Is it Time to Add Selective Insurance (SIGI) to Your Portfolio?

Selective Insurance Group, Inc.’s SIGI compelling portfolio, high retention ratio, pure renewal price increase, new business growth, rise in investment income and solid capital position make it worth adding to one’s portfolio.

Earnings of this property and casualty insurer have risen 9.6% over the last five years. It has a VGM Score of A. The Style Score rates stocks on their combined weighted styles, helping to identify those with the most attractive value, best growth, and most promising momentum.

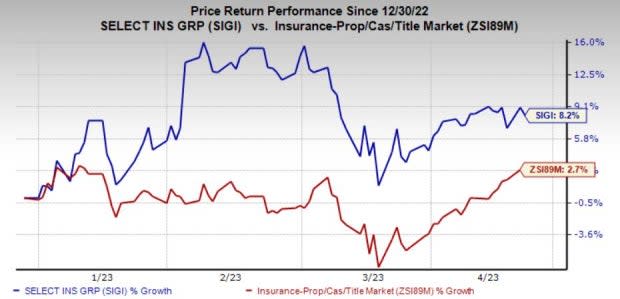

Zacks Rank & Price Performance

Selective Insurance currently has a Zacks Rank #2 (Buy). Year to date, the stock has gained 8.2% compared with the industry’s increase of 2.7%.

Image Source: Zacks Investment Research

Northbound Estimate Revision

The Zacks Consensus Estimate for 2023 and 2024 earnings has moved 0.8% and 0.7% north each in the past seven days, reflecting analyst optimism.

Return on Equity

SIGI has been delivering double-digit returns on equity for the last nine years. Banking on operational strength, the insurer is set to generate 12% ROE in 2023.

Optimistic Growth Projection

The Zacks Consensus Estimate for Selective Insurance’s 2023 earnings is pegged at $6.62, indicating an increase of 31.6% on 13.7% higher revenues of $4.2 billion. The consensus estimate for 2024 earnings is pegged at $7.60, indicating an increase of 14.9% on 10.2% higher revenues of $4.6 billion.

The long-term earnings growth rate is currently pegged at 18.9%, better than the industry average of 14.6%.

Growth Drivers

Solid renewal pricing in standard commercial lines and excess and surplus lines, solid retention rates in standard commercial and personal lines, and an increase in exposure should help SIGI deliver continued improvement in premiums. Notably, the insurer’s premium has risen at a six-year (2017-2022) CAGR of 7.1%.

Continued premium growth across its segments has been driving the top line, which grew at a six-year (2017-2022) CAGR of 6.3%.

Renewal pure price increases, higher direct new business and favorable E&S Lines marketplace conditions should help retain the positive momentum at The Excess and Surplus Lines (E&S) segment.

Selective Insurance has been delivering impressive investment results. For 2023, Selective Insurance projects an after-tax net investment income of $300 million, up from the prior guidance of $215 million that includes after-tax net investment income from alternative investments of $30 million, up from $7 million guided earlier.

Selective Insurance flaunts a sound capital structure and remains committed to enhancing shareholders’ value while improving its financial strength and underwriting capabilities. It thus scores strongly with credit rating agencies.

SIGI has an impressive dividend history, having increased dividends at a nine-year CAGR (2015-2023) of 8.8%. Dividends currently yield 1.2%, banking on sustained solid operational performance. The insurer also has an $84.2 million share buyback authorization under its kitty.

Being a property and casualty insurer, Selective Insurance remains exposed to catastrophe losses from natural disasters and weather-related events, which induce volatility in results. Nonetheless, for 2023, Selective Insurance estimates a GAAP combined ratio of 96.5%, including net catastrophe losses of 4.5 points.

SIGI has a Value Score of B. This style score helps find the most attractive value stocks. Back-tested results have shown that stocks with a Style Score of A or B combined with a Zacks Rank #1 (Strong Buy) or #2 offer better returns.

Other Stocks to Consider

Some other top-ranked stocks from the property and casualty insurance industry are Kinsale Capital Group, Inc. KNSL, Everest Re Group, Ltd. RE and Cincinnati Financial Corporation CINF. While Kinsale Capital sports a Zacks Rank #1, Everest Re and Cincinnati Financial carry a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Kinsale Capital has a solid track record of beating earnings estimates in each of the last four quarters, the average being 13.83%. Year to date, KNSL has gained 21.3%.

The Zacks Consensus Estimate for KNSL’s 2023 and 2024 earnings per share is pegged at $9.92 and $11.94, indicating a year-over-year increase of 27.1% and 20.4%, respectively.

Everest Re beat estimates in each of the last four quarters, the average being 18.41%.

The Zacks Consensus Estimate for RE’s 2023 and 2024 earnings per share is pegged at $44.28 and $53.54, indicating a year-over-year increase of 63.5% and 20.9%, respectively. Year to date, RE has gained 9.5%.

The Zacks Consensus Estimate for Cincinnati Financial’s 2023 and 2024 earnings per share is pegged at $5.13 and $5.92, indicating a year-over-year increase of 21% and 15.4%, respectively. Year to date, SIGI has gained 9.1%.

The Zacks Consensus Estimate for CINF’s 2023 and 2024 revenues is pegged at $8.6 billion and $9.3 billion, indicating a year-over-year increase of 7.5% and 8.3%, respectively.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cincinnati Financial Corporation (CINF) : Free Stock Analysis Report

Everest Re Group, Ltd. (RE) : Free Stock Analysis Report

Selective Insurance Group, Inc. (SIGI) : Free Stock Analysis Report

Kinsale Capital Group, Inc. (KNSL) : Free Stock Analysis Report