Unveiling EQT Corp's True Worth: Is It Really Priced Right? A Comprehensive Guide

EQT Corp (NYSE:EQT), a leading natural gas production company, saw a daily gain of 1.1%, despite a 3-month loss of -1.93%. With an Earnings Per Share (EPS) (EPS) of 8.89, the question arises: is the stock significantly overvalued? This article aims to provide an in-depth analysis of EQT's valuation, providing valuable insights for potential investors. Let's dive in.

An Introduction to EQT Corp

EQT Corp is an independent natural gas production company with operations focused in the cores of the Marcellus and Utica shales in the Appalachian Basin, located in the Eastern United States. The company focuses on executing combo-development projects for developing multiwell pads to meet supply needs, with an emphasis on maximizing operational efficiency, technology, and sustainability. Its main customers include marketers, utilities, and industrial operators in the Appalachian Basin.

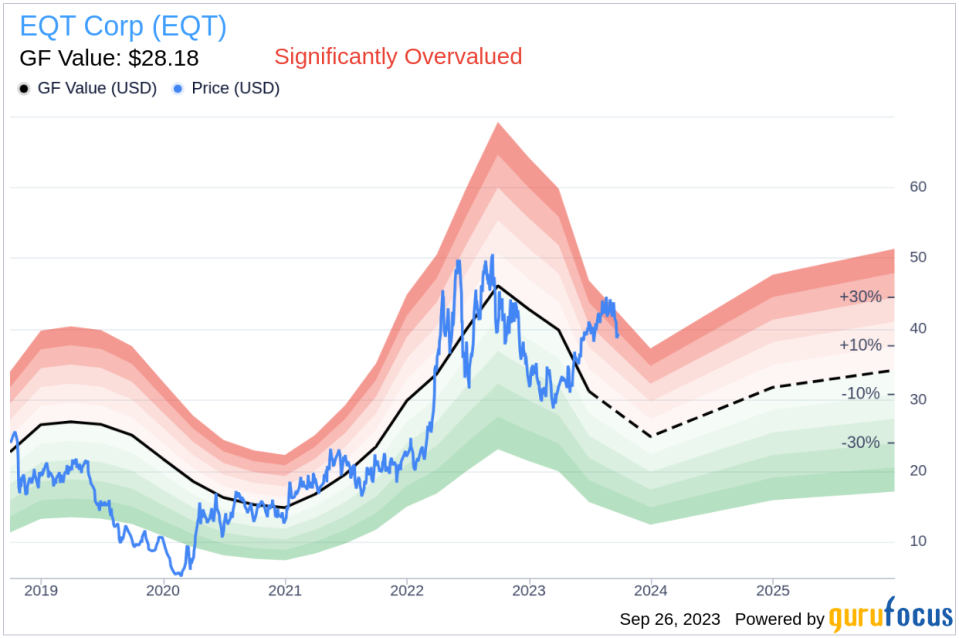

With a current stock price of $39.35, EQT has a market cap of $16.20 billion. However, the GF Value, an estimation of the fair value of the stock, is $28.18. This discrepancy suggests that the stock may be significantly overvalued, a conclusion that will be further examined in the following analysis.

Understanding the GF Value

The GF Value is a proprietary valuation method developed by GuruFocus. The GF Value Line on the summary page represents the fair value at which the stock should ideally be traded. It is calculated based on three factors:

Historical multiples (PE Ratio, PS Ratio, PB Ratio, and Price-to-Free-Cash-Flow) at which the stock has traded.

A GuruFocus adjustment factor based on the company's past returns and growth.

Future estimates of the business performance.

The stock price typically fluctuates around the GF Value Line. If the stock price is significantly above the GF Value Line, it is overvalued and its future return is likely to be poor. On the other hand, if it is significantly below the GF Value Line, its future return will likely be higher.

Based on this method, EQT appears to be significantly overvalued. The stock's fair value is estimated based on historical multiples, an internal adjustment based on the company's past business growth, and analyst estimates of future business performance. If the stock's share price is significantly above the GF Value Line, the stock may be overvalued and have poor future returns. On the other hand, if the stock's share price is significantly below the GF Value Line, the stock may be undervalued and have high future returns.

Because EQT is significantly overvalued, the long-term return of its stock is likely to be much lower than its future business growth.

Link: These companies may deliver higher future returns at reduced risk.

Examining EQT's Financial Strength

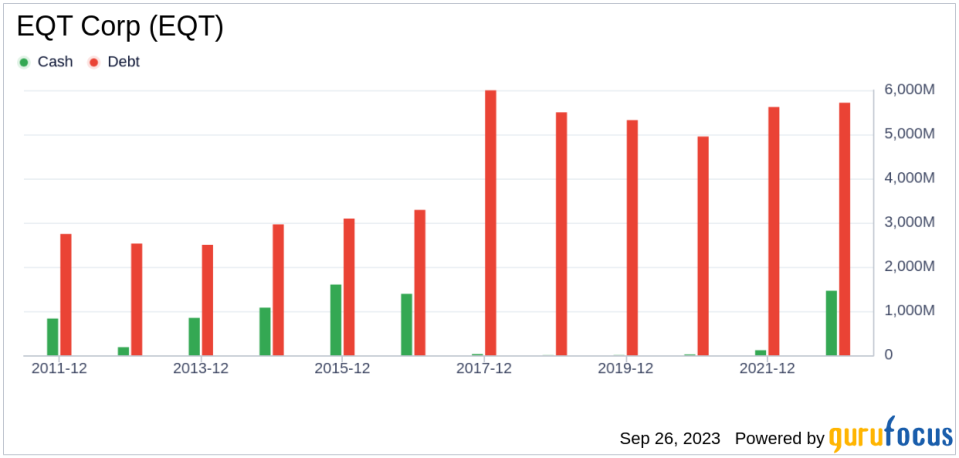

Investing in companies with low financial strength could result in permanent capital loss. Therefore, it's crucial for investors to carefully review a company's financial strength before deciding whether to buy shares. Looking at the cash-to-debt ratio and interest coverage can give a good initial perspective on the company's financial strength. EQT has a cash-to-debt ratio of 0.26, which ranks worse than 63.83% of 1034 companies in the Oil & Gas industry. Based on this, GuruFocus ranks EQT's financial strength as 6 out of 10, suggesting a fair balance sheet.

