Transportadora de Gas del Sur SA (TGS): A Deep Dive into Its Overvaluation Status

Transportadora de Gas del Sur SA (NYSE:TGS) recently experienced a daily gain of 6.73%, despite a 3-month loss of -8.86%. The company's Earnings Per Share (EPS) currently stands at 1.12. These figures present a compelling question: Is the stock significantly overvalued? This article aims to provide a comprehensive analysis of TGS's valuation, encouraging readers to delve into the subsequent sections for a deeper understanding.

Company Introduction

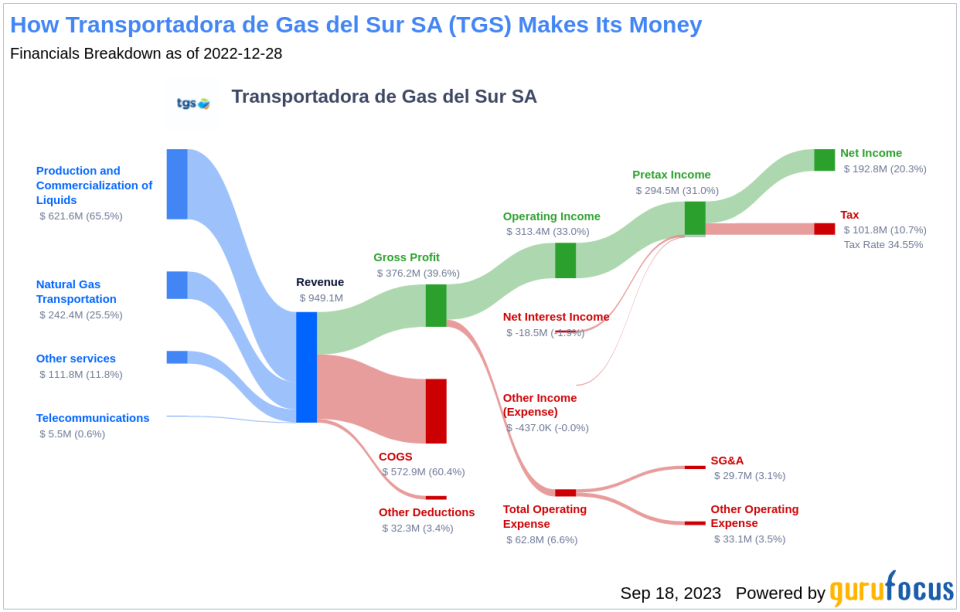

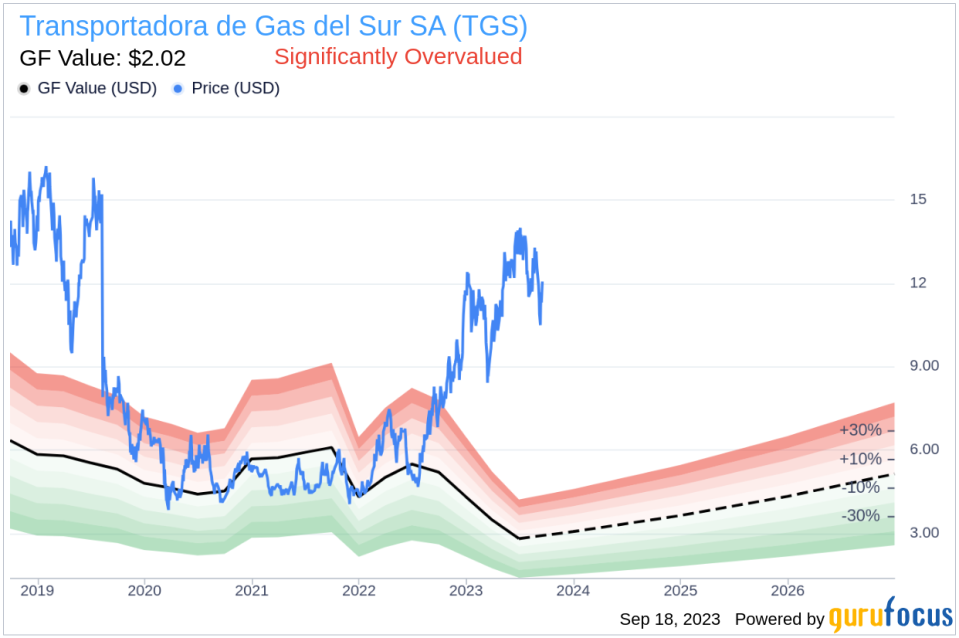

Transportadora de Gas del Sur SA is one of the largest transporters of natural gas in Latin America. With a diverse operating portfolio that includes natural gas transportation, production and commercialization of liquids, other services, and telecommunications, the company has managed to generate substantial revenue predominantly from Argentina. Despite a current stock price of $12.06, the GF Value, our proprietary measure of fair value, stands at $2.02, suggesting a significant overvaluation. This discrepancy between the stock price and GF Value sets the stage for a deeper exploration of the company's value.

