Unveiling The Cooper (COO)'s Value: Is It Really Priced Right? A Comprehensive Guide

The Cooper Companies Inc (NYSE:COO) has experienced a daily loss of -1.61%, and a 3-month gain of 1.04%. With an Earnings Per Share (EPS) of 5.8, the question arises: is the stock modestly undervalued? This article provides an in-depth valuation analysis of The Cooper (NYSE:COO), offering valuable insights for potential investors.

Company Introduction

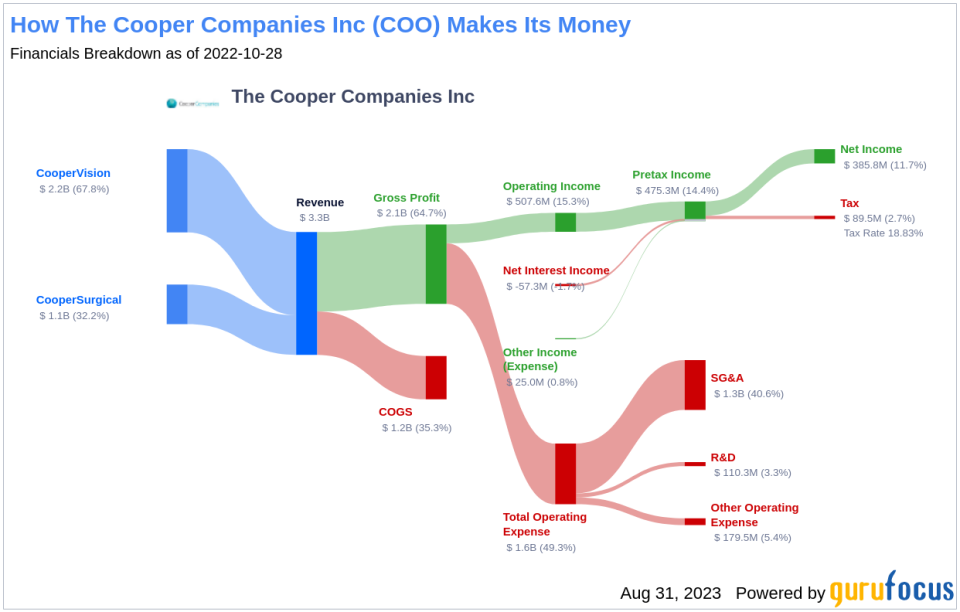

The Cooper Companies Inc (NYSE:COO) is a leading eye care company in the U.S., operating in two segments: CooperVision and CooperSurgical. The company's robust portfolio includes a suite of spherical, multifocal, and toric contact lenses, and it controls approximately a quarter of the U.S. contact lens market. CooperSurgical, founded in 1990, specializes in equipment related to reproductive care, fertility, and women's care. Comparing the stock price and the GF Value, an estimation of fair value, The Cooper appears to be modestly undervalued.

Understanding the GF Value

The GF Value is a proprietary measure that represents the intrinsic value of a stock. It's calculated based on historical multiples, a GuruFocus adjustment factor based on the company's past performance and growth, and future business performance estimates. The GF Value Line on our summary page provides an overview of the fair value that the stock should ideally trade at.

The Cooper (NYSE:COO) is considered to be modestly undervalued based on GuruFocus' valuation method. The GF Value estimates the stock's fair value at $466.88, considering historical multiples, an internal adjustment based on the company's past business growth, and analyst estimates of future business performance. At its current price of $374.71 per share, The Cooper has a market cap of $18.60 billion, suggesting that the stock may be undervalued.

Because The Cooper is relatively undervalued, the long-term return of its stock is likely to be higher than its business growth. This presents an attractive opportunity for value investors.

Financial Strength

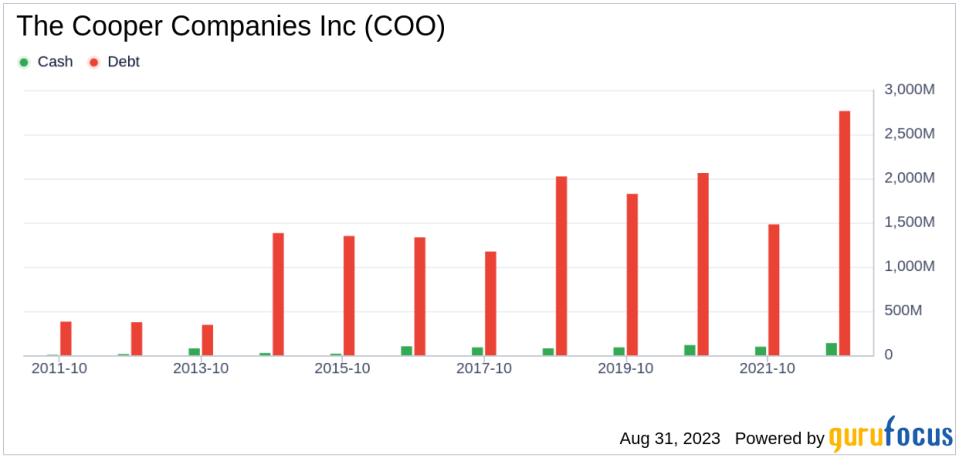

Companies with strong financial strength offer investors a lower risk of permanent capital loss. The Cooper's cash-to-debt ratio of 0.04 ranks worse than 96.76% of 834 companies in the Medical Devices & Instruments industry. However, the overall financial strength of The Cooper is 6 out of 10, indicating fair financial health.

Profitability and Growth

Investing in profitable companies carries less risk, especially in companies that have demonstrated consistent profitability over the long term. The Cooper has been profitable 10 years over the past 10 years. During the past 12 months, the company had revenues of $3.40 billion and Earnings Per Share (EPS) of $5.8. Its operating margin of 14.29% is better than 73.45% of 825 companies in the Medical Devices & Instruments industry. GuruFocus ranks The Cooper's profitability as strong.

Growth is one of the most important factors in the valuation of a company. The average annual revenue growth of The Cooper is 7.8%, which ranks better than 51.25% of 722 companies in the Medical Devices & Instruments industry. However, the 3-year average EBITDA growth is 2.3%, which ranks worse than 60.3% of 728 companies in the Medical Devices & Instruments industry.

ROIC vs WACC

Comparing a company's return on invested capital (ROIC) to its weighted average cost of capital (WACC) can also evaluate a company's profitability. ROIC measures how well a company generates cash flow relative to the capital it has invested in its business. WACC is the rate that a company is expected to pay on average to all its security holders to finance its assets. During the past 12 months, The Cooper's ROIC is 3.34 while its WACC came in at 9.15.

Conclusion

In conclusion, the stock of The Cooper (NYSE:COO) is believed to be modestly undervalued. The company's financial condition is fair, its profitability is strong, but its growth ranks worse than 60.3% of 728 companies in the Medical Devices & Instruments industry. For more details about The Cooper stock, you can check out its 30-Year Financials here.

To find out the high-quality companies that may deliver above-average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.