Unveiling Five Below (FIVE)'s Value: Is It Really Priced Right? A Comprehensive Guide

Five Below Inc (NASDAQ:FIVE) experienced a day's loss of -1.81% and a 3-month loss of -16.45%. Despite these figures, the company boasts an Earnings Per Share (EPS) (EPS) of 4.87. This raises the question: is Five Below modestly undervalued? This article aims to provide a comprehensive valuation analysis of Five Below. Let's delve in.

Company Overview

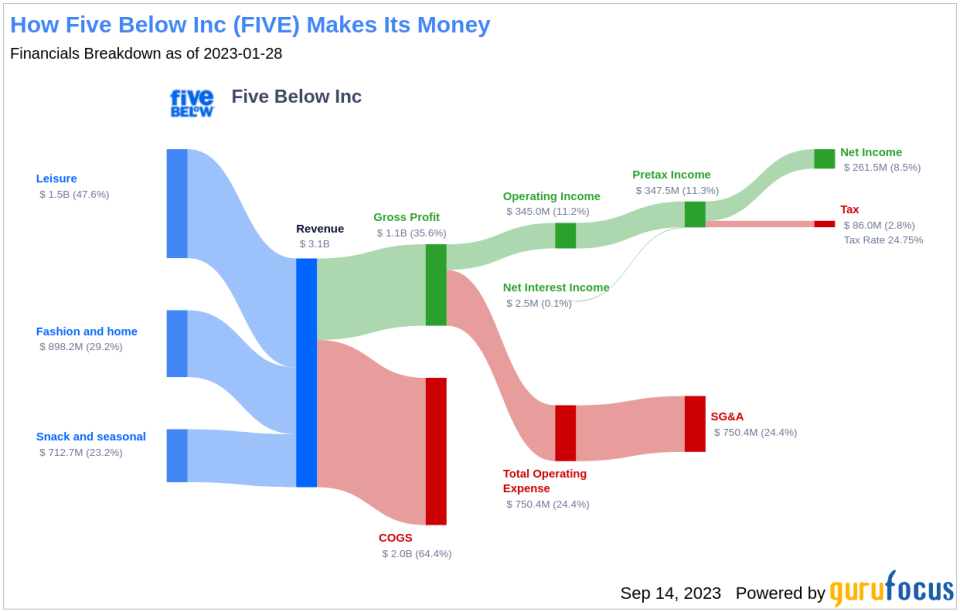

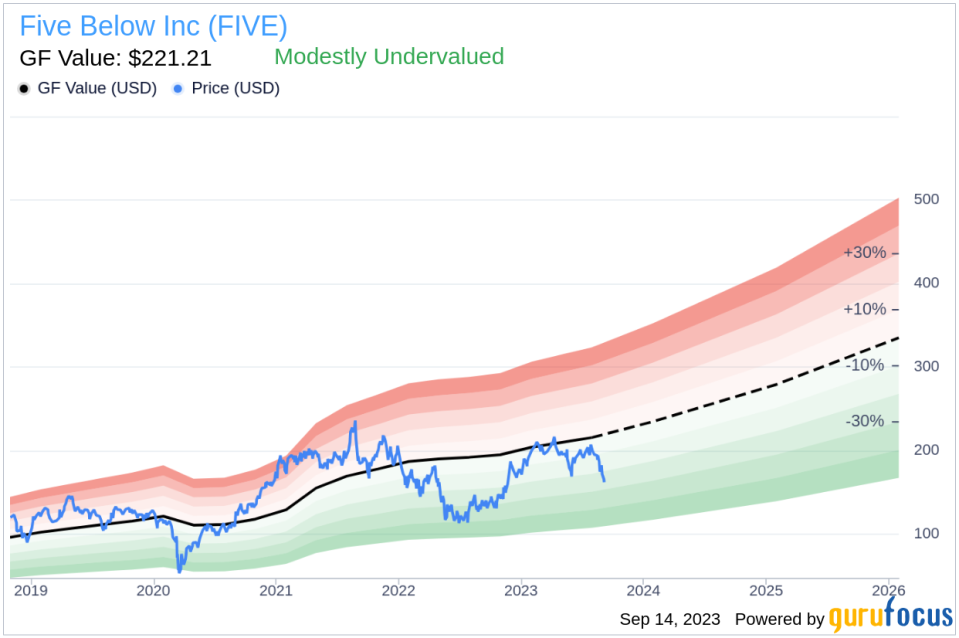

Five Below is a value-oriented retailer that operates 1,340 stores in 42 states across the United States. It primarily caters to teen and preteen consumers, offering a wide variety of merchandise priced below $6. The company's product assortment focuses on discretionary items in several categories, including leisure, fashion and home, and party and snack. As of the end of fiscal 2022, Five Below reported a stock price of $159.76 and a fair value (GF Value) of $221.21.

Understanding GF Value

The GF Value is a proprietary measure of a stock's intrinsic value, computed considering historical trading multiples, a GuruFocus adjustment factor based on past performance and growth, and future business performance estimates. The GF Value Line denotes the stock's ideal fair trading value. We believe the GF Value Line is the fair value that the stock should be traded at.

