Unveiling DHT Holdings (DHT)'s Value: Is It Really Priced Right? A Comprehensive Guide

DHT Holdings Inc (NYSE:DHT) recently recorded a daily gain of 3.91% and a 3-month gain of 17.06%. With an Earnings Per Share (EPS) (EPS) of 1, the question arises: is the stock fairly valued? In this article, we delve into an in-depth valuation analysis of DHT Holdings, exploring its intrinsic value, financial strength, and future prospects.

Company Introduction

DHT Holdings Inc is a renowned crude oil tanker company with international operations. Its fleet, consisting of very large crude carriers (VLCCs) ranging in size from 200,000 to 320,000 deadweight tons, primarily generates revenues from time charter and spot market operations. With operational bases in Monaco, Oslo, Norway, and Singapore, DHT Holdings has a prominent global presence.

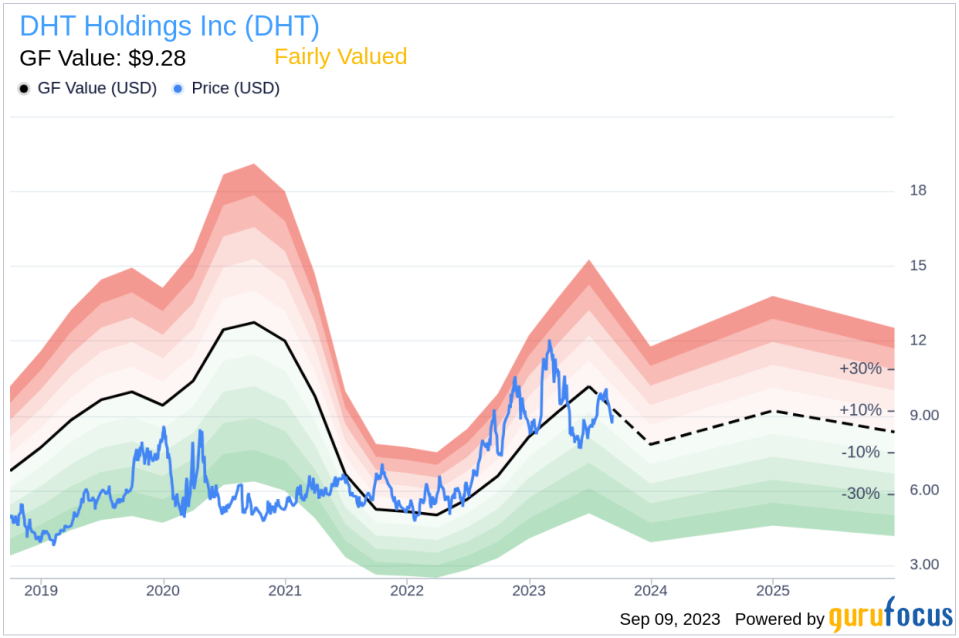

The company's stock is currently priced at $9.04 per share, giving it a market cap of $1.50 billion. To gain insights into the fairness of this valuation, we compare the stock price with the GF Value, a proprietary measure of a stock's intrinsic value, which stands at $9.28 for DHT Holdings.

Understanding the GF Value

The GF Value represents the current intrinsic value of a stock derived from our exclusive method. It takes into account historical multiples (PE Ratio, PS Ratio, PB Ratio, and Price-to-Free-Cash-Flow) that the stock has traded at, GuruFocus adjustment factor based on the company's past returns and growth, and future estimates of the business performance.

DHT Holdings (NYSE:DHT) appears to be fairly valued according to our GF Value estimation. The stock's share price is expected to fluctuate around the GF Value Line. If the share price significantly surpasses the GF Value Line, the stock may be overvalued, leading to poor future returns. Conversely, if it falls significantly below the GF Value Line, the stock may be undervalued and could offer high future returns.

Given that DHT Holdings appears to be fairly valued, the long-term return of its stock is likely to be close to the rate of its business growth.

These companies may deliever higher future returns at reduced risk.

