Time to Buy Bumble Stock as It Outperforms Rival?

Investors may be hesitant to invest in dating apps and social media platforms after a rough year for most of these stocks. Dating app platform operators Bumble BMBL and Match MTCH are down big this year while Meta Platforms META and Snap SNAP have been crushed in the social media realm.

However, investors may be wondering if this year’s decline is an opportunity to invest in Bumble as it starts to really challenge its larger and older rival Match.

Image Source: Zacks Investment Research

IPO

Bumble was founded in 2014 and launched its IPO in 2021. BMBL stock spiked 63% on the first day of trading. BMBL shares went as high as $76 per share after pricing its IPO at $43 a share.

Bumble and Match operate one of the world’s most popular and highest-grossing dating apps.

Bumble Inc. is the parent company of Badoo and Bumble with the ladder being the first dating app centered around social interaction initiated by women.

Bumble is seen as the rival to Tinder which is a Match Group brand. In addition to Tinder, Match Group brands include Match.com, PlentyOfFish, Hinge, and BLK. Match’s paid users of 16.5 million trumps Bumble’s 3.3 million, as both companies look to continue expanding their dating app services.

Growth & Outlook

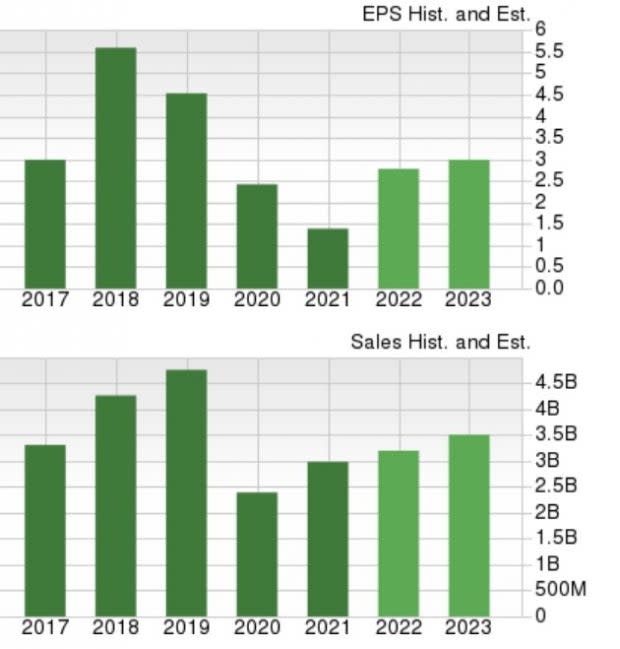

Year over year BMBL earnings are expected to decline -86% to $0.23 per share. However, earnings estimates are largely up from $0.11 a share 90 days ago. FY23 earnings are set to decline another -16% to $0.19 per share. Earnings estimates for FY23 are slightly down from $0.25 a share last quarter.

Top line growth is expected, with sales set to jump 17% this year and another 16% in FY23 to $1.05 billion. The top line growth is impressive as bottom line growth usually catches up once early-stage companies such as Bumble adjust to operating costs in their respective industry.

Pivoting to MTCH, while the stock is further along the profitability line earnings estimate revisions are trending down for FY23 and FY24. MTCH earnings are now expected to rise 19% in 2022 at $1.65 per share compared to $2.35 a share 90 days ago. FY23 earnings are projected to rise 40% to $2.32 per share, which is also down from estimates of $2.82 a share last quarter.

Sales are forecasted to rise 7% this year and another 8% in FY23 to $3.46 billion. However, this would still represent a -24% decrease from pre-pandemic levels as competition from Bumble is certainly slowing the company’s top line growth.

Image Source: Zacks Investment Research

With the two companies directly competing with their Bumble and Tinder apps, the trend in earnings estimate revisions and top line sales growth reflects which company is taking market share.

To that note, BMBL appears to be more attractive at the moment and could continue narrowing the profitability gap between them as the company matures.

Performance & Valuation

Year to date BMBL is down -34% to underperform the S&P 500’s -18% but beat MTCH’s -64%. Since BMBL begin publicly trading last February the stock is now down -68% but slightly above MTCH’s decline.

Image Source: Zacks Investment Research

BMBL stock is now 33% from its 52-week highs with MTCH 67% from its peaks. Such large falls may have some thinking the stocks are oversold and gauging valuation can help distinguish this.

Currently trading around $22 per share BMBL has a forward P/E of 98X. This is much higher than MTCH which trades at $46 a share and 28.8X forward earnings. In this regard, MTCH stock is certainly more attractive with the Internet-Software Industry average at 44.7X.

With BMBL less than two years removed from its IPO, this is somewhat expected and price to sales can give another perspective as to the value these stocks offer investors. We can see from the nearby chart that BMBL trades at 3.3X sales to put it solidly below MTCH’s 4.4X.

Image Source: Zacks Investment Research

Bottom Line

BMBL currently sports a Zacks Rank #2 (Buy) in correlation with 2022 earnings estimates significantly rising over the last quarter. In contrast, MTCH lands a Zacks Rank #5 (Strong Sell) as 2022 earnings estimates have largely declined as the company faces increased competition from Bumble along with the challenging economy.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bumble Inc. (BMBL) : Free Stock Analysis Report

Match Group Inc. (MTCH) : Free Stock Analysis Report

Snap Inc. (SNAP) : Free Stock Analysis Report

Meta Platforms, Inc. (META) : Free Stock Analysis Report