Toast (NYSE:TOST) Posts Better-Than-Expected Sales In Q4, Stock Jumps 11.8%

Restaurant software platform Toast (NYSE:TOST) reported Q4 FY2023 results topping analysts' expectations , with revenue up 34.7% year on year to $1.04 billion. It made a GAAP loss of $0.07 per share, down from its loss of $0.04 per share in the same quarter last year.

Is now the time to buy Toast? Find out by accessing our full research report, it's free.

Toast (TOST) Q4 FY2023 Highlights:

Revenue: $1.04 billion vs analyst estimates of $1.02 billion (1.9% beat)

EPS: -$0.07 vs analyst estimates of -$0.11 (35.8% beat)

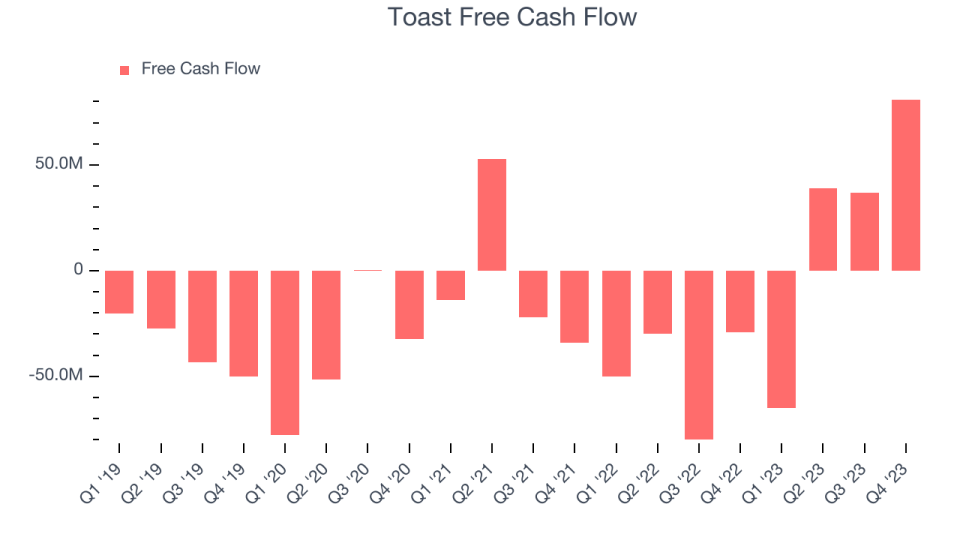

Free Cash Flow of $81 million, up 119% from the previous quarter

Gross Margin (GAAP): 21.8%, up from 20.8% in the same quarter last year

Market Capitalization: $10.89 billion

Founded by three MIT engineers at a local Cambridge bar, Toast (NYSE:TOST) provides integrated point-of-sale (POS) hardware, software, and payments solutions for restaurants.

Hospitality & Restaurant Software

Enterprise resource planning (ERP) and customer relationship management (CRM) are two of the largest software categories dominated by the likes of Microsoft, Oracle, and Salesforce.com. Today, the secular trend of mass customization is driving vertical software that customizes ERP and CRM functions for specific industry requirements. Restaurants are a prime example where a set of customized software providers have sprung up in recent years to create unique operating systems that blend tax and accounting software, order management and delivery, along with supply chain management. Hotels and other hospitality providers are another example.

Sales Growth

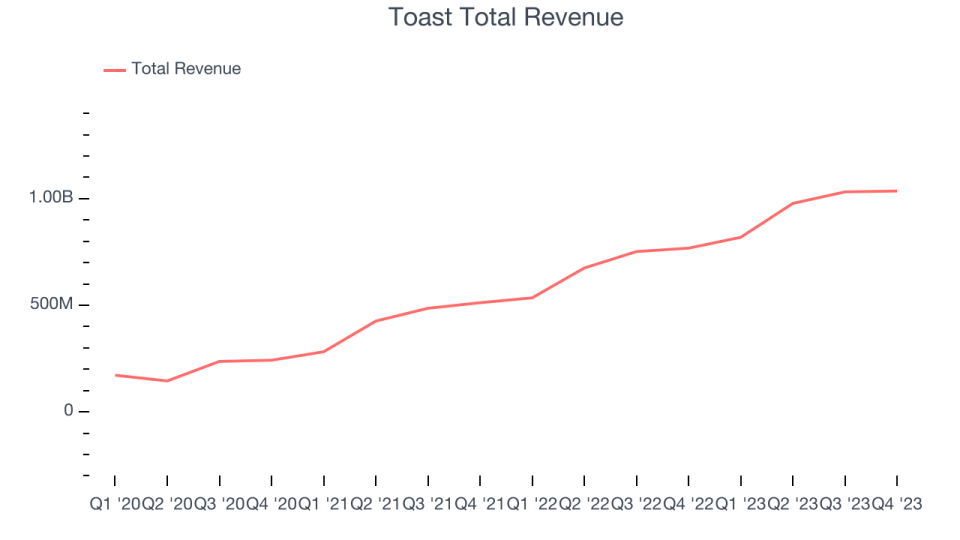

As you can see below, Toast's revenue growth has been exceptional over the last two years, growing from $512 million in Q4 FY2021 to $1.04 billion this quarter.

Unsurprisingly, this was another great quarter for Toast with revenue up 34.7% year on year. However, its growth did slow down compared to last quarter as the company's revenue increased by just $4 million in Q4 compared to $54 million in Q3 2023. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Toast's free cash flow came in at $81 million in Q4, turning positive over the last year.

Toast has burned through $92 million of cash over the last 12 months, resulting in a negative 2.4% free cash flow margin. This low FCF margin stems from Toast's poor unit economics or a constant need to reinvest in its business to stay competitive.

Key Takeaways from Toast's Q4 Results

It was encouraging to see Toast narrowly top analysts' revenue expectations this quarter. We also found the continued momentum in free cash flow promising. Zooming out, we think this was a decent quarter, showing that the company is staying on target. The stock is up 11.8% after reporting and currently trades at $21.5 per share.

So should you invest in Toast right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.