Tilray, Inc. (NasdaqGS:TLRY) is Yet to Attract Institutional Investors

This article originally appeared on Simply Wall St News.

It is no secret that the cannabis boom was one of the greatest market stories of the 2010s.

Tilray, Inc. ( NasdaqGS:TLRY ) rode the cannabis wave, becoming one of the major players in the sector and developing into a multi-billion corporation.

Yet, for some reason, the interest from institutional investors remains surprisingly low. Institutions often own shares in more established companies, while it's not unusual to see insiders own a fair bit of smaller companies.

Latest Developments

After a parabolic move in Q1, the stock went through much tamer Q2, oscillating between $13 and $21. While still a significant range, it pales in comparison to the yearly high of $64.

Obviously, the euphoria of the Tilray-Aphria merger that created the world's largest cannabis company by revenue has now subsided.

The average 5-year monthly Beta is at 2.62, showing that the stocks moves on average that many times more than the overall market. Unsurprisingly, some investors don't want to deal with that volatility.

Meanwhile, the main catalyst to propel the stock forward remains the elusive US federal legalization. However, Senate Majority leader Chuck Schumer admitted that he doesn't have the necessary support to pass the cannabis legislation yet. With the Senate under a 50-50 split between the Democrats and Republicans, he needs at least 60 votes to get the pass.

With a market capitalization of US$6.6b, Tilray is rather large. We'd expect to see institutional investors on the register. Companies of this size are usually well known to retail investors, too. In the chart below, we can see that institutional investors have bought into the company, but not in share you'd expect from a company of this size.

View our latest analysis for Tilray

What Does The Institutional Ownership Tell Us About Tilray?

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

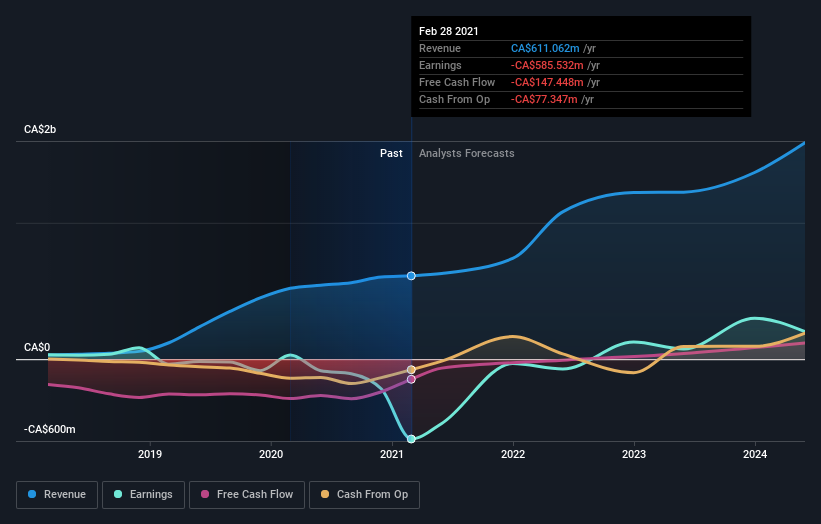

Tilray already has institutions on the share registry. Indeed, they own a respectable stake in the company. This suggests some credibility amongst professional investors. But we can't rely on that fact alone since institutions make bad investments sometimes, just like everyone does. If multiple institutions change their view on a stock simultaneously, you could see the share price drop fast. It's, therefore, worth looking at Tilray's earnings history below. Of course, the future is what really matters - but the question remains on how much US federal legalization is baked into the future projections.

Hedge funds do not own Tilray. Brendan Kennedy is currently the largest shareholder, with 2.1% of shares outstanding. With 1.9% and 1.6% of the shares outstanding, respectively, ETF Managers Group LLC and Heights Capital Management, Inc. are the second and third largest shareholders.

A deeper look at our ownership data shows that the top 25 shareholders collectively hold less than half of the register, suggesting a large group of smallholders where no single shareholder has a majority.

While studying institutional ownership for a company can add value to your research, it is also good to research analyst recommendations to get a deeper understanding of a stock's expected performance. A reasonable number of analysts cover the stock, so it might be useful to find out their aggregate view on the future.

Insider Ownership Of Tilray

While the precise definition of an insider can be subjective, almost everyone considers board members to be insiders. Company management runs the business, but the CEO will answer the board, even if they are a member of it.

Most consider insider ownership a positive because it can indicate the board is well aligned with other shareholders. However, on some occasions, too much power is concentrated within this group.

Our most recent data indicates that insiders own some shares in Tilray. The insiders have a meaningful stake worth US$285m. Most would see this as a real positive. It is good to see this level of investment by insiders. You can check here to see if those insiders have been buying recently.

General Public Ownership

The general public -- including retail investors -- owns 90% of Tilray. This level of ownership gives investors from the wider public some power to sway key policy decisions such as board composition, executive compensation, and the dividend payout ratio.

Notably, executive compensation is high, with the CEO Irwin Simon being compensated twice the amount of the average compensation for similarly sized companies. Mr.Simon is a former CEO of Aphria who took over after the previously mentioned merger was completed.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too. Be aware that Tilray is showing 3 warning signs in our investment analysis , and 1 of those doesn't sit too well with us...

Ultimately the future is most important . You can access this free report on analyst forecasts for the company .

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full-year annual report figures.

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com