We Like These Underlying Return On Capital Trends At Docebo (TSE:DCBO)

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, we've noticed some promising trends at Docebo (TSE:DCBO) so let's look a bit deeper.

What Is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Docebo is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

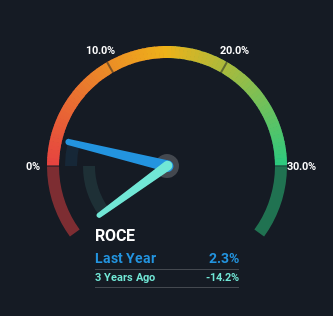

0.023 = US$3.3m ÷ (US$254m - US$111m) (Based on the trailing twelve months to September 2023).

Therefore, Docebo has an ROCE of 2.3%. In absolute terms, that's a low return and it also under-performs the Software industry average of 7.1%.

See our latest analysis for Docebo

In the above chart we have measured Docebo's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Docebo here for free.

What Can We Tell From Docebo's ROCE Trend?

The fact that Docebo is now generating some pre-tax profits from its prior investments is very encouraging. Shareholders would no doubt be pleased with this because the business was loss-making three years ago but is is now generating 2.3% on its capital. Not only that, but the company is utilizing 190% more capital than before, but that's to be expected from a company trying to break into profitability. We like this trend, because it tells us the company has profitable reinvestment opportunities available to it, and if it continues going forward that can lead to a multi-bagger performance.

On a side note, Docebo's current liabilities are still rather high at 44% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

Our Take On Docebo's ROCE

Long story short, we're delighted to see that Docebo's reinvestment activities have paid off and the company is now profitable. And given the stock has remained rather flat over the last three years, there might be an opportunity here if other metrics are strong. With that in mind, we believe the promising trends warrant this stock for further investigation.

If you'd like to know about the risks facing Docebo, we've discovered 3 warning signs that you should be aware of.

While Docebo isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.