Unveiling AtriCure (ATRC)'s Value: Is It Really Priced Right? A Comprehensive Guide

AtriCure Inc (NASDAQ:ATRC) saw a daily gain of 4.3%, despite a 3-month loss of 8.79%. With a Loss Per Share of $0.61, the question arises: is the stock significantly undervalued? We delve into the valuation analysis of AtriCure (NASDAQ:ATRC) to answer this question and provide a comprehensive understanding of the company's intrinsic value.

Company Introduction

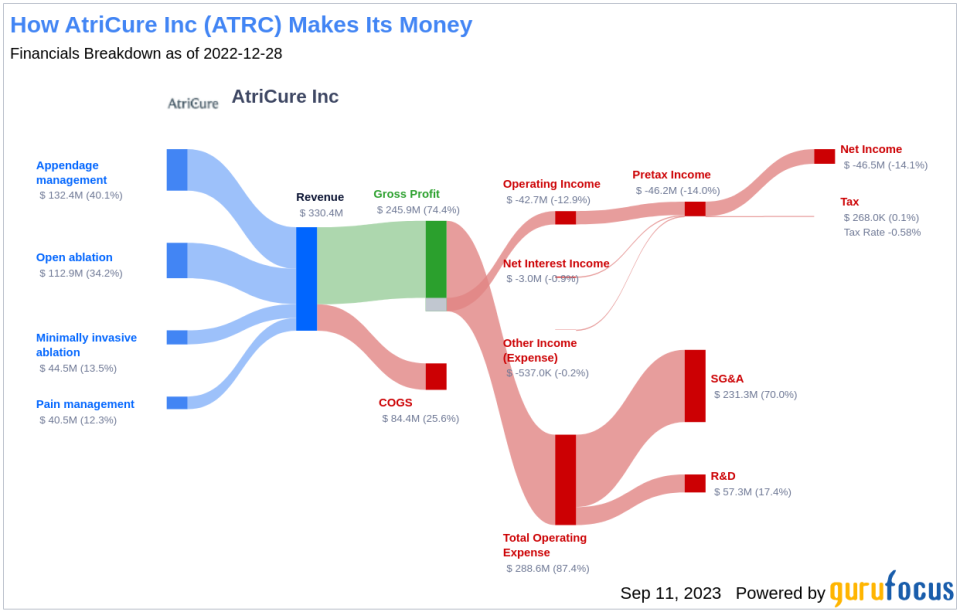

AtriCure Inc is an innovator in surgical treatments and therapies for atrial fibrillation (Afib), left atrial appendage (LAA) management, and post-operative pain management. The company sells its products to medical centers through its direct sales force and distributors. Its product line includes Cryo, Soft Tissue Dissection, RF Ablation Pacing and Sensing, and others. AtriCure also offers a variety of minimally invasive ablation devices and access tools to facilitate the growing trend in less invasive cardiac and thoracic surgery. The majority of its revenue is generated from the United States.

Understanding GF Value

The GF Value represents the current intrinsic value of a stock derived from our exclusive method. The GF Value Line on our summary page gives an overview of the fair value that the stock should be traded at. It is calculated based on three factors: historical multiples that the stock has traded at, GuruFocus adjustment factor based on the company's past returns and growth, and future estimates of the business performance.

The stock of AtriCure (NASDAQ:ATRC) is estimated to be significantly undervalued according to GuruFocus Value calculation. At its current price of $43.4 per share and the market cap of $2.10 billion, AtriCure stock is estimated to be significantly undervalued. As AtriCure is significantly undervalued, the long-term return of its stock is likely to be much higher than its business growth.

Link: These companies may deliever higher future returns at reduced risk.

