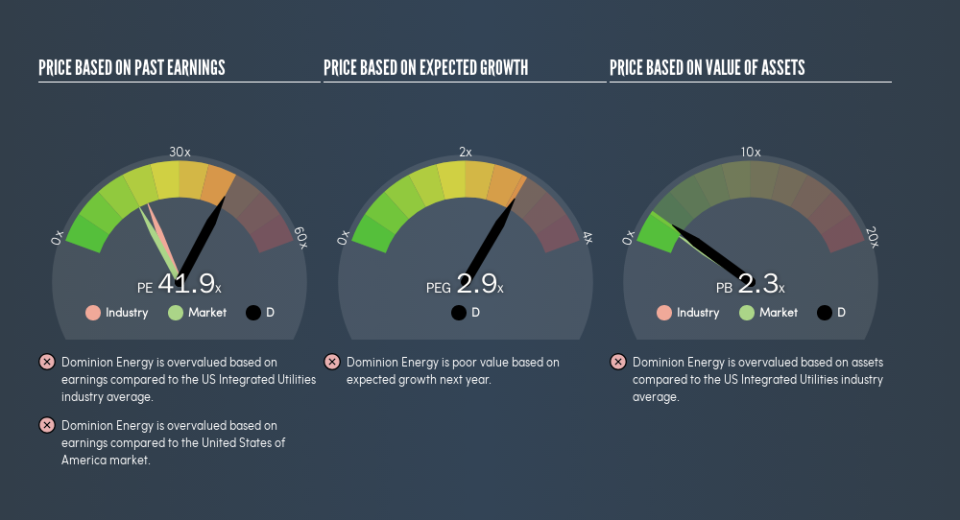

Today, we'll introduce the concept of the P/E ratio for those who are learning about investing. We'll show how you can use Dominion Energy, Inc.'s (NYSE:D) P/E ratio to inform your assessment of the investment opportunity. Dominion Energy has a P/E ratio of 41.94, based on the last twelve months. That means that at current prices, buyers pay $41.94 for every $1 in trailing yearly profits.

View our latest analysis for Dominion Energy

How Do I Calculate Dominion Energy's Price To Earnings Ratio?

The formula for P/E is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Dominion Energy:

P/E of 41.94 = $76.85 ÷ $1.83 (Based on the trailing twelve months to March 2019.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio implies that investors pay a higher price for the earning power of the business. That is not a good or a bad thing per se, but a high P/E does imply buyers are optimistic about the future.

Does Dominion Energy Have A Relatively High Or Low P/E For Its Industry?

One good way to get a quick read on what market participants expect of a company is to look at its P/E ratio. As you can see below, Dominion Energy has a higher P/E than the average company (20.2) in the integrated utilities industry.

That means that the market expects Dominion Energy will outperform other companies in its industry. Shareholders are clearly optimistic, but the future is always uncertain. So further research is always essential. I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

When earnings fall, the 'E' decreases, over time. That means even if the current P/E is low, it will increase over time if the share price stays flat. Then, a higher P/E might scare off shareholders, pushing the share price down.

Dominion Energy saw earnings per share decrease by 59% last year. And it has shrunk its earnings per share by 8.7% per year over the last five years. This might lead to muted expectations.

Remember: P/E Ratios Don't Consider The Balance Sheet

The 'Price' in P/E reflects the market capitalization of the company. So it won't reflect the advantage of cash, or disadvantage of debt. The exact same company would hypothetically deserve a higher P/E ratio if it had a strong balance sheet, than if it had a weak one with lots of debt, because a cashed up company can spend on growth.

While growth expenditure doesn't always pay off, the point is that it is a good option to have; but one that the P/E ratio ignores.

Dominion Energy's Balance Sheet

Dominion Energy has net debt worth 69% of its market capitalization. This is a reasonably significant level of debt -- all else being equal you'd expect a much lower P/E than if it had net cash.

The Bottom Line On Dominion Energy's P/E Ratio

Dominion Energy's P/E is 41.9 which is above average (17.9) in its market. With significant debt and no EPS growth last year, shareholders are betting on an improvement in earnings from the company.

When the market is wrong about a stock, it gives savvy investors an opportunity. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine.' So this free report on the analyst consensus forecasts could help you make a master move on this stock.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.