TipRanks ‘Perfect 10’ List: There’s an Opportunity Brewing in These 3 Top-Rated Stocks

There are thousands of publicly traded companies on Wall Street’s stock exchanges, tens of thousands of investors buying and selling practically every hour, and more thousands of professional stock analysts watching every detail of these transactions. It’s enough raw data that even Mr. Spock would have trouble calculating the odds in his head.

Spock would turn to the Enterprise computer, which we haven’t got – but we do have the Smart Score, a sophisticated data parsing and collation tool, powered by AI-driven algorithms. The Smart Score gathers data on those thousands of stocks, and then rates each stock against a set of 8 separate factors that have been shown to match up with future outperformance. In the end, each stock gets a single-digit score on a scale of 1 to 10 – with a ‘Perfect 10’ indicating a stock that, quite logically, deserves a second look.

So, let’s do that. We’ve opened up the TipRanks database and pulled up the details on 3 of these top-rated, ‘Perfect 10’ stocks, and gone on to find out what the analysts have to say about them. Here they are, with the analyst commentaries.

Phillips 66 (PSX)

The first name on our list is Phillips 66, one of the world’s major oil companies. This firm, with its $44.5 billion market cap, has been reaping the gains from oil’s post-pandemic rise and saw its annual revenues jump from $111 billion in 2021 to $170 billion last year. Phillips generates these numbers by bringing crude oil, natural gas, and natural gas products – mainly liquids – to the refineries, and then marketing a wide range of refined hydrocarbon products, including automotive and fuels, fuel and lubricating oils, petrochemicals, and other industrial chemicals.

The company currently has 13 active refineries, and markets its fuels under several brand names, including the widely known Conoco, 76, and the eponymous Phillips 66. In fact, the company’s shield logo is one of the more widely recognized branding symbols on US highways. Phillips products are used both in and out of the transportation sector, in the aviation industry, in industrial chemicals, in agriculture, and in the pharmaceutical business.

In its most recent quarterly report, for 1Q23, Phillips showed a slowdown in revenue generation, with the $35.1 billion top line slipping from the $36.6 billion reported in the year-ago period. At the same time, the revenues beat expectations by $562.74 million. The bottom-line earnings, reported as a non-GAAP EPS of $4.21, were 65 cents per share better than the forecasts.

Phillips finished Q1 with deep pockets, including $7 billion in cash and liquid assets, as well as $6.2 billion in ‘committed capacity’ from its credit facilities. In the quarter, the company generated $2.5 billion in operating cash flow, of which $1.2 billion was free cash flow. Some $1.3 billion was returned to shareholders during the quarter, through both dividend payments and repurchases.

The div payments deserve a closer look. Phillips increased its payment earlier this year, and the last payment sent, on June 1 for $1.05 per common share, represented the second payment at the higher rate. The current dividend, at $4.20 annualized, is yielding 4.3%.

