Triumph Bancorp (NASDAQ:TBK) sheds 4.6% this week, as yearly returns fall more in line with earnings growth

We think all investors should try to buy and hold high quality multi-year winners. And we've seen some truly amazing gains over the years. To wit, the Triumph Bancorp, Inc. (NASDAQ:TBK) share price has soared 302% over five years. If that doesn't get you thinking about long term investing, we don't know what will. Unfortunately, though, the stock has dropped 4.6% over a week. However, this might be related to the overall market decline of 4.6% in a week.

Since the long term performance has been good but there's been a recent pullback of 4.6%, let's check if the fundamentals match the share price.

View our latest analysis for Triumph Bancorp

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

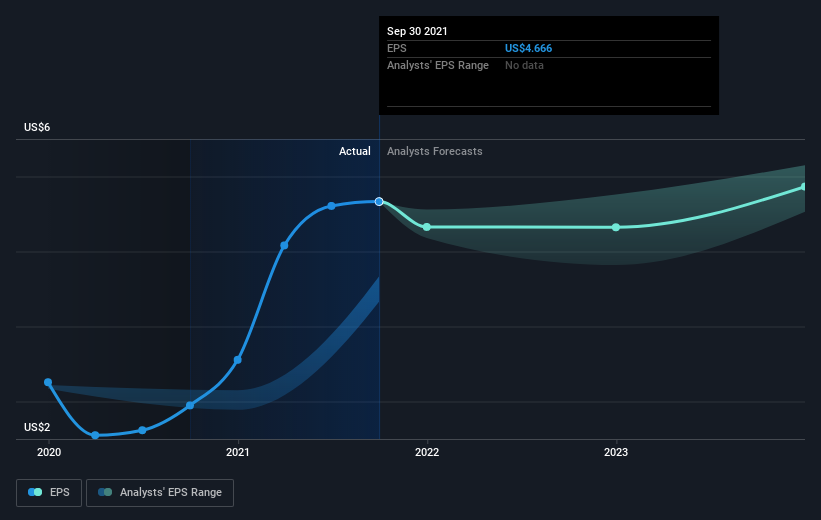

Over half a decade, Triumph Bancorp managed to grow its earnings per share at 36% a year. So the EPS growth rate is rather close to the annualized share price gain of 32% per year. This indicates that investor sentiment towards the company has not changed a great deal. Indeed, it would appear the share price is reacting to the EPS.

You can see how EPS has changed over time in the image below (click on the chart to see the exact values).

We're pleased to report that the CEO is remunerated more modestly than most CEOs at similarly capitalized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. Dive deeper into the earnings by checking this interactive graph of Triumph Bancorp's earnings, revenue and cash flow.

A Different Perspective

It's nice to see that Triumph Bancorp shareholders have received a total shareholder return of 92% over the last year. Since the one-year TSR is better than the five-year TSR (the latter coming in at 32% per year), it would seem that the stock's performance has improved in recent times. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Case in point: We've spotted 1 warning sign for Triumph Bancorp you should be aware of.

We will like Triumph Bancorp better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.