Those who invested in W. R. Berkley (NYSE:WRB) five years ago are up 103%

Generally speaking the aim of active stock picking is to find companies that provide returns that are superior to the market average. And the truth is, you can make significant gains if you buy good quality businesses at the right price. For example, the W. R. Berkley Corporation (NYSE:WRB) share price is up 84% in the last 5 years, clearly besting the market return of around 53% (ignoring dividends). However, more recent returns haven't been as impressive as that, with the stock returning just 2.3% in the last year , including dividends .

So let's investigate and see if the longer term performance of the company has been in line with the underlying business' progress.

View our latest analysis for W. R. Berkley

While markets are a powerful pricing mechanism, share prices reflect investor sentiment, not just underlying business performance. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

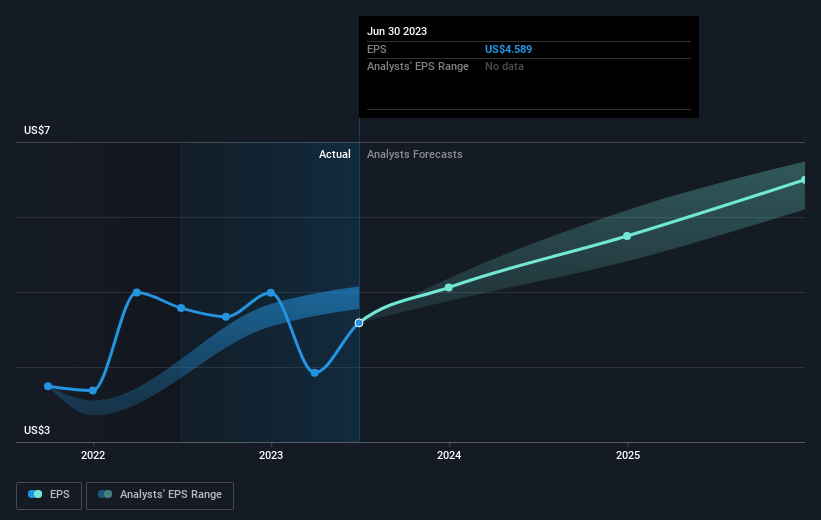

Over half a decade, W. R. Berkley managed to grow its earnings per share at 16% a year. This EPS growth is higher than the 13% average annual increase in the share price. So it seems the market isn't so enthusiastic about the stock these days.

You can see how EPS has changed over time in the image below (click on the chart to see the exact values).

We know that W. R. Berkley has improved its bottom line over the last three years, but what does the future have in store? If you are thinking of buying or selling W. R. Berkley stock, you should check out this FREE detailed report on its balance sheet.

What About Dividends?

It is important to consider the total shareholder return, as well as the share price return, for any given stock. The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. So for companies that pay a generous dividend, the TSR is often a lot higher than the share price return. In the case of W. R. Berkley, it has a TSR of 103% for the last 5 years. That exceeds its share price return that we previously mentioned. The dividends paid by the company have thusly boosted the total shareholder return.

A Different Perspective

W. R. Berkley shareholders are up 2.3% for the year (even including dividends). But that was short of the market average. On the bright side, the longer term returns (running at about 15% a year, over half a decade) look better. It may well be that this is a business worth popping on the watching, given the continuing positive reception, over time, from the market. Before forming an opinion on W. R. Berkley you might want to consider these 3 valuation metrics.

We will like W. R. Berkley better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.