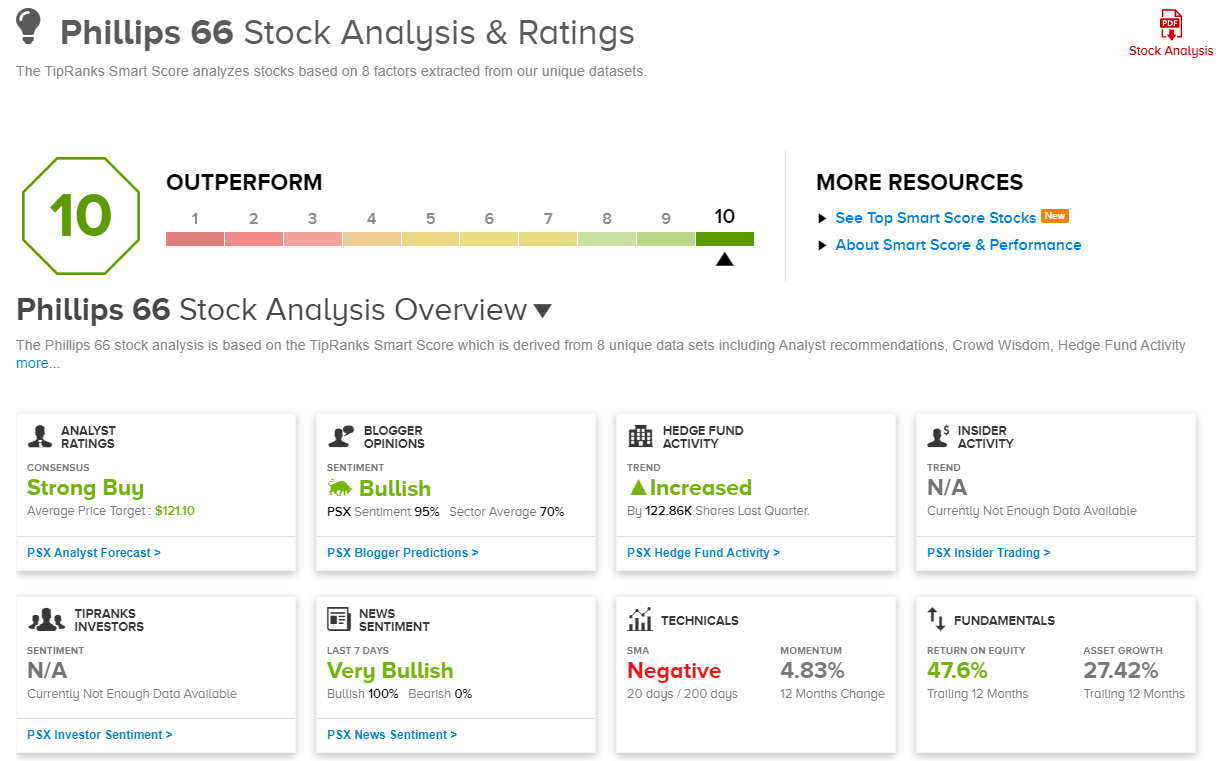

On the Smart Score, PSX gets a boost from its fundamental factors, which include a 47.6% return on equity for the trailing 12 month period, as well as from 100% positive news sentiment and 95% positive sentiment from the financial bloggers.

Analyst Jason Gabelman, from TD Cowen, is bullish here, noting Phillips’ overall strong performance in a vital industry. He writes, “We expect refining operations to improve and its non-refining exposure to once again become a more appreciated differentiator. Refinery operations weakened in 2021-22 given elevated planned and unplanned maintenance. We anticipate operations to move back to levels consistent with pre-Covid performance, near best-in-class, including $7/bbl opex and 93% refinery utilization.”

“Moreover,” Gableman went on to add, “as industry refining margins continue to normalize from peak-cycle 2022 over the next couple years, we anticipate PSX higher non-refining earnings mix and growth to become a more appreciated factor.”

Gabelman’s Outperform (Buy) rating comes along with a $123 price target implying an upside of 27% for the year ahead. (To watch Gabelman’s track record, click here.)

The Strong Buy consensus rating on PSX shares is based on 10 recent reviews, with a breakdown of 8 to 2 in favor of Buys over Holds. The stock’s $97.13 trading price and $121.10 average price target suggest a one-year upside potential of 25%. (See Phillips 66’s stock forecast.)

GFL Environmental (GFL)

For the second stock on our list, we’ll turn to a sector that most people don’t think about, but wouldn’t want to live without – waste management services. GFL, a Toronto-based company, is active across Canada, serving commercial, industrial, institutional, municipal, and residential customers. The company’s activities include disposal of liquid and solid waste, including general garbage, recyclables, commercial dumpster collection, construction debris, automotive fluids, hazardous wastes – and that’s only the beginning of the list. GFL even works with soil reclamation.

Waste management – or garbage collection, as we usually think of it – is big business, far bigger than most of us ever imagine. GFL has a market cap of $13.76 billion in US currency, and saw more than C$6.76 billion ($5.11 billion) in revenue last year. The company works from a network of facilities that include everything from material recovery plants to traditional landfill, and organic processing stations to soil remediation sites.

In the first quarter of this year, GFL boasted revenues of C$1.8 billion ($1.36 billion), beating the Street’s C$1.68 billion ($1.27 billion) forecast. The company’s bottom line of C$0.08 per share came in C$0.11 ahead of expectations. The firm’s revenue generation is on a generally upward trajectory, growing 22% from 2021 to 2022, and the 1Q23 top line was up 28% from the prior-year period.