Assessing Financial Strength

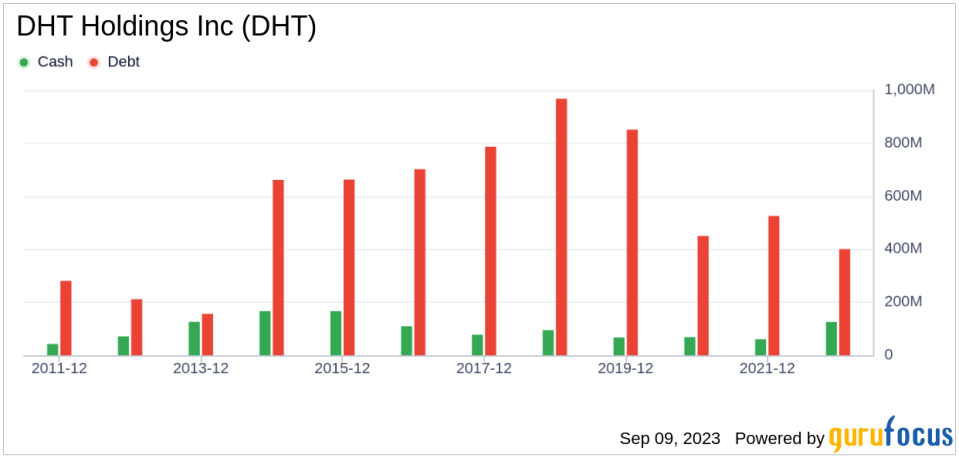

Investing in companies with low financial strength could result in permanent capital loss. Therefore, it's crucial to review a company's financial strength before deciding to buy shares. Looking at the cash-to-debt ratio and interest coverage can provide a good initial perspective on the company's financial strength. DHT Holdings has a cash-to-debt ratio of 0.34, ranking it lower than 58.81% of 1022 companies in the Oil & Gas industry. Based on this, GuruFocus ranks DHT Holdings's financial strength as 7 out of 10, suggesting a fair balance sheet.

Profitability and Growth

Profitable companies, especially those with consistent profitability over the long term, are generally less risky to invest in. DHT Holdings has been profitable 7 over the past 10 years. Over the past twelve months, the company had a revenue of $563.50 million and an Earnings Per Share (EPS) of $1. Its operating margin is 32.43%, ranking better than 76.42% of 967 companies in the Oil & Gas industry. Overall, the profitability of DHT Holdings is ranked 6 out of 10, indicating fair profitability.

Growth is probably one of the most important factors in the valuation of a company. DHT Holdings's 3-year average revenue growth rate is worse than 77.41% of 850 companies in the Oil & Gas industry. DHT Holdings's 3-year average EBITDA growth rate is -4%, ranking worse than 73.17% of 820 companies in the Oil & Gas industry.

Comparing ROIC and WACC

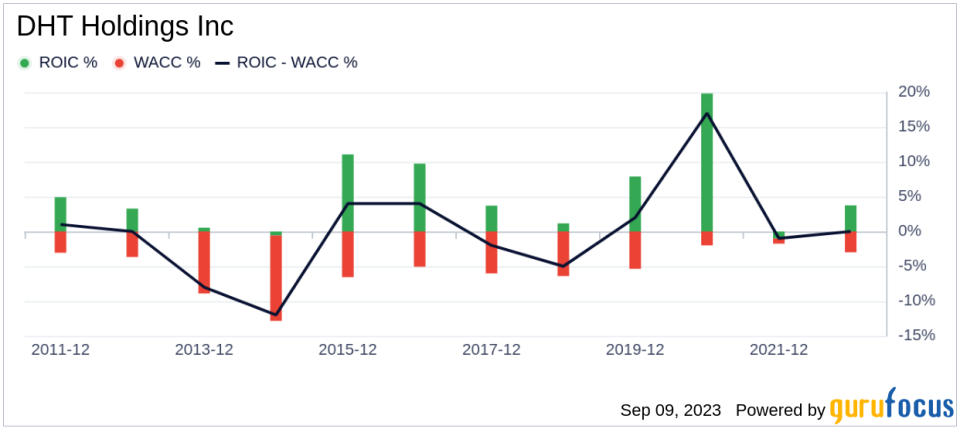

Return on invested capital (ROIC) measures how well a company generates cash flow relative to the capital it has invested in its business. The weighted average cost of capital (WACC) is the rate that a company is expected to pay on average to all its security holders to finance its assets. For the past 12 months, DHT Holdings's return on invested capital is 13.36, and its cost of capital is 5.28.

Conclusion

Overall, DHT Holdings (NYSE:DHT) stock appears to be fairly valued. The company's financial condition is fair, and its profitability is fair. Its growth ranks worse than 73.17% of 820 companies in the Oil & Gas industry. To learn more about DHT Holdings stock, you can check out its 30-Year Financials here.

To find out the high-quality companies that may deliver above-average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.