Summarizing GF Value

The GF Value is a unique measure of a stock's intrinsic value, calculated based on historical trading multiples, a GuruFocus adjustment factor, and future business performance estimates. When the stock price significantly deviates from the GF Value Line, it suggests overvaluation or undervaluation. In the case of TGS, with a market cap of $1.80 billion and a stock price of $12.06 per share, the stock appears to be significantly overvalued.

As a result, the long-term return of TGS's stock is likely to be much lower than its future business growth. However, this does not detract from the fact that TGS has shown substantial profitability and growth.

Link: These companies may deliver higher future returns at reduced risk.

Financial Strength

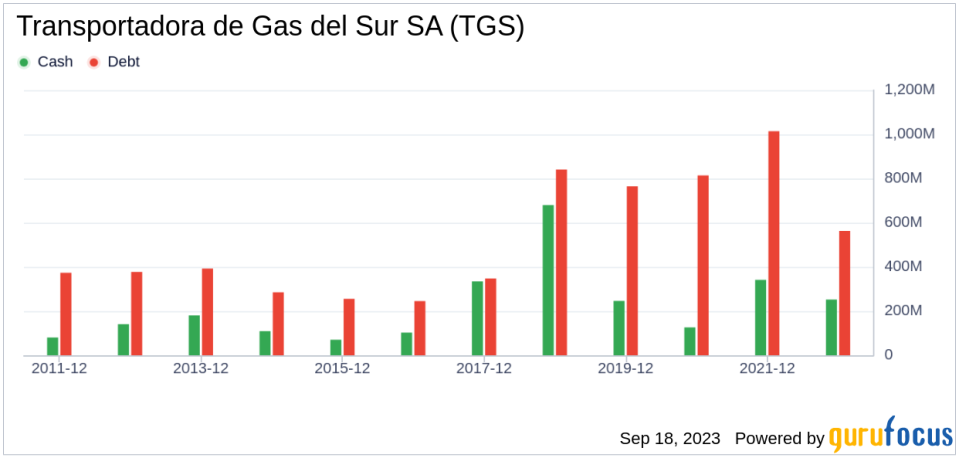

Investing in companies with poor financial strength can pose a high risk of permanent capital loss. To mitigate this risk, investors must review a company's financial strength before purchasing shares. TGS has a cash-to-debt ratio of 0.84, ranking better than 56.67% of 1027 companies in the Oil & Gas industry. Overall, TGS's financial strength is fair, with a score of 7 out of 10.

Profitability and Growth

Companies with consistent profitability are often less risky investments. TGS has been profitable 9 out of the past 10 years, boasting an operating margin of 28.09% that ranks better than 73.05% of 976 companies in the Oil & Gas industry. The company's overall profitability rank is 10 out of 10, indicating strong profitability.

Furthermore, TGS's growth has been impressive, with a 3-year average annual revenue growth rate of 18.8%. This ranks better than 67.44% of 857 companies in the Oil & Gas industry. The 3-year average EBITDA growth rate is 19.6%, ranking better than 57.09% of 825 companies in the same industry.

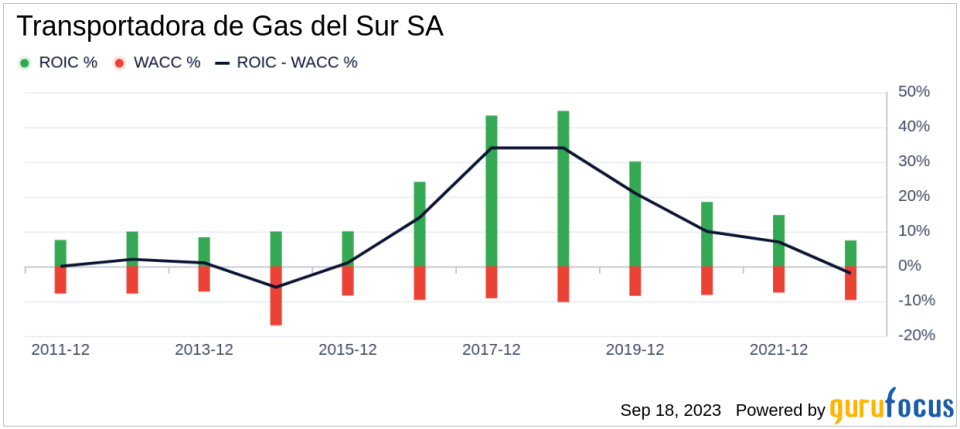

Another measure of a company's profitability is the comparison between its return on invested capital (ROIC) and its weighted average cost of capital (WACC). If the ROIC is higher than the WACC, it indicates that the company is creating value for shareholders. Over the past 12 months, TGS's ROIC was 8.72, while its WACC came in at 9.92.

Conclusion

In summary, TGS's stock appears to be significantly overvalued. Despite this, the company's financial condition is fair, and its profitability is strong. Its growth ranks better than 57.09% of 825 companies in the Oil & Gas industry. For more information about TGS's stock, check out its 30-Year Financials here.

To find high-quality companies that may deliver above-average returns, consider GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.