Is Tootsie Roll Industries (NYSE:TR) A Risky Investment?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Tootsie Roll Industries, Inc. (NYSE:TR) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Tootsie Roll Industries

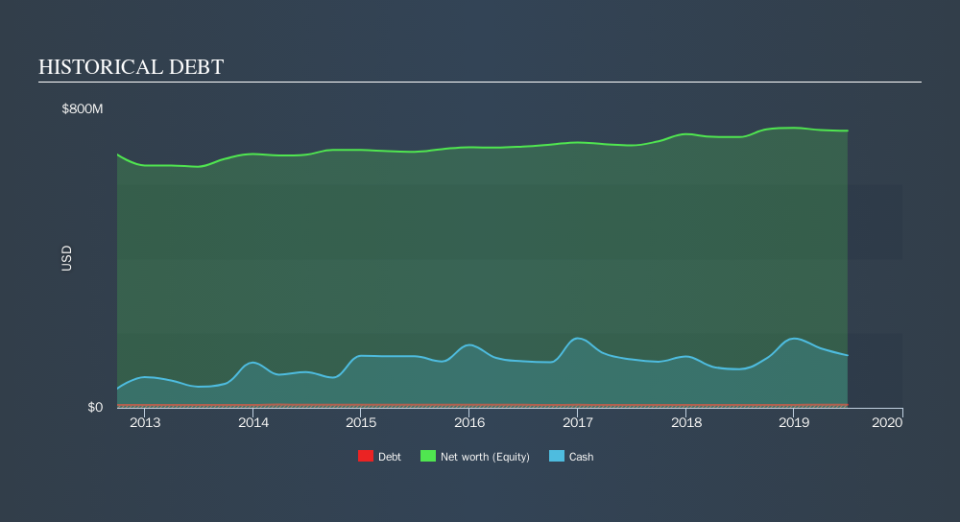

What Is Tootsie Roll Industries's Net Debt?

As you can see below, Tootsie Roll Industries had US$8.19m of debt, at June 2019, which is about the same the year before. You can click the chart for greater detail. But it also has US$140.6m in cash to offset that, meaning it has US$132.4m net cash.

How Strong Is Tootsie Roll Industries's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Tootsie Roll Industries had liabilities of US$60.3m due within 12 months and liabilities of US$145.6m due beyond that. Offsetting this, it had US$140.6m in cash and US$39.9m in receivables that were due within 12 months. So its liabilities total US$25.4m more than the combination of its cash and short-term receivables.

This state of affairs indicates that Tootsie Roll Industries's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the US$2.36b company is struggling for cash, we still think it's worth monitoring its balance sheet. While it does have liabilities worth noting, Tootsie Roll Industries also has more cash than debt, so we're pretty confident it can manage its debt safely.

While Tootsie Roll Industries doesn't seem to have gained much on the EBIT line, at least earnings remain stable for now. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Tootsie Roll Industries will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Tootsie Roll Industries may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, Tootsie Roll Industries recorded free cash flow worth 70% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Tootsie Roll Industries has US$132.4m in net cash. The cherry on top was that in converted 70% of that EBIT to free cash flow, bringing in US$80m. So is Tootsie Roll Industries's debt a risk? It doesn't seem so to us. Over time, share prices tend to follow earnings per share, so if you're interested in Tootsie Roll Industries, you may well want to click here to check an interactive graph of its earnings per share history.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.