Profitability and Growth of EQT

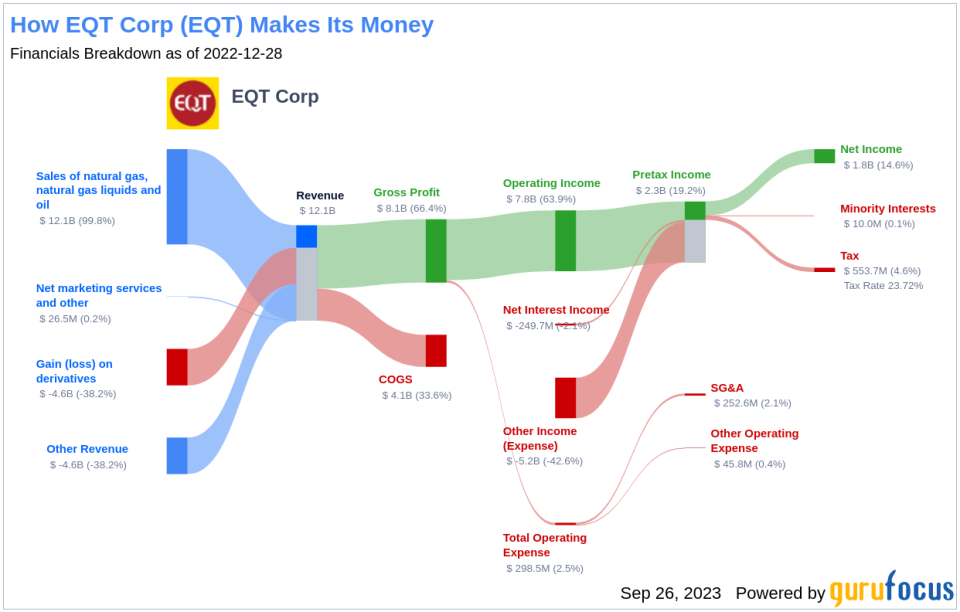

Investing in profitable companies carries less risk, especially in companies that have demonstrated consistent profitability over the long term. Typically, a company with high profit margins offers better performance potential than a company with low profit margins. EQT has been profitable 5 years over the past 10 years. During the past 12 months, the company had revenues of $9 billion and Earnings Per Share (EPS) of $8.89. Its operating margin of 52.69% is better than 92.17% of 984 companies in the Oil & Gas industry. Overall, GuruFocus ranks EQT's profitability as fair.

Growth is probably the most important factor in the valuation of a company. GuruFocus research has found that growth is closely correlated with the long-term stock performance of a company. A faster-growing company creates more value for shareholders, especially if the growth is profitable. The 3-year average annual revenue growth of EQT is 26.1%, which ranks better than 79.35% of 862 companies in the Oil & Gas industry. The 3-year average EBITDA growth rate is 137.6%, which ranks better than 97.71% of 829 companies in the Oil & Gas industry.

Comparing ROIC and WACC

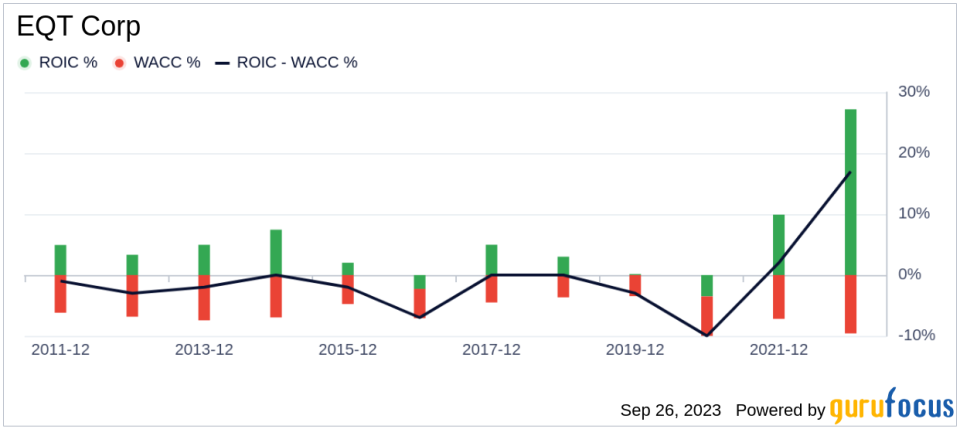

Another way to look at the profitability of a company is to compare its return on invested capital and the weighted cost of capital. Return on invested capital (ROIC) measures how well a company generates cash flow relative to the capital it has invested in its business. The weighted average cost of capital (WACC) is the rate that a company is expected to pay on average to all its security holders to finance its assets. We want to have the return on invested capital higher than the weighted cost of capital. For the past 12 months, EQT's return on invested capital is 16.78, and its cost of capital is 7.48.

Conclusion

In conclusion, the stock of EQT Corp (NYSE:EQT) appears to be significantly overvalued. The company's financial condition is fair, and its profitability is fair. Its growth ranks better than 97.71% of 829 companies in the Oil & Gas industry. To learn more about EQT stock, you can check out its 30-Year Financials here.

To find out the high-quality companies that may deliver above-average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.