Evaluating Financial Strength

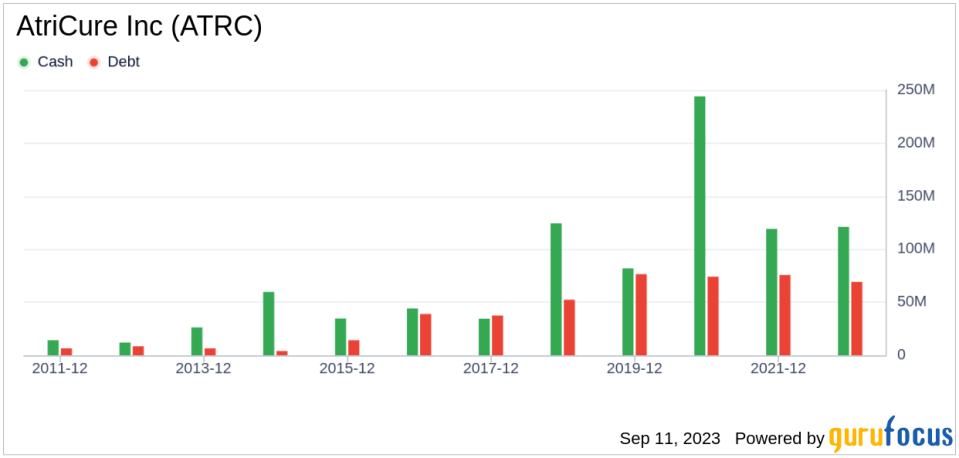

Investing in companies with low financial strength could result in permanent capital loss. Therefore, it's crucial to review a company's financial strength before deciding to buy shares. AtriCure has a cash-to-debt ratio of 1.7, which ranks worse than 55.4% of 834 companies in the Medical Devices & Instruments industry. Based on this, GuruFocus ranks AtriCure's financial strength as 8 out of 10, suggesting a strong balance sheet.

Profitability and Growth

Investing in profitable companies, especially those with consistent profitability over the long term, is less risky. AtriCure has been profitable 1 over the past 10 years. Over the past twelve months, the company had a revenue of $365.70 million and Loss Per Share of $0.61. Its operating margin is -6.78%, which ranks worse than 56.07% of 824 companies in the Medical Devices & Instruments industry. Overall, the profitability of AtriCure is ranked 3 out of 10, which indicates poor profitability.

Growth is one of the most important factors in the valuation of a company. AtriCure's 3-year average revenue growth rate is worse than 55.94% of 724 companies in the Medical Devices & Instruments industry. AtriCure's 3-year average EBITDA growth rate is -4.1%, which ranks worse than 67.95% of 730 companies in the Medical Devices & Instruments industry.

ROIC vs WACC

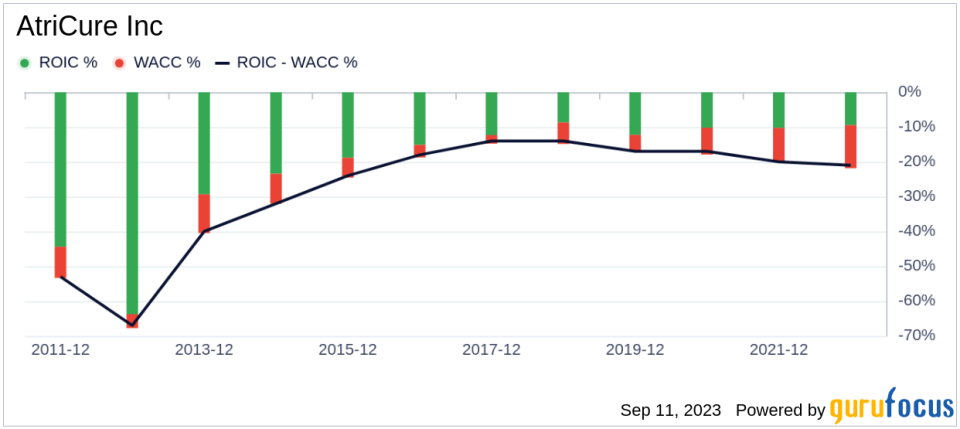

Evaluating a company's profitability by comparing its return on invested capital (ROIC) to its weighted average cost of capital (WACC) is crucial. Return on invested capital (ROIC) measures how well a company generates cash flow relative to the capital it has invested in its business. The weighted average cost of capital (WACC) is the rate that a company is expected to pay on average to all its security holders to finance its assets. If the return on invested capital exceeds the weighted average cost of capital, the company is likely creating value for its shareholders. During the past 12 months, AtriCure's ROIC is -5.8 while its WACC came in at 13.9.

Conclusion

In summary, the stock of AtriCure (NASDAQ:ATRC) is estimated to be significantly undervalued. The company's financial condition is strong and its profitability is poor. Its growth ranks worse than 67.95% of 730 companies in the Medical Devices & Instruments industry. To learn more about AtriCure stock, you can check out its 30-Year Financials here.

To find out the high quality companies that may deliever above average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.