The Smart Score here shows several points for investors to consider. Technical factors are solid; the 12-month-change momentum came in at 50.88%, and the simple moving average (20 days over 200 days) is positive. The financial bloggers are 100% bullish, and the hedge funds tracked by TipRanks increased their holdings here by 743,000 shares last quarter.

With all of these sound metrics, what caught the eye of 5-star analyst Michael Doumet, of Scotiabank, was this company’s fast growth. Doumet says, “GFL’s growth story is well understood: it is executing the playbook its larger peers executed decades ago (but is doing so, when industry pricing discipline is improved)… GFL’s attractive market selection (i.e., >65% in secondary/less competitive markets) provides the basis for above-market margin expansion, and its ability to further densify its existing operating regions provide it with meaningful runway to execute accretive M&A. De-leveraging to below 4x net debt before the end of 2023, with three planned divestitures (expected to be completed before the end of Q2/23), and more so beyond, could aid in a positive re-rate.”

Looking ahead, Doumet puts an Outperform (Buy) rating here, with a C$58 (US$43.87) price target that suggests an upside of 17.7% for the next 12 months. (To watch Doumet’s track record, click here.)

It’s clear, from the unanimous Strong Buy consensus rating based on 10 positive analyst reviews, that Wall Street is bullish on this stock. The shares are selling for US$37.28, and the US$43.81 average price target implies a gain of 17% on the one-year time horizon. (See GFL’s stock forecast.)

Tecnoglass, Inc. (TGLS)

Last on our list, Tecnoglass, is a leader in a specialty market within the construction materials sector. The company provides architectural glass, windows, and related aluminum products used in the construction industry, and its products can be found in everything from single-family homes to multi-family apartment dwellings to commercial buildings. The firm is based in Colombia, and holds the #1 position in the Latin American market for architectural glass – and the #2 position in the US market.

Tecnoglass boasts a massive production facility in its home country, a 4.1 million square foot, vertically integrated, state-of-the-art factory that is capable of meeting the needs of more than 1,000 global customers. While Tecnoglass is active around the world, and leads its market in Latin America, some 90% of its revenue come from sales to the US construction market, especially in the fast-growing state of Florida. We should note that Florida is closely linked to Latin America, by a combination of geography and immigration.

The US real estate market – particularly the residential market, was hot in 2022, and Tecnoglass saw a sharp rise in revenues and earnings. At the top line, the company’s 2022 revenue was up 44% year-over-year to hit $716.6 million. In the last quarterly report, for 1Q23, the upward trend continued. The company reported a top line of $202.6 million, up 50% y/y and beating the forecast by $11.6 million. The non-GAAP EPS figure, of $1.08 per share, was 18 cents per share better than had been expected – and was more than double the 53-cent EPS figure reported in the year-ago quarter.

When we look at Tecnoglass’s Smart Score, we find powerful momentum from the technical factors – a 12-month change of 183%. The news sentiment is 100% bullish, as are the financial bloggers. Positive crowd wisdom and increasing hedge activity round out the Perfect 10; last quarter, the hedges increased their holdings of TGLS by 292,400 shares.

These strong growth figures caught the eye of Stanley Elliott, 5-star analyst from Stifel. Elliott writes of Tecnoglass, “TGLS has experienced robust growth driven by market share gains, new product line expansions (entered residential in 2017), and geographic expansion, all trends we expect will continue into the foreseeable future. Further, TGLS has exposure to relatively attractive portions of the end market, with nearly 90% of sales in Florida and nearly 30% from R&R. Shares currently trade at a discount to its closest peer, which we believe provides an attractive entry point opportunity.”

These comments support Elliott’s initiation of coverage with a Buy rating and $60 price target indicating confidence in a 26% one-year gain. (To watch Elliott’s track record, click here.)

While there are only 4 recent analyst reviews of this stock, they are all positive – giving TGLS its Strong Buy consensus rating. The shares have an average price target of $54.75 and a trading price of $47.56, suggesting a 15% upside for the year ahead. (See Tecnoglass’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.