We Think Enerplus Corporation's (TSE:ERF) CEO Compensation Looks Fair

Key Insights

Enerplus' Annual General Meeting to take place on 4th of May

Salary of US$504.5k is part of CEO Ian Dundas's total remuneration

The overall pay is comparable to the industry average

Enerplus' total shareholder return over the past three years was 454% while its EPS grew by 100% over the past three years

We have been pretty impressed with the performance at Enerplus Corporation (TSE:ERF) recently and CEO Ian Dundas deserves a mention for their role in it. Coming up to the next AGM on 4th of May, shareholders would be keeping this in mind. The focus will probably be on the future company strategy as shareholders cast their votes on resolutions such as executive remuneration and other matters. In light of the great performance, we discuss the case why we think CEO compensation is not excessive.

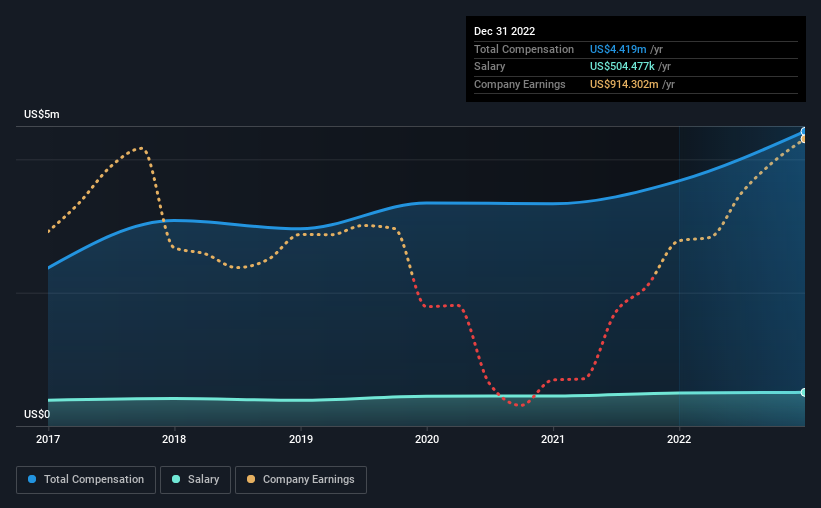

See our latest analysis for Enerplus

How Does Total Compensation For Ian Dundas Compare With Other Companies In The Industry?

According to our data, Enerplus Corporation has a market capitalization of CA$4.2b, and paid its CEO total annual compensation worth US$4.4m over the year to December 2022. Notably, that's an increase of 20% over the year before. We think total compensation is more important but our data shows that the CEO salary is lower, at US$504k.

In comparison with other companies in the Canadian Oil and Gas industry with market capitalizations ranging from CA$2.7b to CA$8.7b, the reported median CEO total compensation was US$3.5m. This suggests that Enerplus remunerates its CEO largely in line with the industry average. What's more, Ian Dundas holds CA$6.7m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

Component | 2022 | 2021 | Proportion (2022) |

Salary | US$504k | US$496k | 11% |

Other | US$3.9m | US$3.2m | 89% |

Total Compensation | US$4.4m | US$3.7m | 100% |

Speaking on an industry level, nearly 36% of total compensation represents salary, while the remainder of 64% is other remuneration. Enerplus pays a modest slice of remuneration through salary, as compared to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Enerplus Corporation's Growth

Over the past three years, Enerplus Corporation has seen its earnings per share (EPS) grow by 100% per year. It achieved revenue growth of 58% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. The combination of strong revenue growth with medium-term EPS improvement certainly points to the kind of growth we like to see. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Enerplus Corporation Been A Good Investment?

Boasting a total shareholder return of 454% over three years, Enerplus Corporation has done well by shareholders. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

The company's solid performance might have made most shareholders happy, possibly making CEO remuneration the least of the matters to be discussed in the AGM. In fact, strategic decisions that could impact the future of the business might be a far more interesting topic for investors as it would help them set their longer-term expectations.

So you may want to check if insiders are buying Enerplus shares with their own money (free access).

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here