Is It Too Late to Buy StoneCo Ltd. Stock?

Fintech is a hot topic in emerging markets, like Brazil, where StoneCo (NASDAQ: STNE) operates. The company offers various banking and fintech services, and its shares have risen more than 60% during the past year.

Despite its recent momentum, shares remain well off their past highs, raising the question: Is the stock at the beginning of a significant run? Or should investors be wary of this bounce?

Unfortunately, there is one red flag that may spoil the fun.

Here is what you need to know.

First, what is StoneCo?

Most American investors have probably never heard of StoneCo. You should always know what you're investing in, so this is a good chance for a brief introduction. StoneCo is a banking and fintech company in Brazil. It provides hardware and software for merchants to process payments, financial services, and lending to help businesses operate. You could think of StoneCo as a Brazilian version of Block's Square ecosystem.

The company is focusing more on the banking side of its business. In January, it said that it had acquired a banking license, which lets StoneCo offer more financial products and services. Nearly 3.5 million merchants use StoneCo, which grew an impressive 37% year over year in the fourth quarter.

Growth could last years if StoneCo is successful. There are roughly 15 million companies in Brazil, and 93% of them are small businesses that would benefit from the turnkey tools that StoneCo can provide.

So, what's the problem?

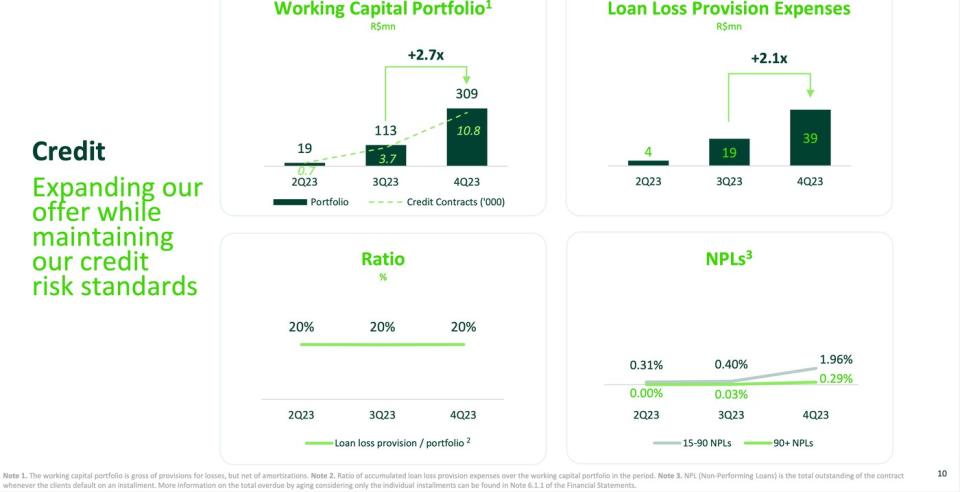

Unfortunately, part of banking involves lending money, and StoneCo's enthusiasm for lending is a potential problem for investors. You can see below how Q4 credit performance turned out:

As StoneCo lends more, provisions for losses rise, too. This is inevitable because no lender will ever be perfect. Things happen. However, non-performing loans (NPLs), which are essentially past-due loans that may never be repaid, ticked notably higher during Q4.

The investment picture is much cleaner when companies don't have to analyze risk. Lending can be a mysterious black box. How can shareholders know how well StoneCo will do at evaluating credit and determining whom to lend to and how much? You can't know until you start seeing losses pile up. This happened once already a few years back when StoneCo suffered heavy losses and had to pause issuing new loans.

What happens in a recession when merchants struggle and defaults rise? These are all important questions, but they must be asked as StoneCo expands its lending business. Upstart, a lending platform built around artificial intelligence (AI), was doing very well until rising rates tripped it up and forced loans that it wanted to sell back onto its balance sheet. It's not apples-to-apples, but it shows how difficult lending can be and how much more risk the business takes when loans are involved.

What should investors do?

You can decide whether StoneCo's credit exposure ruins your appetite for shares. At the very least, investors should exercise some caution. Shares currently look cheap at just 12 times this year's estimated earnings. Block, my earlier comparison, trades at twice the valuation StoneCo does. A low valuation can help negate some of the investment risk.

Plus, the credit exposure is still minimal. Its 39 million reals ($7.8 million) in loan loss provisions still pales compared to StoneCo's R$564 million net income in Q4. Perhaps I'm making something out of nothing.

Remember that the banking license could dramatically change the business, but change isn't always good. Investors willing to take that risk early on should consider buying stock slowly and often so there's no panic if things suddenly start going south.

Time will tell how this all shakes out.

Should you invest $1,000 in StoneCo right now?

Before you buy stock in StoneCo, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and StoneCo wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Justin Pope has positions in Upstart. The Motley Fool has positions in and recommends Block, StoneCo, and Upstart. The Motley Fool has a disclosure policy.

Is It Too Late to Buy StoneCo Ltd. Stock? was originally published by The Motley Fool