According to our valuation method, Five Below (NASDAQ:FIVE) appears to be modestly undervalued. The GF Value estimates the stock's fair value based on historical multiples, an internal adjustment based on past business growth, and analyst estimates of future business performance. If the share price is significantly above the GF Value Line, the stock may be overvalued and have poor future returns. Conversely, if the share price is significantly below the GF Value calculation, the stock may be undervalued and have higher future returns. With its current price of $159.76 per share, Five Below stock is believed to be modestly undervalued.

As Five Below is relatively undervalued, the long-term return of its stock is likely to be higher than its business growth.

Financial Strength

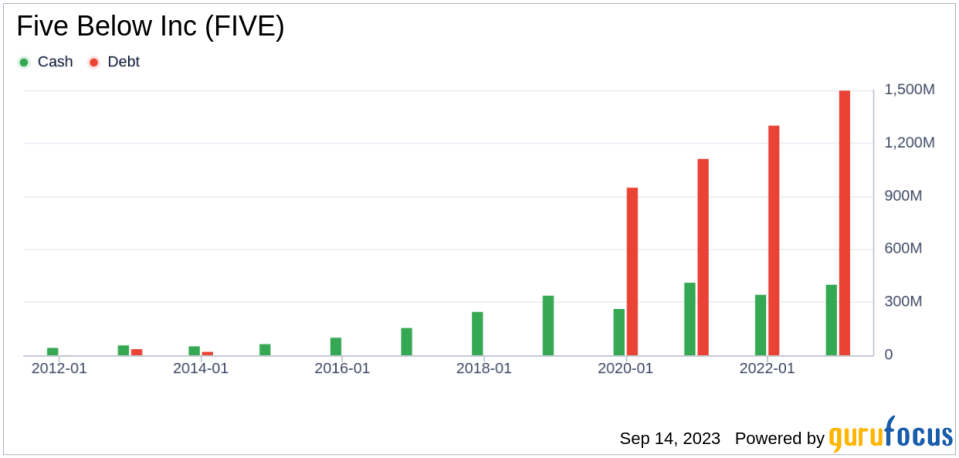

Investing in companies with low financial strength could result in permanent capital loss. Therefore, it's crucial to assess a company's financial strength before deciding to buy its shares. Five Below has a cash-to-debt ratio of 0.27, ranking worse than 61.66% of 1098 companies in the Retail - Cyclical industry. Based on this, GuruFocus ranks Five Below's financial strength as 5 out of 10, suggesting a fair balance sheet.

Profitability and Growth

Investing in profitable companies carries less risk, especially those that have demonstrated consistent profitability over the long term. Five Below has been profitable for 10 years over the past 10 years. During the past 12 months, the company had revenues of $3.30 billion and an Earnings Per Share (EPS) of $4.87. Its operating margin of 10.69% is better than 80.13% of 1097 companies in the Retail - Cyclical industry. Overall, GuruFocus ranks Five Below's profitability as strong.

Growth is probably the most important factor in the valuation of a company. A faster-growing company creates more value for shareholders, especially if the growth is profitable. The 3-year average annual revenue growth of Five Below is 18.8%, which ranks better than 80.46% of 1044 companies in the Retail - Cyclical industry. The 3-year average EBITDA growth rate is 18.6%, which ranks better than 68.64% of 896 companies in the Retail - Cyclical industry.

ROIC vs WACC

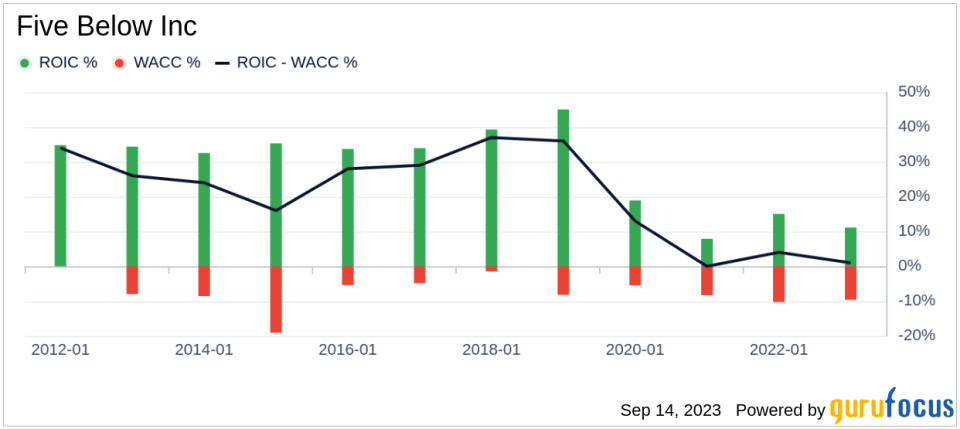

An effective way to evaluate a company's profitability is to compare its return on invested capital (ROIC) and the weighted average cost of capital (WACC). ROIC measures how well a company generates cash flow relative to the capital it has invested in its business. WACC represents the average rate a company is expected to pay to finance its assets. Ideally, the ROIC should be higher than the WACC. For the past 12 months, Five Below's ROIC is 10.37, and its cost of capital is 8.54.

Conclusion

In conclusion, Five Below (NASDAQ:FIVE) appears to be modestly undervalued. The company's financial condition is fair, and its profitability is strong. Its growth ranks better than 68.64% of 896 companies in the Retail - Cyclical industry. To learn more about Five Below stock, you can check out its 30-Year Financials here.

To find out the high-quality companies that may deliver above-average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.